Refinancing your mortgage can unlock significant financial opportunities, from lowering monthly payments to accessing home equity for strategic investments. For Seattle-area homeowners navigating the 2026 refinance market, choosing from the best mortgage companies for refinance requires understanding not just rates but also expertise, speed, and specialized knowledge of local real estate dynamics. Whether you're a tech professional with RSU compensation in Bellevue or a growing family in Shoreline, the right refinance partner makes all the difference in achieving your financial goals.

What Defines the Best Mortgage Companies for Refinance

The mortgage refinance landscape has evolved considerably, with lenders differentiating themselves through technology, specialized programs, and customer service excellence. Top-tier refinance companies share several key characteristics that separate them from average providers.

Speed and efficiency represent critical factors for borrowers who want to capitalize on favorable rate conditions. The best lenders maintain streamlined processes that can close refinances in 15 to 30 days, with exceptional providers completing transactions even faster. Fairway Independent Mortgage Corporation, for instance, offers closings in as few as 9 business days through advanced underwriting systems.

Rate Competitiveness and Transparency

Interest rates remain the primary motivator for refinancing, but the lowest advertised rate doesn't always translate to the best overall value. Understanding when to refinance involves examining the complete cost structure.

Top refinance companies provide:

- Transparent fee structures with itemized closing costs

- Rate lock guarantees protecting borrowers during processing

- Competitive wholesale pricing passed directly to consumers

- Multiple product options tailored to different financial situations

- No hidden junk fees or last-minute cost surprises

The difference between a 6.5% and 6.25% rate on a $750,000 refinance amounts to approximately $140 monthly or $50,400 over 30 years. However, excessive closing costs can negate years of interest savings, making transparent pricing essential.

Types of Refinance Programs Offered by Leading Lenders

Different financial objectives require specialized refinance solutions. The best mortgage companies for refinance maintain diverse product portfolios serving various borrower needs across Seattle, Redmond, and Kirkland markets.

Rate-and-Term Refinancing

This traditional refinance approach focuses exclusively on improving your interest rate or adjusting your loan term. Seattle homeowners often use rate-and-term refinances to reduce monthly payments or accelerate equity building.

Common scenarios include:

- Refinancing from adjustable to fixed rates for payment stability

- Extending loan terms to reduce monthly obligations

- Shortening to 15-year terms to eliminate mortgage debt faster

- Removing private mortgage insurance after reaching 20% equity

For tech professionals in the Greater Seattle area, understanding mortgage financing options becomes particularly important when compensation structures change or career transitions occur.

Cash-Out Refinancing

Cash-out refinances allow homeowners to convert equity into liquid capital while potentially securing better rates. Seattle's strong appreciation rates since 2020 have created substantial equity positions for many homeowners.

Leading cash-out refinance lenders typically permit borrowing up to 80% of current home value. On a $900,000 Bellevue home with $400,000 remaining mortgage balance, this could unlock approximately $320,000 in available cash.

Strategic uses include:

- Home improvement projects increasing property value

- Debt consolidation eliminating high-interest obligations

- Investment property down payments building rental portfolios

- Business capital for entrepreneurial ventures

- Education expenses for family members

Streamline Refinance Options

Government-backed streamline programs offer simplified refinancing for existing FHA, VA, and USDA borrowers. These programs minimize documentation and often waive appraisal requirements.

| Program Type | Key Benefits | Ideal Candidates |

|---|---|---|

| FHA Streamline | Reduced documentation, no appraisal in many cases | Current FHA borrowers with payment history |

| VA IRRRL | No appraisal, minimal credit check, funding fee may be waived | Veterans with existing VA loans |

| USDA Streamline | Lower rates, reduced paperwork | Rural property owners with USDA mortgages |

Veterans throughout the Seattle region particularly benefit from VA streamline options. Learn more about VA loan benefits and qualifications specific to Washington state.

Evaluating Lender Expertise and Service Quality

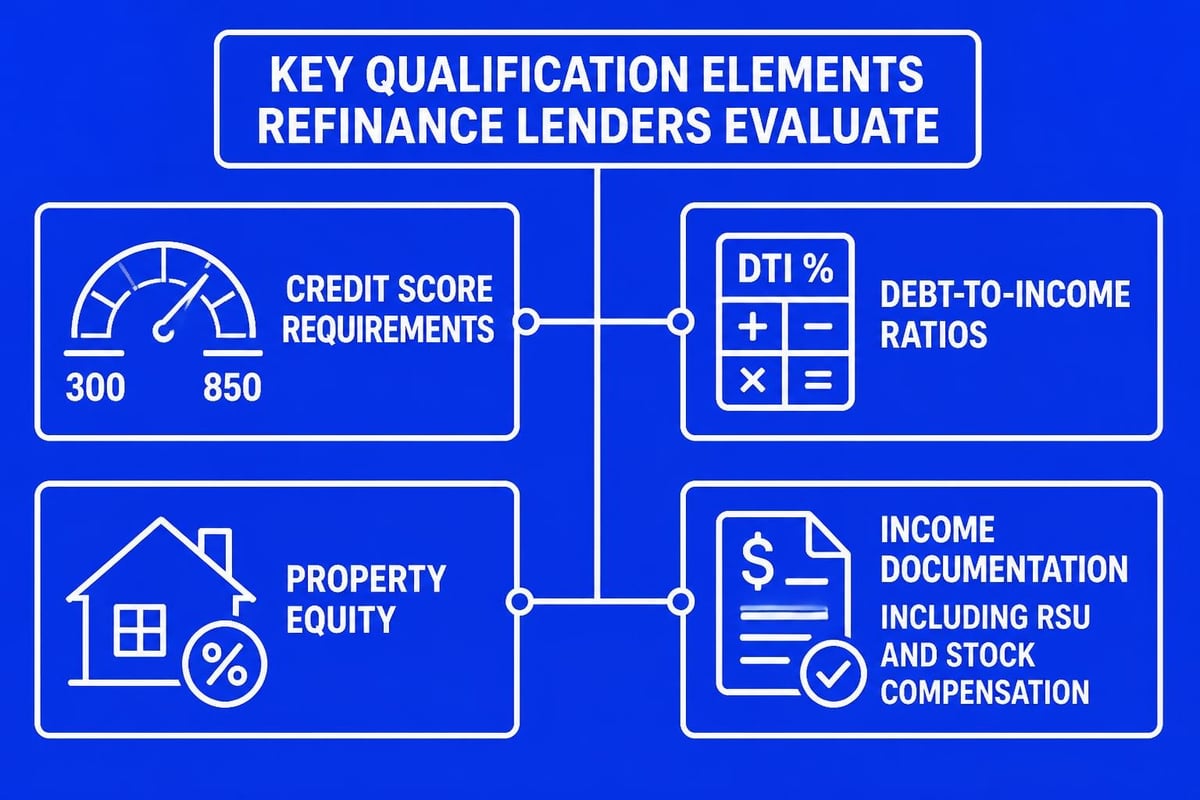

Beyond rates and programs, the best mortgage companies for refinance distinguish themselves through specialized knowledge and execution excellence. This becomes especially important in complex scenarios involving non-traditional income or high-balance loans.

Specialized Income Qualification

Seattle's concentration of technology employers creates unique refinancing challenges. Amazon, Microsoft, and Google employees often receive significant compensation through restricted stock units (RSUs), performance bonuses, and equity grants.

Top refinance specialists understand how to:

- Document and qualify RSU income for debt-to-income calculations

- Average variable compensation over appropriate timeframes

- Project future vesting schedules for qualification purposes

- Navigate underwriting guidelines for stock-based compensation

- Maximize borrowing power for jumbo loan scenarios

Working with lenders experienced in jumbo home loans in Washington State ensures proper handling of loans exceeding conventional conforming limits of $806,500 in 2026.

Customer Service and Communication

The refinance process involves substantial documentation, strict timelines, and coordinating multiple parties. Exceptional lenders maintain proactive communication throughout.

Responsive communication channels include direct loan officer access, dedicated processing teams, and real-time status updates. Borrowers should expect replies within business hours and clear explanations of requirements.

Educational approach separates top professionals from transactional lenders. The best mortgage companies for refinance invest time explaining options, running comparison scenarios, and helping clients understand long-term implications of different strategies.

Technology and Digital Experience

Modern refinance companies leverage technology to enhance speed, accuracy, and borrower convenience. Digital-first platforms have transformed application and tracking processes.

Leading technological capabilities include:

- Online applications capturing complete borrower profiles efficiently

- Digital document upload eliminating mailing delays

- Automated underwriting systems providing faster initial decisions

- E-signature capabilities streamlining approval workflows

- Mobile apps offering 24/7 loan status visibility

However, technology should complement rather than replace human expertise. The ideal combination pairs digital efficiency with experienced guidance, particularly for complex Seattle-area refinances involving high property values or sophisticated income structures.

Geographic Expertise and Local Market Knowledge

National lenders may offer competitive rates, but local market expertise provides distinct advantages. Understanding the benefits of choosing a local Seattle lender includes faster processing, regional property knowledge, and established relationships with area appraisers and title companies.

Seattle Metro Real Estate Dynamics

Property values across Seattle submarkets vary significantly. A Capitol Hill condominium presents different refinance considerations than a Shoreline single-family home or Lake Forest Park waterfront property.

Local refinance specialists understand:

- Neighborhood appreciation patterns affecting equity positions

- Condo association requirements impacting qualification

- Appraisal challenges in unique Seattle neighborhoods

- Title issues common to older properties

- Environmental considerations for waterfront or hillside homes

For homeowners exploring opportunities in specific areas, resources like the Lake Forest Park housing market guide provide valuable market context for refinance timing decisions.

Processing Speed Advantages

Proximity enables faster processing through established local networks. When appraisals, title work, and inspections involve familiar regional partners, coordination happens more efficiently than with distant national operations.

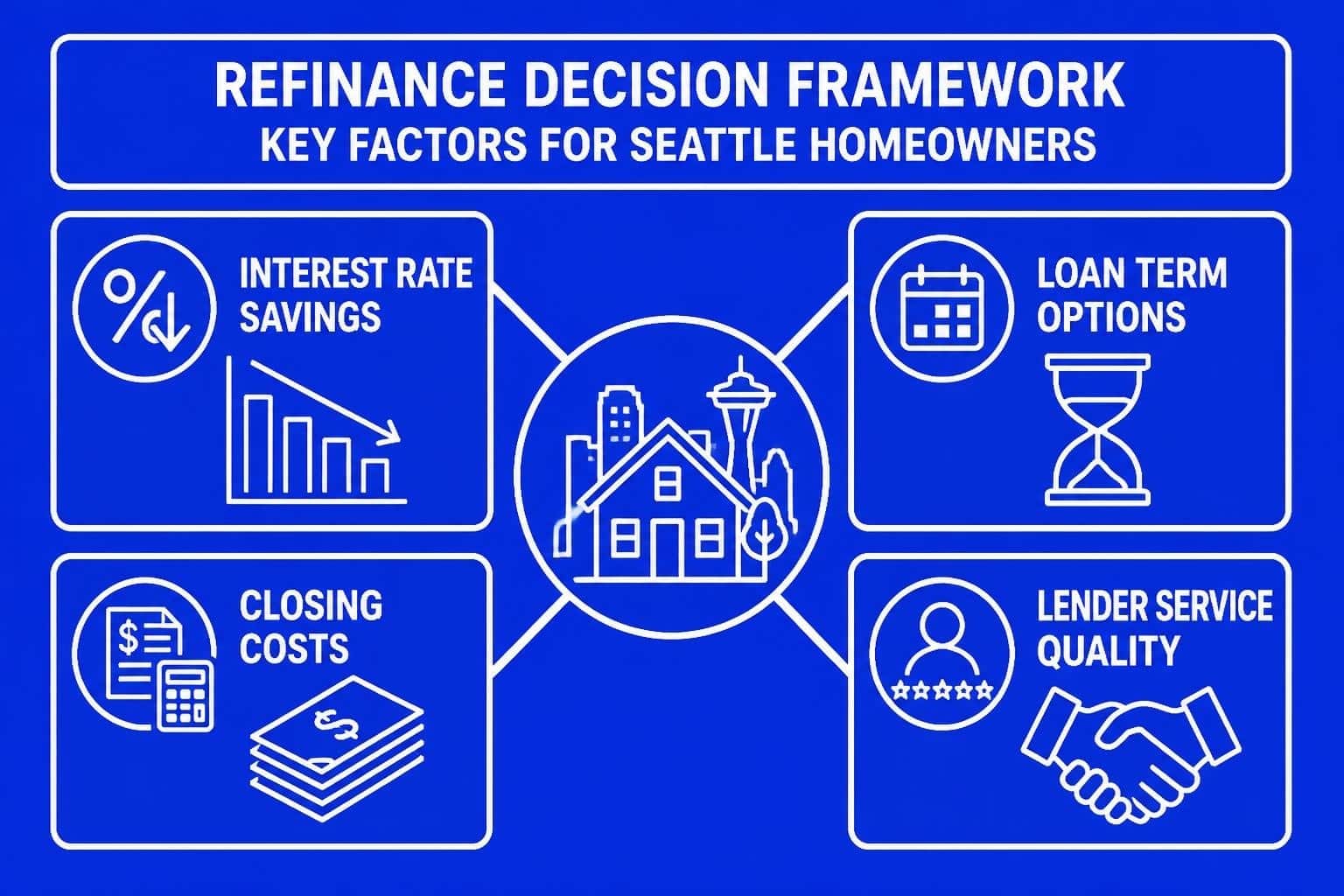

Critical Factors in Refinance Decision-Making

Selecting from the best mortgage companies for refinance requires analyzing multiple variables beyond advertised rates. Strategic decision-making considers both immediate costs and long-term financial impact.

Break-Even Analysis

Every refinance involves upfront costs that must be recovered through monthly savings. Understanding your break-even timeline prevents financially counterproductive refinances.

Calculate break-even by dividing total closing costs by monthly payment reduction:

Example: $6,000 closing costs ÷ $250 monthly savings = 24 months break-even

If you plan to remain in your Seattle home beyond the break-even period, refinancing likely makes financial sense. Conversely, homeowners planning to relocate within two years might reconsider despite attractive rates.

Loan Term Considerations

Resetting to a new 30-year mortgage extends your debt timeline and increases total interest paid, even at lower rates. Strategic borrowers often refinance to shorter terms when monthly budgets allow.

| Current Situation | Refinance Option | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| $500,000 at 7.0%, 25 years remaining | New 30-year at 6.25% | $3,078 | $608,080 |

| $500,000 at 7.0%, 25 years remaining | New 25-year at 6.25% | $3,276 | $483,000 |

| $500,000 at 7.0%, 25 years remaining | New 15-year at 6.0% | $4,219 | $259,420 |

The 15-year option saves $348,660 in interest compared to the 30-year refinance, though monthly payments increase by $1,141. Understanding how refinancing works helps homeowners evaluate these tradeoffs effectively.

Closing Cost Structures

Refinance closing costs typically range from 2% to 5% of loan amount. Detailed understanding prevents surprises and enables accurate comparison shopping.

Common closing cost components:

- Origination fees (0.5% to 1.5% of loan amount)

- Appraisal costs ($500 to $900 in Seattle metro)

- Title insurance and search ($1,000 to $2,500)

- Credit report fees ($30 to $100)

- Recording fees (varies by county)

- Prepaid interest and escrow items

Some lenders offer no-closing-cost refinances by incorporating fees into higher interest rates. While this eliminates upfront expenses, it increases long-term costs and may not suit borrowers planning extended homeownership.

Preparing for a Successful Refinance Application

The best mortgage companies for refinance appreciate well-prepared borrowers. Advance preparation accelerates processing and improves approval likelihood.

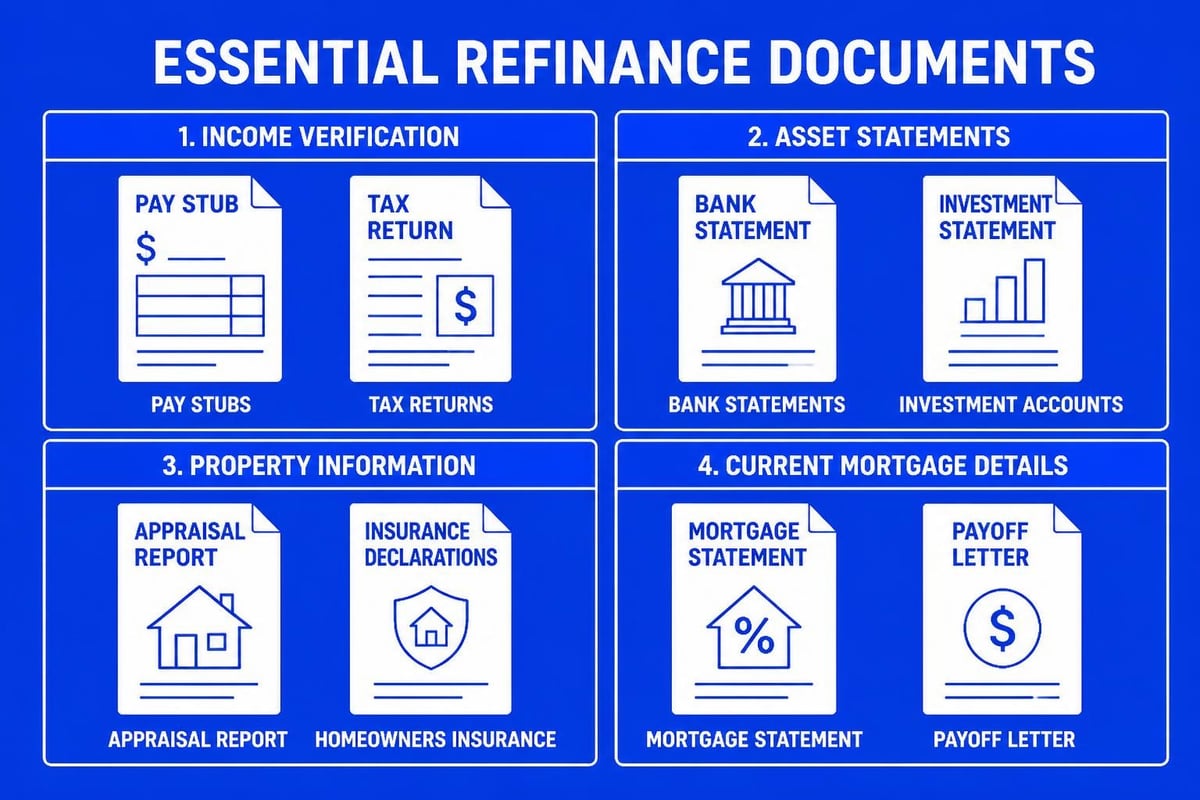

Documentation Requirements

Complete documentation packages enable faster underwriting decisions. Gather materials before initiating applications:

Income verification includes recent pay stubs covering 30 days, W-2 forms from the past two years, and complete tax returns with schedules. Self-employed borrowers need two years of business tax returns and year-to-date profit/loss statements.

Asset documentation requires recent statements for all bank accounts, retirement accounts, and investment portfolios. Document any large deposits with source explanations.

Property information encompasses current mortgage statements, homeowners insurance declarations, property tax bills, and HOA documentation if applicable.

For tech professionals with complex compensation, additional documentation might include RSU vesting schedules, equity grant letters, and bonus history. Experienced mortgage brokers in Seattle guide clients through specialized documentation requirements.

Credit Profile Optimization

While refinancing typically requires less stringent credit standards than purchase mortgages, stronger profiles unlock better rates. Conventional refinances generally require minimum 620 credit scores, though 740+ scores access optimal pricing.

Credit improvement strategies:

- Review credit reports for errors requiring dispute

- Pay down revolving balances below 30% utilization

- Avoid new credit applications during refinance process

- Maintain current payment status on all obligations

- Address collections or judgments proactively

Even modest credit score improvements from 680 to 720 can reduce rates by 0.25% to 0.375%, creating substantial long-term savings on Seattle-area home values.

Special Considerations for Seattle-Area Refinances

The Greater Seattle market presents unique refinance opportunities and challenges requiring specialized approaches.

High-Balance and Jumbo Refinancing

Seattle's elevated property values frequently push refinances into jumbo territory. Loans exceeding $806,500 in 2026 require jumbo financing with distinct qualification standards.

Jumbo refinance requirements typically include:

- Higher credit scores (typically 700+ minimum, 740+ preferred)

- Lower debt-to-income ratios (usually 43% maximum)

- Larger reserve requirements (6 to 12 months payments)

- Comprehensive income documentation

- Higher equity positions (often 20%+ required)

Specialized jumbo lenders understand nuances of qualifying for jumbo loans with stock-based compensation and variable income common among Seattle tech professionals.

Condo Refinancing Complexities

Seattle's significant condominium inventory introduces additional refinance considerations. Lender condo approval requires HOA financial health verification, sufficient owner-occupancy ratios, and adequate reserve funds.

Warrantable versus non-warrantable designation affects rate and availability. Non-warrantable condos (those not meeting Fannie Mae/Freddie Mac standards) require specialized lenders and typically carry higher rates.

Investment Property Refinancing

Seattle's strong rental market attracts real estate investors managing multiple properties. Investment property refinances involve stricter qualification and higher rates than primary residences.

Key differences include:

- Higher interest rates (typically 0.5% to 0.875% above primary residence rates)

- Larger down payment requirements (25% to 30% equity minimum)

- Rental income verification through lease agreements and tax returns

- Reserve requirements covering 6+ months of payments across all investment properties

Navigating the Refinance Process From Application to Closing

Understanding the complete refinance process helps borrowers anticipate requirements and timelines.

Initial Consultation and Rate Shopping

Begin by consulting multiple lenders to compare rates, fees, and service approaches. Provide consistent financial information enabling accurate rate quotes. Request Loan Estimates within three business days of application for transparent comparison.

During consultations, ask about:

- Current rate environment and lock strategies

- Specific programs matching your situation

- Estimated closing timeline

- Communication processes and points of contact

- Lender experience with your property type and location

Application and Documentation Phase

Complete applications trigger formal processing. Submit all requested documentation promptly to avoid delays. Lenders verify employment, income, assets, and credit during this phase.

Underwriting review evaluates risk and ensures guideline compliance. Automated underwriting systems provide initial approvals within hours, though manual review follows for complex scenarios.

Appraisal scheduling occurs after initial approval. Seattle-area appraisals typically complete within 7 to 14 days depending on property type and location. Appraisers assess current market value confirming adequate equity for refinance terms.

Closing Preparation and Funding

Final approval triggers closing preparation. Review Closing Disclosures carefully, comparing fees to initial estimates. Federal law requires three-day waiting periods after receiving Closing Disclosures before funding.

Title work ensures clear ownership and identifies any liens requiring payoff. Title insurance protects against future ownership disputes.

Closing appointments can occur in-person or through mobile notary services. Bring government-issued identification and any required certified funds for closing costs exceeding escrow account credits.

Most refinances fund within 24 hours of closing, with existing mortgages paying off and new terms taking effect.

Common Refinance Mistakes to Avoid

Even experienced homeowners make costly errors during refinancing. Awareness prevents common pitfalls.

Focusing exclusively on interest rates while ignoring closing costs, loan terms, and service quality creates false economies. A slightly higher rate with dramatically lower fees often provides better value.

Neglecting to shop multiple lenders costs thousands through missed rate and fee competition. Obtain at least three Loan Estimates comparing total costs, not just interest rates.

Extending loan terms repeatedly through serial refinancing keeps borrowers perpetually in debt. Consider the risks of mortgage term resets before pursuing rate reductions that restart amortization.

Withdrawing excessive equity through cash-out refinances for non-appreciating purchases jeopardizes financial security. Reserve equity access for strategic investments, not consumption.

Timing refinances poorly relative to planned home sales wastes closing costs that won't be recovered. Ensure break-even periods align with ownership timelines.

Finding the Right Refinance Partner in Seattle

The best mortgage companies for refinance combine competitive pricing, specialized expertise, responsive service, and local market knowledge. For Seattle-area homeowners, these factors create measurably better outcomes.

Evaluate potential lenders through:

- Online reviews across multiple platforms (Google, Zillow, Yelp)

- Licensing verification through Washington State Department of Financial Institutions

- Product availability matching your specific needs

- Communication style during initial consultations

- Processing capabilities and typical closing timelines

National online lenders may advertise attractive rates but often lack expertise in complex scenarios involving jumbo loans, stock compensation, or unique Seattle property types. Conversely, local specialists understand regional nuances while maintaining competitive pricing through efficient operations.

For comprehensive guidance tailored to Seattle, Bellevue, Redmond, Kirkland, Shoreline, and surrounding areas, experienced professionals provide education-focused consultations examining all refinance options. Whether pursuing rate reduction, equity access, or loan restructuring, strategic refinancing requires analyzing your complete financial picture against current market conditions.

Selecting from the best mortgage companies for refinance in 2026 requires balancing rates, service quality, and specialized expertise matching your unique situation. Seattle-area homeowners benefit from working with experienced local professionals who understand regional property markets, tech industry compensation structures, and efficient processing timelines. Keith Akada and the team at Mortgage Reel bring 25+ years of expertise helping Seattle homeowners achieve refinance goals through transparent guidance, competitive pricing, and execution excellence backed by 750+ five-star reviews. Whether you're refinancing a Bellevue jumbo loan or optimizing your Capitol Hill mortgage terms, strategic professional guidance ensures confident, informed decisions that strengthen your long-term financial position.