Purchasing a home represents one of the most significant financial decisions you'll ever make, particularly in competitive markets like Seattle, Bellevue, and Redmond. Without proper mortgage education, even well-qualified buyers can struggle to navigate loan programs, understand true affordability, or recognize when they're being steered toward unsuitable products. The foundation of a successful home purchase starts with understanding how mortgages work, what lenders evaluate, and which strategies align with your specific financial situation and long-term goals.

Understanding the Core Components of Mortgage Education

Effective mortgage education extends far beyond simply comparing interest rates. It encompasses understanding how lenders evaluate creditworthiness, how different loan structures impact long-term costs, and how your unique income sources affect qualification. For tech professionals in Seattle working at Amazon, Microsoft, or Google, this becomes particularly important when stock compensation, RSUs, and bonus income factor into buying power.

The fundamental elements every homebuyer should master include:

- Credit score requirements and how they affect both approval and pricing

- Debt-to-income ratio calculations and acceptable thresholds

- Down payment requirements across different loan programs

- Closing costs, prepaid items, and reserve requirements

- Interest rate structures including fixed-rate versus adjustable-rate mortgages

- Private mortgage insurance (PMI) and how to avoid or eliminate it

The Federal Housing Finance Agency provides comprehensive mortgage education resources that cover these fundamentals and help buyers understand their rights and responsibilities throughout the lending process.

Income Qualification Strategies for Seattle Tech Workers

Traditional mortgage education often focuses on W-2 income from single employers, but the reality for many Seattle-area homebuyers involves more complex compensation structures. Understanding how underwriters evaluate RSUs, stock options, and performance bonuses can dramatically increase your purchasing power.

Stock-based compensation requires specific documentation and qualification approaches:

- Restricted Stock Units (RSUs): Two-year history of vesting typically required for full consideration

- Stock Options: Evaluated based on exercise history and current vested amounts

- Performance Bonuses: Minimum two-year history with consistency analysis

- Base Salary Plus Equity: Combined calculation using verified income patterns

For first-time buyers working in Seattle's tech sector, proper mortgage education for first-time homebuyers should specifically address how these income sources translate into qualification dollars. Many buyers unnecessarily limit their search price range because they don't understand how their total compensation package qualifies.

Loan Program Selection and Strategic Planning

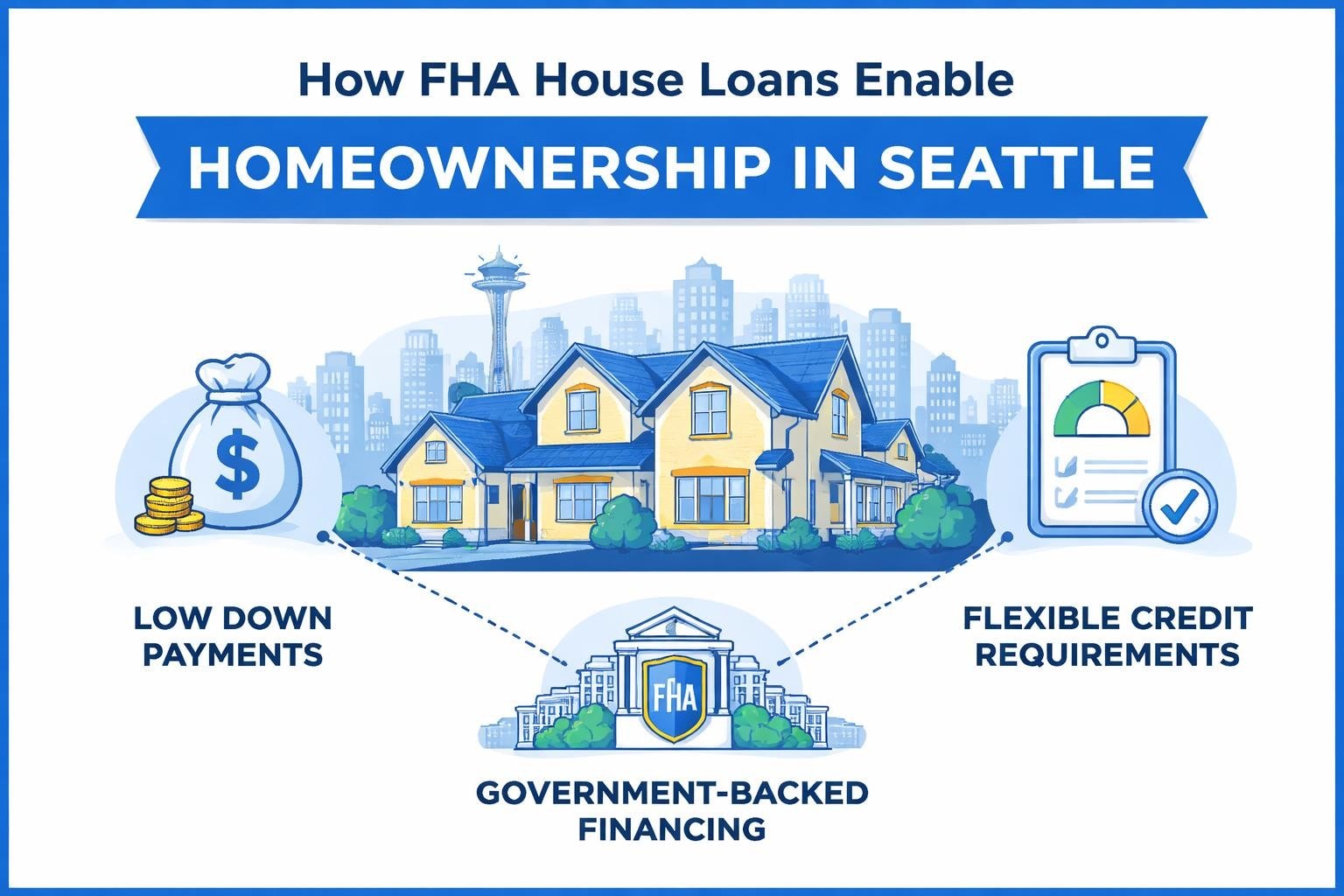

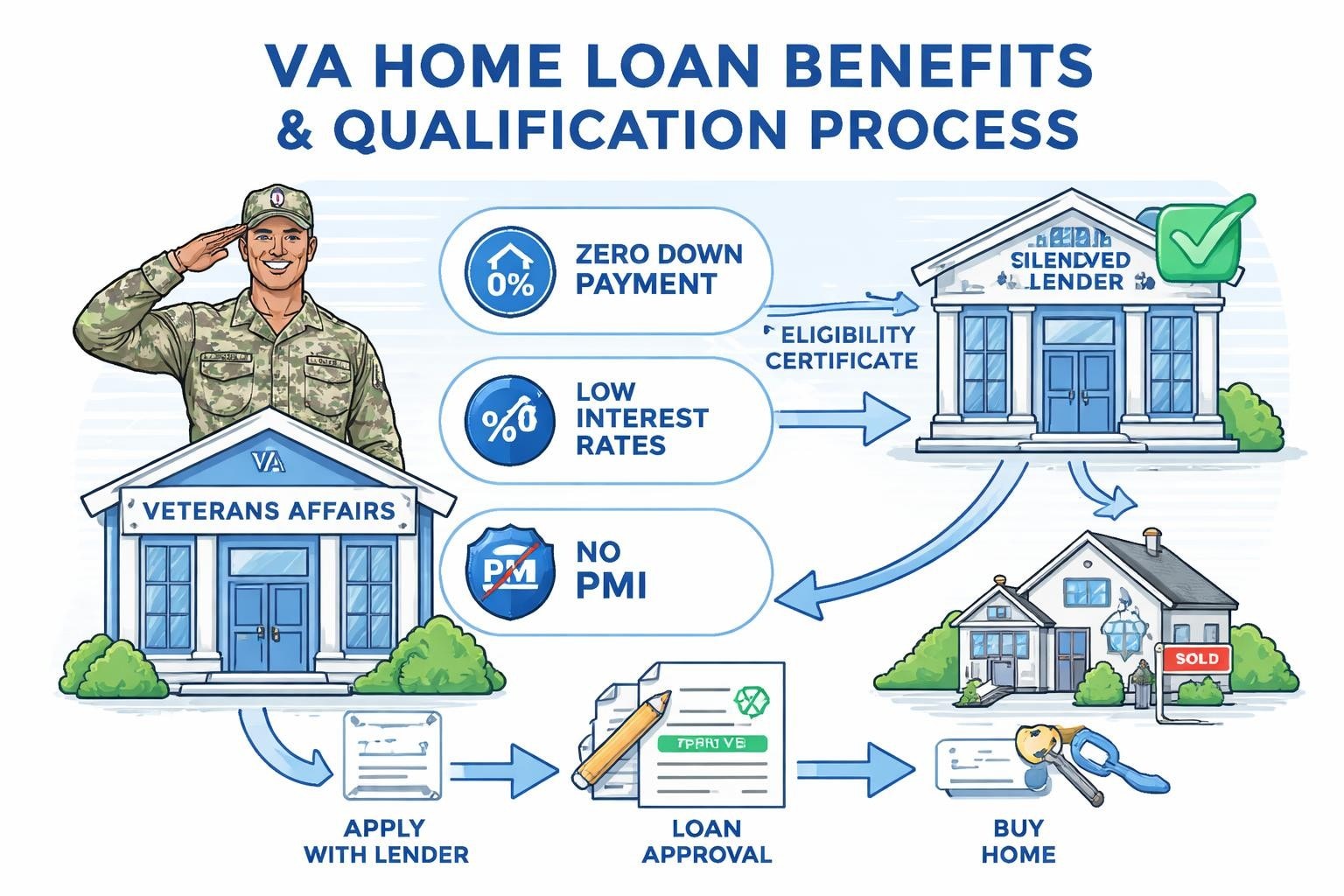

Choosing the appropriate loan program requires understanding both current financial capacity and future plans. The decision between conventional, FHA, VA, or jumbo financing isn't simply about which program accepts your down payment-it's about optimizing costs, flexibility, and long-term value based on your specific situation.

| Loan Type | Minimum Down Payment | Credit Score Minimum | Best For |

|---|---|---|---|

| Conventional | 3% | 620 | Strong credit, various property types |

| FHA | 3.5% | 580 | Lower credit scores, higher DTI ratios |

| VA | 0% | No minimum | Eligible veterans and service members |

| Jumbo | 10-20% | 680+ | High-value properties in Seattle, Bellevue |

Conventional loans offer the most flexibility for properties in Shoreline, Lynnwood, and Lake Forest Park, particularly when you can provide at least 5% down. Those exploring conventional loan options with lower down payments should understand that putting down less than 20% triggers PMI requirements, but this insurance can be removed once you reach 20% equity.

Jumbo Loan Considerations in High-Cost Markets

Seattle's median home prices frequently exceed conforming loan limits, making jumbo financing a necessary topic within comprehensive mortgage education. In 2026, understanding jumbo qualification becomes essential for buyers targeting properties in Bellevue, Redmond, or Kirkland's most desirable neighborhoods.

Jumbo loans require heightened scrutiny in several areas:

- Larger reserve requirements (typically 6-12 months of housing payments)

- More detailed income documentation and verification

- Lower maximum debt-to-income ratios (usually 43% or less)

- Stricter appraisal standards and property condition requirements

Jumbo loan qualification strategies become particularly important when stock compensation forms a significant portion of your income. Lenders evaluate consistency, vesting schedules, and employer stability more rigorously on jumbo transactions.

Pre-Approval Process and Documentation Requirements

A critical component of mortgage education involves understanding the difference between pre-qualification and pre-approval, and knowing which documentation lenders require for full underwriting review. In competitive Seattle markets, a strong pre-approval from a reputable lender can make the difference between winning and losing a bidding situation.

Complete pre-approval documentation typically includes:

- Most recent two years of tax returns (personal and business if self-employed)

- 30 days of pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts

- Two years of W-2 forms or 1099s

- Complete employment verification

- Full credit report authorization

- Explanation letters for any credit issues or large deposits

The home loan approval timeline varies based on documentation complexity and current volume, but working with experienced brokers can significantly expedite the process. Some lenders can now close loans in as few as 9 business days when documentation is complete and property appraisals come back clean.

Credit Score Optimization Before Applying

Understanding how credit scoring works represents an essential piece of mortgage education that many buyers overlook until it's too late. Your credit score affects not only whether you're approved, but what interest rate you'll receive-potentially costing or saving tens of thousands of dollars over the loan's life.

Key actions to optimize your credit score before applying:

- Review all three credit reports (Experian, TransUnion, Equifax) for errors

- Pay down revolving balances below 30% utilization, ideally under 10%

- Avoid opening new credit accounts within six months of applying

- Maintain consistent on-time payment history across all obligations

- Don't close old credit cards unless absolutely necessary

For buyers in Mill Creek or Everett considering their first home purchase, addressing credit issues six months before starting the home search creates significantly better options than trying to repair credit during an active transaction.

Interest Rates, Points, and Cost Analysis

Proper mortgage education must include understanding how interest rates are determined, what factors influence the rate you're quoted, and how paying points affects long-term costs. Many buyers fixate on securing the absolute lowest rate without considering whether that rate requires paying excessive upfront costs that won't be recouped.

Rate determination factors include:

- Overall credit score (both score and credit profile depth)

- Loan-to-value ratio (down payment percentage)

- Property type (single-family, condo, multi-unit, investment)

- Occupancy status (primary residence, second home, investment)

- Loan amount (conforming versus jumbo)

- Rate lock period and market conditions

Understanding current mortgage rates and how they’re structured helps buyers recognize whether paying points makes financial sense for their situation. A point equals 1% of the loan amount and typically reduces your interest rate by approximately 0.25%. If you plan to keep the loan for seven years or more, paying points often makes sense. For shorter timeframes, taking a slightly higher rate with lower upfront costs proves more economical.

Fixed-Rate Versus Adjustable-Rate Mortgages

The choice between fixed and adjustable rates represents a significant decision within mortgage education. Fixed-rate mortgages provide payment stability and protection against rising rates, while adjustable-rate mortgages (ARMs) offer lower initial rates that adjust after a fixed period.

| Feature | 30-Year Fixed | 7/1 ARM | 5/1 ARM |

|---|---|---|---|

| Initial Rate Period | 30 years | 7 years fixed | 5 years fixed |

| Rate Stability | Complete | Adjusts after year 7 | Adjusts after year 5 |

| Initial Rate | Higher | Lower | Lowest |

| Best For | Long-term ownership | 7-10 year ownership | 5-7 year ownership |

For Seattle professionals who anticipate relocating for career opportunities or upgrading within five to seven years, ARMs can provide substantial savings. However, this strategy requires honest assessment of your actual plans and risk tolerance regarding potential rate increases.

Down Payment Sources and Gift Funds

Comprehensive mortgage education addresses where down payment funds can originate and what documentation lenders require for different sources. Many first-time buyers in Seattle don't realize that gift funds from family members are acceptable and even encouraged by most loan programs.

Acceptable down payment sources include:

- Personal savings in checking, savings, or money market accounts

- Proceeds from sale of previous property or other assets

- Gift funds from relatives (parents, grandparents, siblings)

- Employer assistance programs (increasingly common with tech employers)

- Retirement account withdrawals (with restrictions and tax implications)

- Grants and down payment assistance programs for qualifying buyers

Gift funds require specific documentation including a gift letter stating the funds are a gift with no repayment expectation, documentation of the donor's ability to provide the gift, and verification that funds were transferred. For buyers working with a trusted mortgage broker in Seattle, proper gift fund documentation prevents delays during underwriting.

Down Payment Assistance Programs

Seattle and King County offer various down payment assistance programs that many qualified buyers overlook. Proper mortgage education includes awareness of these resources, particularly for first-time buyers or those purchasing in specific neighborhoods.

Programs typically target households earning below area median income, though definitions and limits vary. Some provide grants requiring no repayment, while others structure assistance as deferred second mortgages due only when you sell or refinance. Understanding eligibility requirements and program restrictions forms an important component of complete homebuyer education.

Closing Costs and Cash-to-Close Requirements

Beyond the down payment, understanding total cash-to-close requirements prevents surprises at the closing table. Mortgage education should clearly explain the difference between down payment, closing costs, prepaid items, and required reserves.

Typical closing cost categories include:

- Lender fees (origination, underwriting, processing)

- Third-party fees (appraisal, credit report, title insurance)

- Prepaid items (property taxes, homeowners insurance, prepaid interest)

- Escrow reserves (tax and insurance impounds)

- Recording fees and transfer taxes

In Seattle and surrounding areas, closing costs typically range from 2% to 5% of the purchase price. On a $800,000 home in Bellevue, this translates to $16,000 to $40,000 in addition to your down payment. Understanding these costs early in the process allows proper financial planning.

Many buyers successfully negotiate seller-paid closing costs, particularly in balanced or buyer-favorable markets. However, in competitive situations, asking for seller concessions may weaken your offer compared to buyers paying their own costs.

Professional Guidance and Ongoing Education

While self-education through resources like industry-standard mortgage education platforms provides valuable baseline knowledge, working with an experienced mortgage professional ensures you apply that knowledge correctly to your specific situation. Generic information rarely accounts for the nuances of complex income structures, unique property types, or competitive market conditions.

Benefits of working with an experienced mortgage broker include:

- Access to multiple lenders and loan programs through one application

- Expertise in structuring loans for complex income situations

- Strategic advice on timing, documentation, and offer structuring

- Advocacy throughout the underwriting and closing process

- Problem-solving when unexpected issues arise

The mortgage industry continues evolving, with digital mortgage education and eMortgage technologies changing how applications are submitted, processed, and closed. Staying current on these developments helps buyers understand what to expect during their transaction.

Continuing Your Mortgage Education Journey

Mortgage education shouldn't stop once you close on your first home. Understanding refinancing opportunities, how to build equity faster, and when market conditions favor rate-and-term refinances or cash-out refinances helps you optimize your mortgage over time.

Strategic home buying guidance extends beyond the initial purchase to encompass long-term financial planning. Many homeowners refinance multiple times over their homeownership journey, taking advantage of rate decreases, eliminating PMI once equity reaches 20%, or accessing equity for improvements or investments.

For investors or those considering eventually purchasing rental properties, understanding conventional loans for investment properties becomes relevant as your portfolio expands. Investment property financing requires different down payments, reserves, and qualification calculations than primary residences.

Market-Specific Considerations for Greater Seattle

Mortgage education must account for local market conditions, property values, and economic factors that influence lending in your specific area. Seattle's robust job market, limited housing inventory, and high property values create unique considerations that don't apply in all markets.

Seattle-specific mortgage considerations include:

- Condo financing in high-rise buildings with specific warrantability requirements

- Townhome and planned unit developments with HOA review processes

- Historic homes in neighborhoods like Shoreline requiring specialized appraisals

- New construction financing with builder incentives and phased closings

Understanding these local nuances prevents surprises during the qualification and closing process. What works perfectly for a single-family home in Mill Creek may not apply to a downtown Seattle condo with complex HOA structures.

Working with Local Experts

The value of working with a locally-based mortgage professional who understands Greater Seattle markets cannot be overstated. National online lenders may offer competitive rates, but they rarely provide the market-specific expertise, local appraiser relationships, and hands-on service that complex transactions require.

When evaluating mortgage brokers in the Seattle area, consider their track record, client reviews, responsiveness, and specific experience with your situation-whether that's first-time buyers, tech professionals with stock compensation, or investors building rental portfolios.

Comprehensive mortgage education empowers you to make informed decisions, avoid costly mistakes, and optimize both your home search and financing strategy. Whether you're a first-time buyer navigating the process for the first time or a seasoned homeowner exploring refinancing options, understanding how mortgages work creates confidence and clarity. Keith Akada and the team at Mortgage Reel bring over 25 years of experience helping Seattle-area buyers and homeowners achieve their real estate goals through education-focused guidance, transparent communication, and strategic loan structuring. With specialized expertise in qualifying complex income sources for tech professionals and a proven track record of closing loans efficiently even in competitive markets, Keith provides the personalized support you need to navigate your mortgage journey successfully.