Buying a home in Seattle's competitive real estate market requires more than just finding the right property. Behind every successful home purchase stands a critical professional who guides borrowers through the complex mortgage process: the house loan officer. This financial expert serves as your advocate, advisor, and coordinator throughout one of the most significant financial decisions you'll make. Whether you're a first-time buyer in Shoreline, a tech professional in Bellevue looking to leverage stock compensation, or a seasoned investor in Kirkland, understanding what a house loan officer does can dramatically improve your homebuying experience and financial outcomes.

The Core Responsibilities of a House Loan Officer

A house loan officer functions as the primary point of contact between borrowers and mortgage lenders, managing the entire loan application process from initial consultation to closing. Their expertise extends far beyond simply taking applications and processing paperwork.

Financial Assessment and Pre-Qualification

One of the first and most important functions involves evaluating a borrower's financial situation to determine loan eligibility. A skilled house loan officer reviews:

- Credit reports and scores to identify potential issues

- Income documentation including W-2s, tax returns, and pay stubs

- Debt-to-income ratios to assess borrowing capacity

- Employment history and stability

- Asset documentation for down payment and reserves

For Seattle-area tech professionals working at companies like Amazon, Microsoft, or Google, this assessment becomes particularly nuanced. A specialized house loan officer understands how to properly qualify restricted stock units (RSUs), employee stock purchase plans, and performance bonuses to maximize buying power for jumbo loan purchases.

Loan Product Selection and Strategy

The mortgage landscape offers numerous loan programs, each with distinct requirements, benefits, and costs. According to SmartAsset’s overview of loan officer functions, one of the primary responsibilities is matching borrowers with the most appropriate loan products.

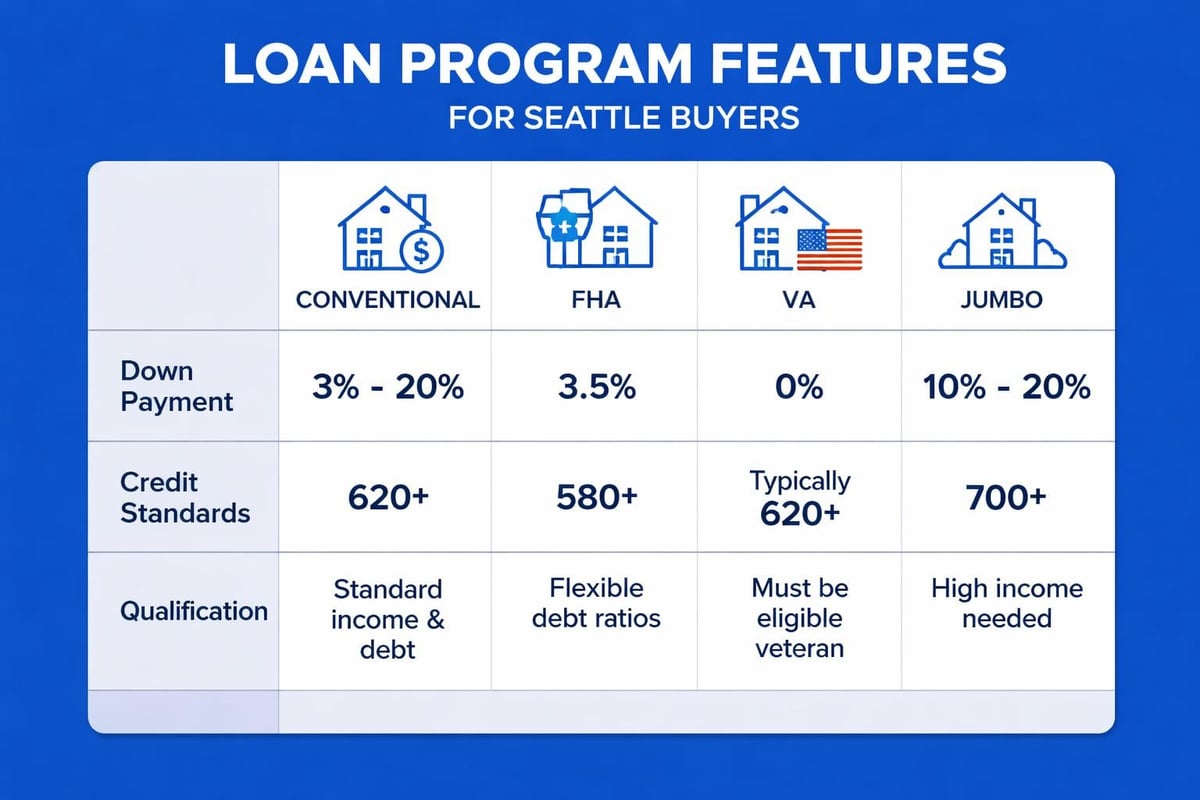

Common loan types a house loan officer might recommend include:

- Conventional loans with varying down payment options

- FHA loans for borrowers with lower credit scores or limited funds

- VA loans for eligible veterans and service members

- Jumbo loans for high-balance purchases in expensive markets

- Specialized programs for first-time homebuyers in Seattle

The right loan choice depends on individual circumstances, market conditions, and long-term financial goals. A house loan officer analyzes these factors to create a customized lending strategy rather than offering one-size-fits-all solutions.

The Mortgage Application Process Management

Once a borrower selects a loan program, the house loan officer orchestrates a complex series of tasks involving multiple parties and strict timelines. This coordination separates exceptional loan officers from average ones, particularly in competitive markets like Bellevue and Redmond where speed matters.

Documentation Collection and Verification

The house loan officer must gather, organize, and submit complete documentation packages to underwriting. This includes:

| Document Category | Typical Requirements | Special Considerations |

|---|---|---|

| Income Verification | Recent pay stubs, W-2s, tax returns | RSU vesting schedules, bonus history for tech workers |

| Asset Documentation | Bank statements, investment accounts | Gift funds, crypto holdings, stock portfolios |

| Credit Information | Tri-merge credit report, tradelines | Credit inquiries, dispute resolutions |

| Property Documents | Purchase agreement, appraisal | HOA docs for condos in Seattle high-rises |

A detail-oriented house loan officer catches missing information early, preventing delays that could jeopardize purchase contracts in time-sensitive transactions.

Underwriting Coordination

After submission, the house loan officer serves as the liaison between the borrower and the underwriting team. According to Mortgage Professional America’s guide to loan officer duties, this coordination role is critical for maintaining momentum.

Key underwriting coordination tasks include:

- Explaining underwriting conditions to borrowers in plain language

- Gathering additional documentation requested by underwriters

- Advocating for borrowers when circumstances require clarification

- Troubleshooting issues that arise during the review process

- Keeping all parties informed of status and timeline updates

For buyers working with tight closing deadlines common in Seattle's fast-paced market, having a house loan officer who maintains excellent underwriter relationships and can expedite reviews becomes invaluable. Some lenders like Fairway can close loans in as few as 9 business days when properly coordinated.

Client Education and Transparency

Beyond the technical aspects of loan processing, an exceptional house loan officer serves an educational role that empowers borrowers to make informed decisions. This function becomes especially important for first-time buyers in areas like Lake Forest Park or Lynnwood who may be unfamiliar with mortgage terminology and processes.

Explaining Mortgage Terms and Costs

A transparent house loan officer breaks down complex concepts into understandable terms:

- Interest rates versus APR and why both matter

- Points and credits and when each makes financial sense

- Closing costs itemized and explained

- Escrow accounts for taxes and insurance

- Private mortgage insurance (PMI) requirements and elimination strategies

Rather than overwhelming borrowers with jargon, skilled professionals use real numbers and scenarios relevant to the Seattle market to illustrate concepts. For example, explaining how a conventional loan with 5% down compares to 20% down in terms of monthly payment, PMI costs, and overall investment return.

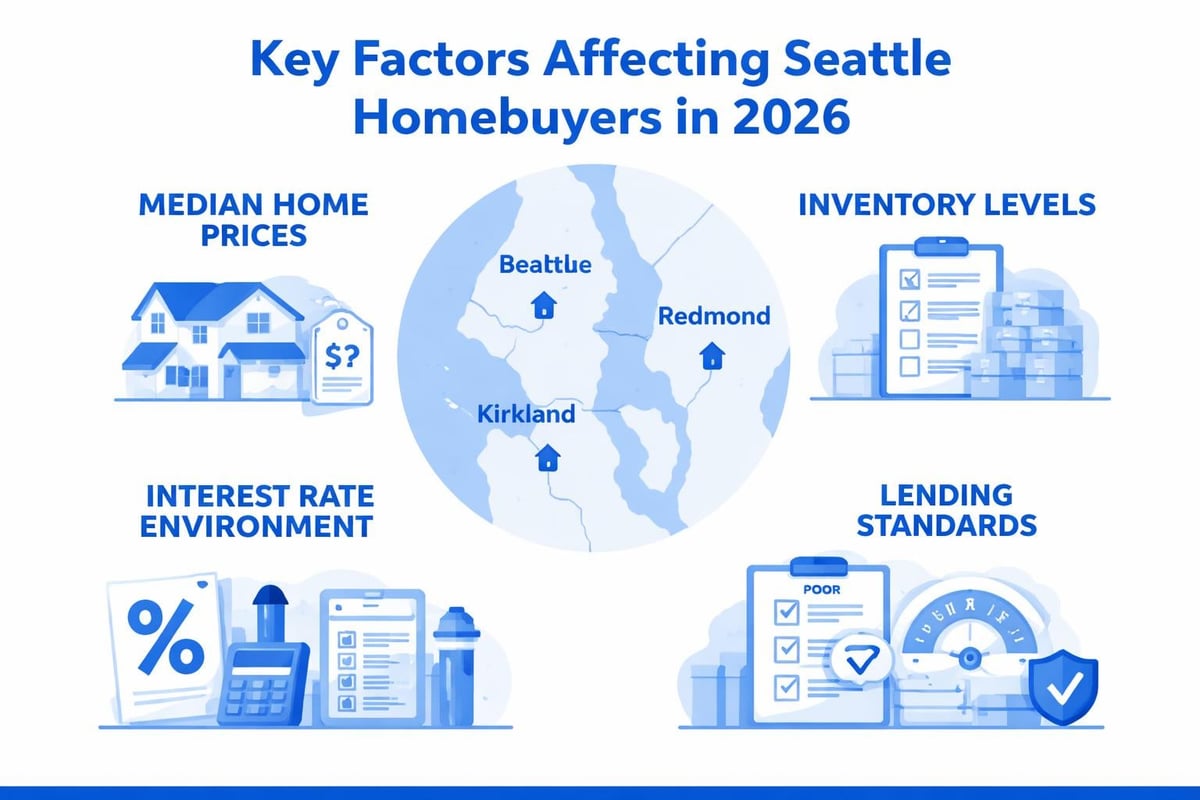

Market-Specific Guidance

Local market knowledge distinguishes a house loan officer who truly serves their community. In 2026, Seattle-area buyers face unique challenges including:

- Median home prices significantly above the national average

- Multiple offer situations requiring strong pre-approvals

- Condo financing complexities due to building age and FHA approval status

- Property tax considerations that vary by city

- Rapidly evolving inventory levels across different neighborhoods

A house loan officer familiar with top mortgage brokers in Seattle and local market conditions can advise on competitive strategies, realistic timelines, and neighborhood-specific financing considerations.

Building Relationships with Real Estate Professionals

A house loan officer doesn't work in isolation but as part of a broader team that includes real estate agents, escrow officers, appraisers, and title companies. These professional relationships directly impact client outcomes.

Agent Partnerships and Communication

Real estate agents rely on responsive, competent loan officers to close their transactions successfully. Coursera’s guide on becoming a loan officer emphasizes that communication skills rank among the most important attributes for success in this role.

Effective house loan officers maintain agent relationships by:

- Providing accurate pre-approval letters with verified information

- Responding quickly to questions about buyer qualifications

- Meeting promised timelines and setting realistic expectations

- Proactively communicating potential issues before they become problems

- Being available during evenings and weekends when offers happen

In competitive Seattle neighborhoods like Fremont or Capitol Hill, a house loan officer's reputation with local agents can make the difference between an accepted offer and a passed-over bid.

Coordinating the Closing Process

As the closing date approaches, the house loan officer ensures all parties have what they need for a smooth settlement:

- Coordinating with the title company on closing disclosure timing

- Verifying final loan numbers match buyer expectations

- Confirming funding will be available on schedule

- Explaining the closing process and what to bring

- Being available to troubleshoot last-minute issues

This coordination becomes particularly important when working with conventional loans for investment properties or other complex transactions that may involve additional requirements or documentation.

Specialized Knowledge Areas

The mortgage industry requires continuous education as regulations, programs, and guidelines evolve. An experienced house loan officer develops specialized expertise in areas that benefit specific client segments.

Stock Compensation and Tech Employee Lending

Seattle's economy centers heavily on technology companies, creating unique lending scenarios. A house loan officer serving this market must understand:

| Compensation Type | Qualification Approach | Documentation Needed |

|---|---|---|

| RSUs (Restricted Stock Units) | Typically 2-year vesting history required | Vesting schedules, tax returns showing receipt |

| Stock Options | Generally not qualifying income | May be counted as assets if exercised |

| Signing Bonuses | Must demonstrate likelihood of continuation | Offer letters, company policy documentation |

| Performance Bonuses | 2-year history, stability analysis | W-2s, bonus letters, pay stubs |

This specialized knowledge allows a house loan officer to maximize borrowing capacity for tech professionals who might otherwise struggle to qualify despite strong total compensation packages.

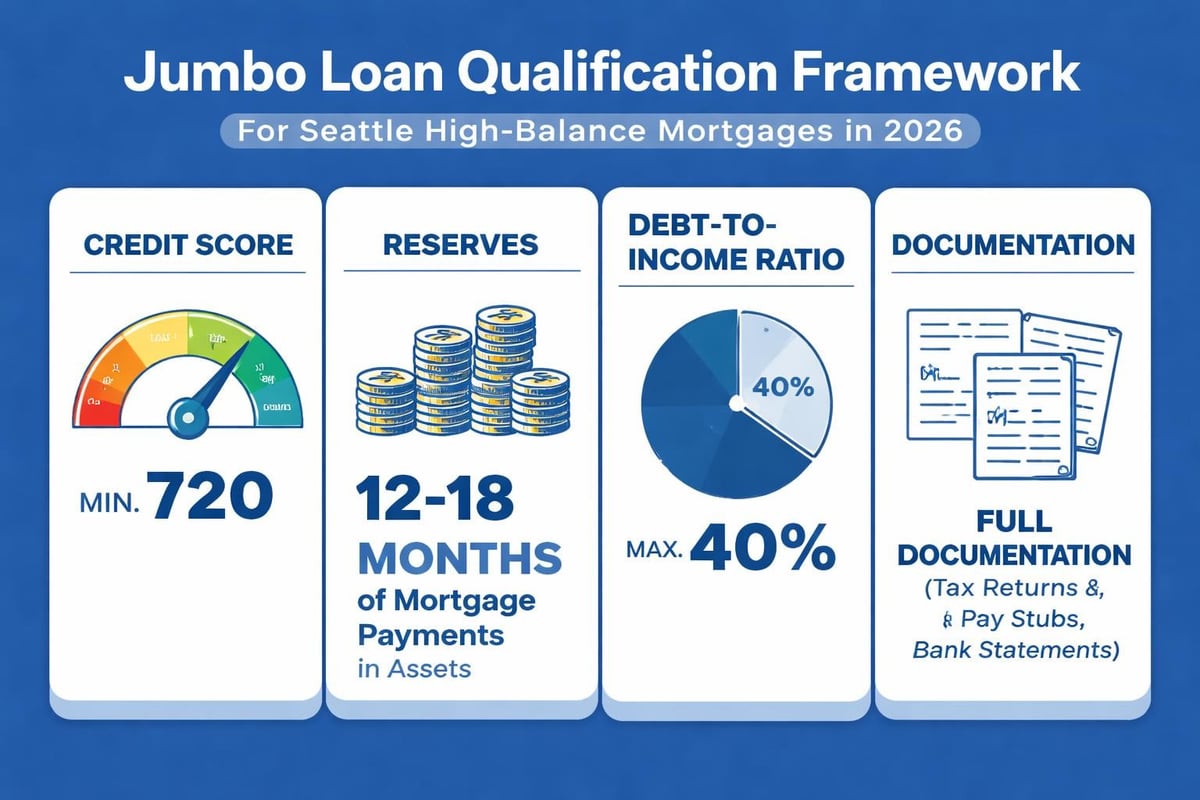

Jumbo Loan Expertise

With Seattle's median home prices consistently exceeding conventional loan limits, jumbo financing knowledge becomes essential. A house loan officer specializing in jumbo loans understands:

- Stricter credit score requirements (typically 700+)

- Higher reserve requirements (often 6-12 months)

- More comprehensive income documentation

- Property appraisal complexities for high-value homes

- Competitive rate structures and relationship pricing

This expertise proves invaluable for buyers in higher-priced areas like Medina, Mercer Island, or waterfront properties throughout the region.

Regulatory Compliance and Ethics

The mortgage industry operates under strict federal and state regulations designed to protect consumers. A licensed house loan officer must maintain compliance while serving clients effectively.

Licensing and Continuing Education

According to Truity’s career profile for loan officers, all mortgage loan officers must obtain a Nationwide Multistate Licensing System (NMLS) number after completing education, passing an exam, and undergoing background checks.

Ongoing requirements include:

- Annual continuing education courses (typically 8 hours)

- Criminal background checks and credit report reviews

- Maintaining errors and omissions insurance

- Staying current on regulation changes

- Company-specific compliance training

These requirements ensure that a house loan officer maintains current knowledge of lending laws, fair housing regulations, and consumer protection statutes.

Ethical Lending Practices

Beyond legal compliance, ethical house loan officers prioritize client interests over commission potential. This means:

- Recommending appropriate loan amounts, not maximum qualifying amounts

- Disclosing all costs transparently without hidden fees

- Steering clients toward products that match their circumstances

- Providing honest assessments of affordability and risk

- Maintaining confidentiality of financial information

According to LHH’s loan officer job description, integrity and trustworthiness rank among the most valued traits in successful loan officers, particularly for those building long-term reputations in specific communities like Everett or Mill Creek.

Technology and Tools of the Trade

Modern mortgage lending relies heavily on technology platforms that streamline processes and improve accuracy. A tech-savvy house loan officer leverages these tools to provide better service.

Loan Origination Systems

Professional loan officers work within sophisticated loan origination systems (LOS) that:

- Automate application intake and data validation

- Generate pre-approval letters instantly

- Track documentation requirements and deadlines

- Integrate with credit reporting and verification services

- Provide real-time pipeline visibility to all stakeholders

These systems allow a house loan officer to manage higher transaction volumes while maintaining attention to detail and personalized service.

Digital Communication Platforms

In 2026, borrowers expect convenient, responsive communication through their preferred channels. Progressive house loan officers utilize:

- Secure document upload portals for easy submission

- Text messaging for quick updates and questions

- Video conferencing for remote consultations

- Electronic signature platforms for paperless transactions

- Mobile apps that provide 24/7 loan status access

This technological flexibility particularly appeals to younger buyers in tech-forward cities like Redmond who expect digital-first experiences similar to what they encounter in their professional lives.

Measuring Success and Client Satisfaction

The effectiveness of a house loan officer can be measured through various metrics that reflect both technical competence and relationship quality.

Performance Indicators

| Metric | What It Measures | Industry Benchmark |

|---|---|---|

| Close Rate | Percentage of applications that fund | 75-85% |

| Average Days to Close | Speed of transaction completion | 30-45 days |

| Client Retention | Repeat and referral business | 40-60% |

| Review Ratings | Client satisfaction scores | 4.5+ stars |

| Loan Quality | Pull-through rate, defects | <2% fallout |

A house loan officer with consistently strong metrics across these areas demonstrates both competence and commitment to client success.

Building a Review Portfolio

In today's digital marketplace, online reviews significantly influence consumer decisions. Exceptional loan officers accumulate hundreds of five-star reviews across platforms like Google, Zillow, and Yelp by consistently delivering outstanding experiences.

These reviews often highlight specific qualities borrowers value:

- Clear communication throughout the process

- Availability and responsiveness to questions

- Problem-solving when unexpected issues arise

- Educational approach that builds confidence

- Successfully closing on time as promised

For borrowers researching mortgage brokers in Seattle, review portfolios provide valuable insights into what working with a particular house loan officer will be like.

Career Path and Professional Development

Understanding the career trajectory of loan officers provides context for their experience levels and expertise depth. According to Maryville University’s overview of loan officer careers, most successful professionals follow similar developmental paths.

Entry and Growth Stages

- Entry-level (Years 1-3): Learning products, building pipelines, establishing processes

- Experienced (Years 4-10): Developing specializations, growing referral networks, increasing volume

- Senior (Years 10-25+): Deep expertise, extensive networks, mentoring others, market leadership

A house loan officer with 25+ years of experience brings invaluable perspective that only comes from navigating multiple market cycles, regulatory changes, and thousands of unique borrower situations.

Specialization Development

As loan officers advance, many develop focused expertise areas such as:

- First-time homebuyer programs and education

- Real estate investor financing strategies

- Reverse mortgages for retirement planning

- Construction and renovation lending

- Self-employed borrower qualification

This specialization allows them to serve specific client segments with exceptional depth of knowledge and proven strategies for success.

Choosing the Right House Loan Officer

With hundreds of loan officers operating in the Seattle area, selecting the right professional for your situation requires careful consideration. Indeed’s loan officer job description outlines the qualifications to look for when evaluating options.

Key Selection Criteria

Experience and track record: How long have they been originating loans? What's their close rate? Do they have experience with your specific situation (tech compensation, jumbo loans, investment properties)?

Local market knowledge: Are they familiar with Seattle-area neighborhoods, pricing trends, and common challenges? Can they provide insights specific to Shoreline, Lynnwood, or other local cities?

Communication style: Do they respond promptly? Explain concepts clearly? Make you feel heard and valued?

Technology capabilities: Can they offer convenient digital processes? Provide real-time updates? Work efficiently to meet tight timelines?

Reviews and reputation: What do past clients say about their experience? Are reviews consistently positive across multiple platforms?

For those comparing options, exploring resources like home buying strategies guides can provide additional context for what excellent service looks like.

Questions to Ask Prospective Loan Officers

During initial consultations, informed borrowers ask questions like:

- What loan programs do you recommend for my situation and why?

- How do you handle stock compensation or bonus income?

- What's your average time to close and current pipeline status?

- Who will I work with day-to-day if not directly with you?

- How do you communicate updates and handle questions?

- What makes your approach different from other loan officers?

The answers reveal not just technical knowledge but also the house loan officer's philosophy, priorities, and commitment to client success.

The Value Proposition in Competitive Markets

Seattle's real estate market presents unique challenges that amplify the importance of working with an exceptional house loan officer. In environments where properties receive multiple offers and sellers have significant leverage, your financing professional can make or break your success.

Speed and Certainty in Multiple Offer Situations

When competing against cash buyers or other well-qualified purchasers, your house loan officer's reputation matters. Listing agents and sellers favor offers backed by:

- Pre-approvals from known, reputable lenders

- Loan officers with track records of closing on time

- Clear communication about borrower strength

- Flexible problem-solving when inspections reveal issues

A house loan officer with strong relationships throughout the Seattle real estate community provides a competitive advantage that extends beyond just the loan terms themselves.

Long-term Financial Partnership

The best house loan officers view client relationships as long-term partnerships rather than single transactions. This means:

- Monitoring rates for refinance opportunities

- Checking in periodically about financial goals

- Providing guidance on home equity strategies

- Assisting with future purchases or investment properties

- Serving as a trusted resource for financial questions

This ongoing relationship approach builds trust and ensures you always have expert guidance available as your financial situation and goals evolve.

Navigating Seattle's complex mortgage landscape requires more than just loan products-it demands an experienced guide who combines technical expertise, market knowledge, and genuine commitment to your success. Whether you're purchasing your first home in Lake Forest Park, leveraging stock compensation for a jumbo loan in Bellevue, or expanding your investment portfolio in Everett, the right house loan officer transforms a potentially stressful process into a confident journey toward homeownership. Keith Akada has spent over 25 years helping Seattle-area buyers and homeowners achieve their real estate goals through education, transparency, and proven execution. With 750+ five-star reviews and specialized expertise in tech compensation and competitive markets, Mortgage Reel delivers the strategic guidance and reliable service that turns homeownership dreams into reality.