Selecting the right financing partner represents one of the most critical decisions in your homebuying journey, particularly in competitive markets like Seattle, Bellevue, and Redmond. Conventional loan lenders offer the most widely used mortgage products in the United States, and understanding how these lenders operate, what they require, and how to maximize your approval odds can save you thousands of dollars while positioning you for success. Unlike government-backed options, conventional loans follow guidelines established by Fannie Mae and Freddie Mac, giving lenders specific parameters for evaluating borrowers. For tech professionals at Amazon, Microsoft, and Google, working with experienced conventional loan lenders who understand stock compensation, RSUs, and complex income scenarios becomes even more essential.

Understanding How Conventional Loan Lenders Evaluate Borrowers

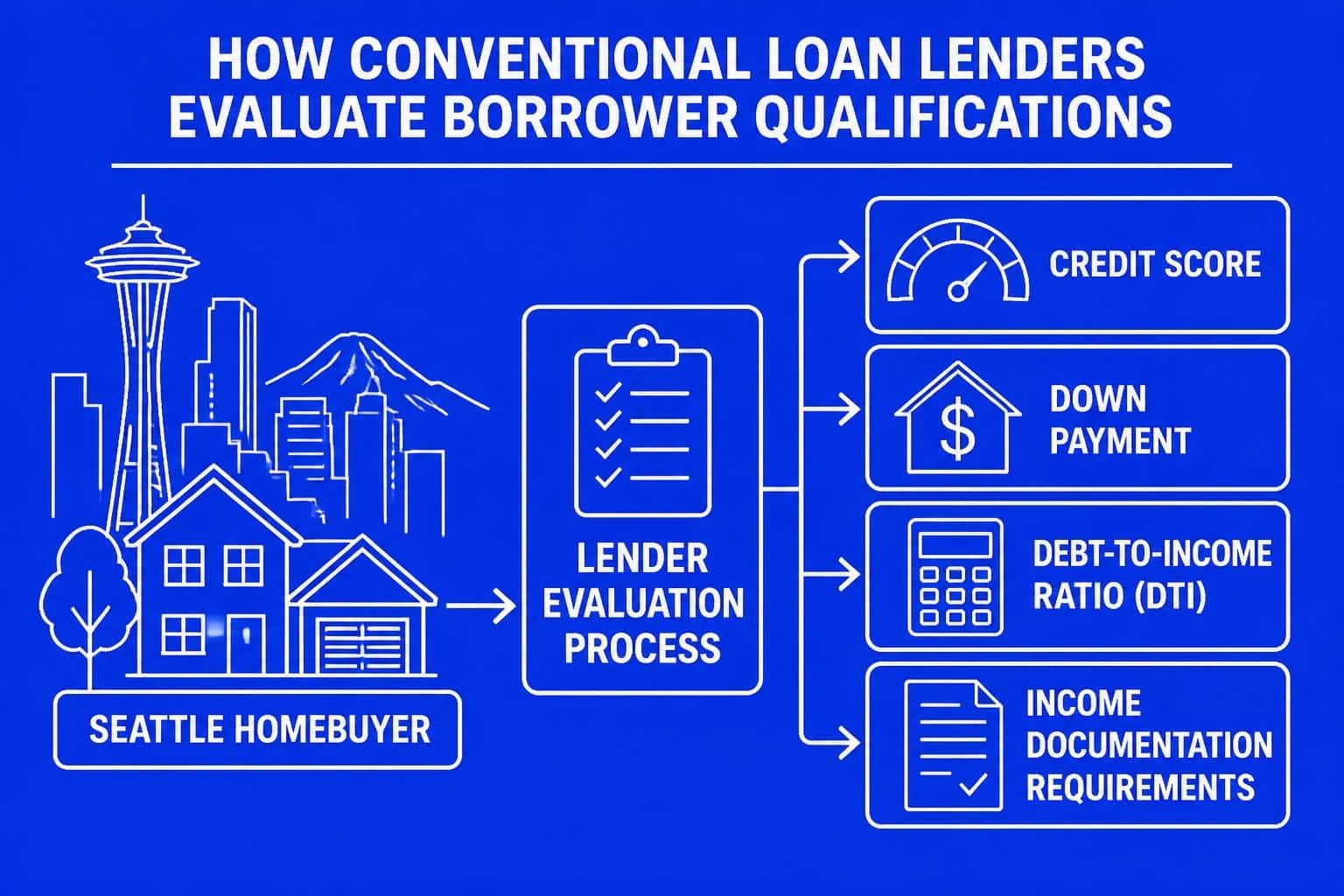

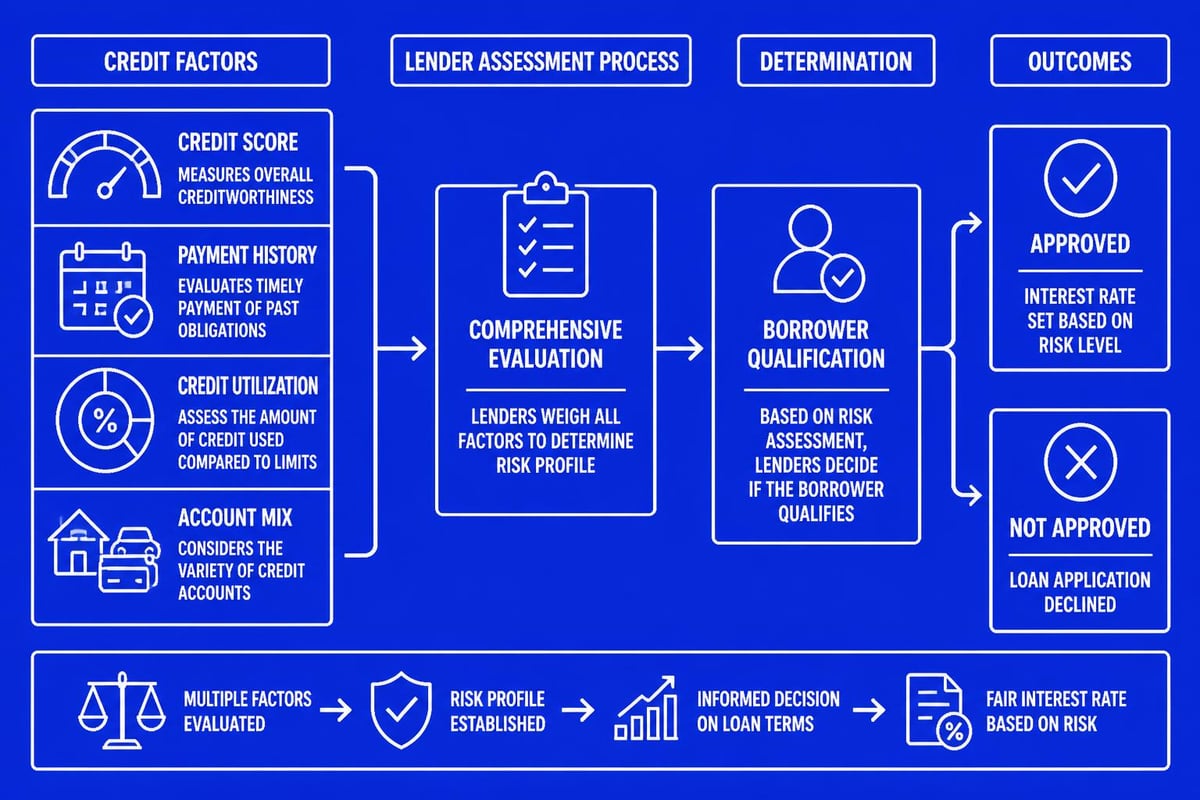

Conventional loan lenders assess your application through a standardized framework that balances risk with opportunity. The Consumer Financial Protection Bureau outlines the fundamental characteristics that distinguish conventional loans from government programs.

Credit Score Requirements and Impact

Your credit profile serves as the foundation of any conventional loan approval. Most conventional loan lenders require a minimum score of 620, though competitive rates typically begin at 680 or higher.

Credit score tiers and their impact:

- 740 and above: Best available rates and terms

- 700-739: Excellent rates with minimal rate adjustments

- 680-699: Good rates with modest pricing adjustments

- 660-679: Higher rates but still competitive

- 620-659: Approval possible but with significant rate premiums

Higher scores don't just unlock approval-they reduce your interest rate, potentially saving tens of thousands over the loan term. In the Seattle market, where home prices average $850,000 to $1.2 million in desirable neighborhoods, even a 0.25% rate difference translates to substantial monthly savings.

Down Payment Standards Across Lender Types

Conventional loan lenders offer flexibility that many borrowers overlook. While the traditional standard suggests 20% down, you can secure approval with as little as 3% down on qualifying conventional loan programs.

| Down Payment | PMI Requirement | Best For |

|---|---|---|

| 3-5% | Required | First-time buyers, those preserving cash |

| 10-15% | Required | Buyers balancing liquidity and equity |

| 20%+ | Not required | Those avoiding PMI, building instant equity |

For tech professionals in Bellevue and Redmond with substantial RSU packages, the decision between larger down payments and preserving liquid investments requires careful analysis. Many sophisticated borrowers choose smaller down payments to maintain stock positions that historically outperform real estate appreciation.

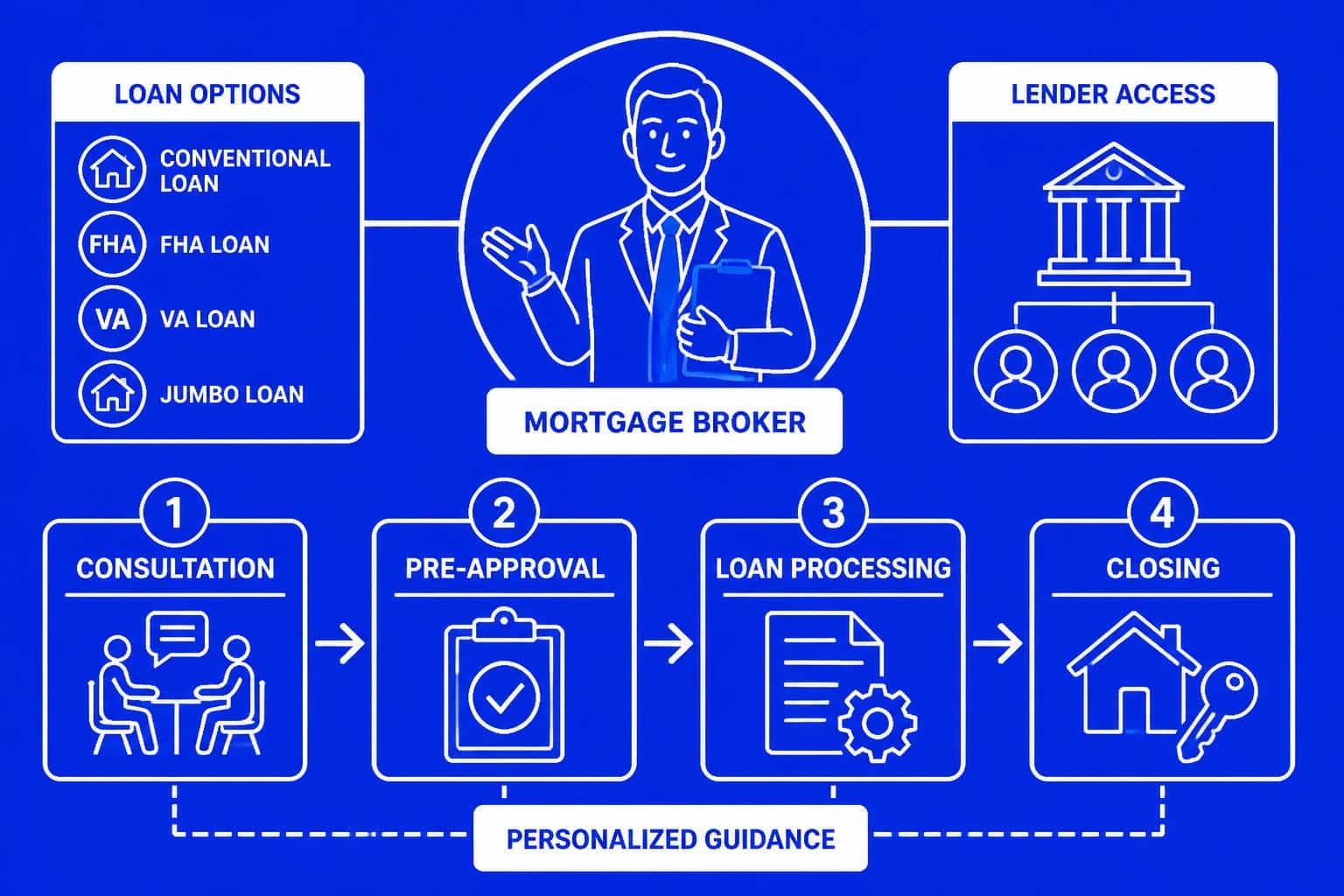

Types of Conventional Loan Lenders in the Seattle Market

Not all conventional loan lenders operate with the same structure, speed, or service model. Understanding these distinctions helps you select the partner aligned with your priorities.

Mortgage Brokers vs. Direct Lenders

Mortgage brokers work with multiple wholesale lenders, comparing options to find optimal terms for your situation. Direct lenders fund loans using their own capital and guidelines. Each model offers distinct advantages.

Mortgage broker benefits:

- Access to multiple lender programs and pricing

- Ability to match complex income scenarios with specialized lenders

- Advocacy throughout the process

- Competitive rate shopping built into the service

Direct lender benefits:

- Streamlined communication within one organization

- Potential for faster processing in simple scenarios

- Direct relationship with underwriting team

For Seattle mortgage borrowers with straightforward W2 income and strong credit, either path works well. But for buyers with stock compensation, self-employment income, or investment property portfolios, broker access to specialized conventional loan lenders proves invaluable.

Credit Unions and Community Banks

Regional financial institutions often provide competitive conventional loan products with relationship-based service. Credit unions in Shoreline and Lake Forest Park may offer rate discounts to members, though their underwriting timelines typically run longer than specialized mortgage lenders.

These lenders excel with borrowers who value personal relationships and don't face tight closing deadlines. However, their limited product menus and slower turnaround times create challenges in competitive Seattle-area markets where sellers expect 21-30 day closings.

National Lenders and Online Platforms

Large national lenders bring scale, technology, and brand recognition. Online platforms automate portions of the application process, appealing to tech-savvy borrowers comfortable with digital interactions.

Considerations with national platforms:

- Potentially lower rates due to volume efficiencies

- Less personalized service and local market knowledge

- Automated systems that struggle with non-traditional income

- Limited ability to problem-solve unique scenarios

In markets like Mill Creek and Everett, where home prices span wide ranges and buyer profiles vary dramatically, the one-size-fits-all approach of many national conventional loan lenders creates approval challenges.

Conventional Loan Products and Program Options

Conventional loan lenders offer multiple product structures designed for different borrower needs and property types. Understanding these options helps you select financing aligned with your long-term strategy.

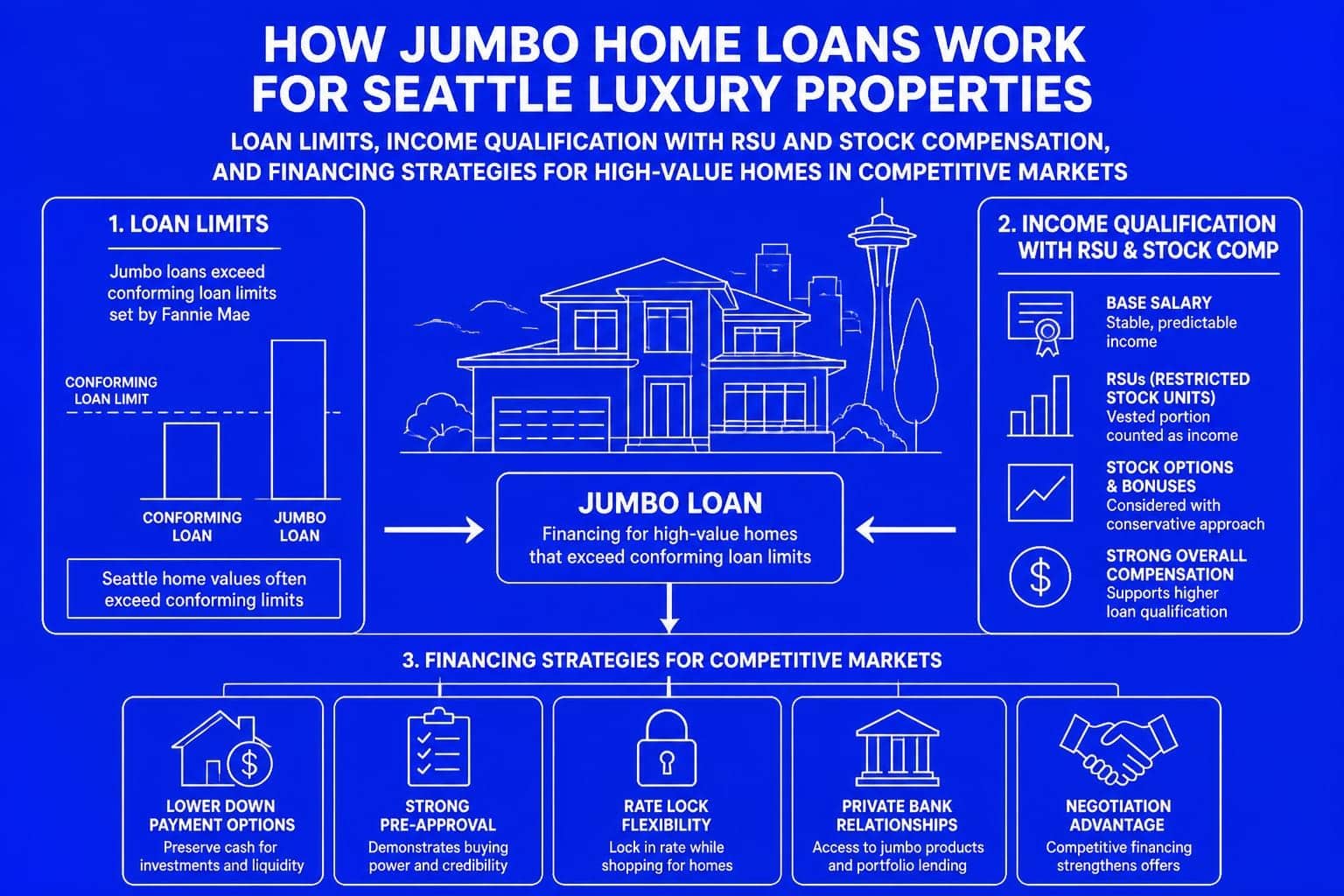

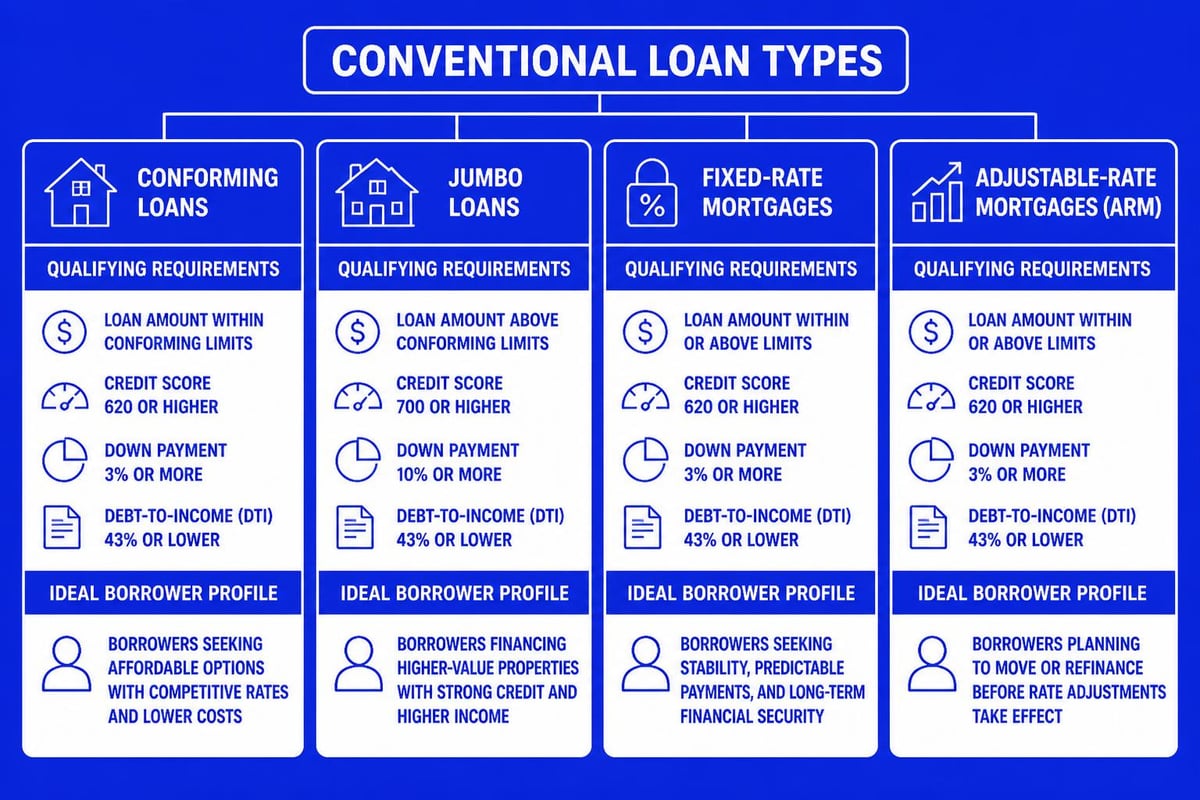

Conforming vs. Non-Conforming Conventional Loans

Conforming loans stay within Fannie Mae and Freddie Mac limits-$806,500 for single-family homes in most Washington State counties in 2026, with higher limits in King County at $1,209,750. These loans receive the most favorable rates and broadest lender participation.

Non-conforming conventional loans, commonly called jumbo loans, exceed these limits and require additional documentation and reserves. In Seattle neighborhoods like Madison Park, Laurelhurst, and Queen Anne, where median prices frequently exceed conforming limits, jumbo loan expertise becomes essential.

Jumbo loan requirements typically include:

- Credit scores of 700 or higher

- Debt-to-income ratios below 43%

- Reserves of 6-12 months PITI

- Comprehensive income documentation

- Property appraisals with additional scrutiny

Fixed-Rate vs. Adjustable-Rate Mortgages

Conventional loan lenders structure products with either fixed interest rates for the entire term or adjustable rates that change after an initial fixed period.

Fixed-rate conventional loans:

- 15-year terms: Higher payments, substantial interest savings

- 20-year terms: Balanced approach gaining popularity

- 30-year terms: Maximum affordability and payment stability

Adjustable-rate mortgages (ARMs):

- 5/1, 7/1, 10/1 structures with fixed periods before adjustment

- Lower initial rates than fixed products

- Interest rate caps limiting adjustment amounts

- Best for borrowers planning to sell or refinance before adjustment

Tech professionals relocating to Seattle often prefer ARMs when they anticipate job changes, stock liquidity events, or geographic moves within 5-7 years. The initial rate savings can be substantial, particularly on jumbo loans.

Qualifying Complex Income with Conventional Loan Lenders

Seattle's concentration of technology employers creates unique income qualification challenges. Not all conventional loan lenders possess equal expertise in documenting RSUs, stock options, bonuses, and equity compensation.

RSU and Stock Compensation Qualification

Restricted Stock Units vest over time, creating income that conventional loan lenders can use for qualification-if they understand the documentation requirements. Most lenders average the past two years of vested RSU income and include it in your qualifying calculation.

Required documentation:

- Two years of W2s showing RSU income

- Recent pay stubs reflecting current vesting schedule

- Equity award statements showing future vesting

- Tax returns documenting stock income

Lenders experienced with Amazon and Microsoft employees in Redmond and Bellevue understand that RSU income often comprises 30-50% of total compensation. Failing to qualify this income properly can reduce your buying power by hundreds of thousands of dollars.

Bonus Income and Commission Documentation

Annual bonuses and commission income require two-year histories for conventional loan lenders to include them in qualification. The lender averages the past 24 months and projects that average forward, assuming continued employment.

Borrowers receiving inconsistent or declining bonuses may face reduced qualifying income. Conversely, those with increasing bonus trajectories benefit from the averaging methodology. Working with experienced mortgage professionals ensures optimal income calculation.

Self-Employment Income Strategies

Self-employed borrowers present documentation challenges that separate sophisticated conventional loan lenders from those lacking expertise. Tax returns showing business deductions reduce qualifying income, creating tension between tax efficiency and mortgage qualification.

| Income Type | Documentation Required | Qualification Method |

|---|---|---|

| W2 Employment | Pay stubs, W2s, VOE | Current income projected forward |

| Self-Employment | 2 years tax returns, P&L, 1099s | Average net income after expenses |

| RSU/Stock | W2s, vesting schedule, equity docs | 2-year average of vested income |

| Rental Income | Lease agreements, tax Schedule E | 75% of gross rent minus PITIA |

Private Mortgage Insurance and How Lenders Apply It

When you provide less than 20% down payment, conventional loan lenders require Private Mortgage Insurance (PMI) to protect against default risk. Understanding PMI costs and removal strategies helps you make informed down payment decisions.

PMI Cost Structures and Payment Methods

PMI typically costs 0.3% to 1.5% of the original loan amount annually, divided into monthly payments added to your mortgage payment. The exact rate depends on your credit score, loan-to-value ratio, and whether you choose borrower-paid or lender-paid options.

PMI payment structures:

- Borrower-paid monthly: PMI added to monthly payment, removable at 78% LTV

- Single premium: One-time upfront payment, often financed into loan

- Lender-paid: Higher interest rate in exchange for no separate PMI payment

- Split premium: Combination of upfront and monthly payments

For a $750,000 home in Lynnwood with 10% down, monthly PMI might range from $225 to $450 depending on your credit profile. Over time, this adds significant cost, making the 20% threshold attractive for many borrowers.

Removing PMI from Conventional Loans

Unlike FHA loans where mortgage insurance remains for the loan life, conventional loan lenders must remove PMI when you reach 78% loan-to-value through scheduled payments. You can also request removal at 80% LTV with a current appraisal.

In Seattle's appreciating market, many homeowners reach 80% LTV through property appreciation rather than principal reduction. Requesting PMI removal after 2-3 years of moderate appreciation can eliminate hundreds in monthly costs.

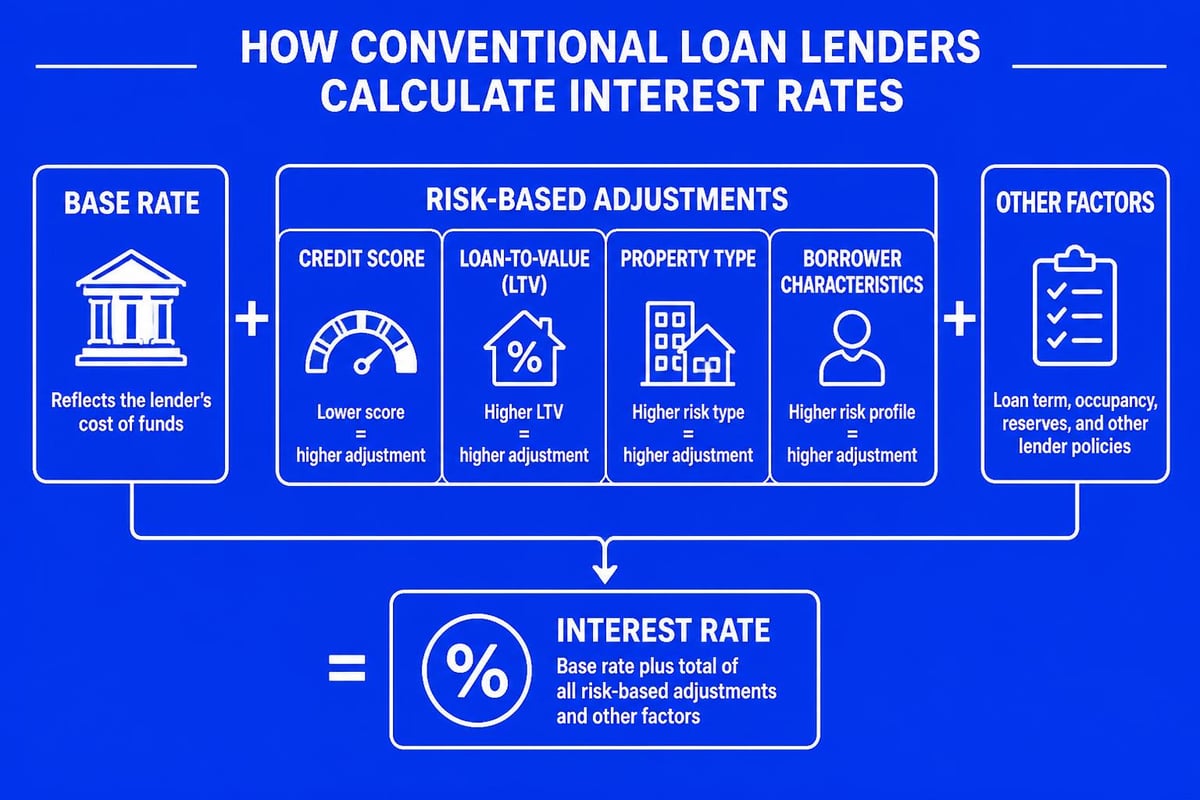

Interest Rates and How Different Lenders Price Loans

Conventional loan lenders price mortgages based on risk assessment, operational costs, and profit margins. Understanding these factors helps you negotiate effectively and recognize competitive offers.

Rate Components and Adjustment Factors

Your interest rate comprises the base rate plus adjustments for credit score, loan-to-value ratio, property type, occupancy, and loan amount. NerdWallet explains how these factors combine to determine your final rate.

Common rate adjustments:

- Credit score below 740: +0.125% to +1.50%

- LTV above 80%: +0.125% to +0.500%

- Investment property: +0.500% to +1.000%

- Condo vs. single-family: +0.125% to +0.250%

- Loan amount under $150,000: +0.250% to +0.500%

For a borrower with 720 credit score, 10% down, purchasing a Seattle condo, total adjustments might add 0.75% to the base rate. Understanding these mechanics helps you identify whether rate quotes reflect accurate pricing.

Discount Points and Rate Buydowns

Conventional loan lenders offer discount points-upfront payments that permanently reduce your interest rate. Each point costs 1% of the loan amount and typically reduces your rate by 0.25%.

When points make financial sense:

- You plan to keep the loan longer than the breakeven period

- Current rates are higher than you expect future rates to be

- You have excess cash and limited tax deductions

- You're maximizing long-term interest savings over payment flexibility

For tech professionals in Bellevue and Kirkland with substantial RSU vesting events, using one-time stock income to buy down rates on large conventional loans creates permanent payment savings.

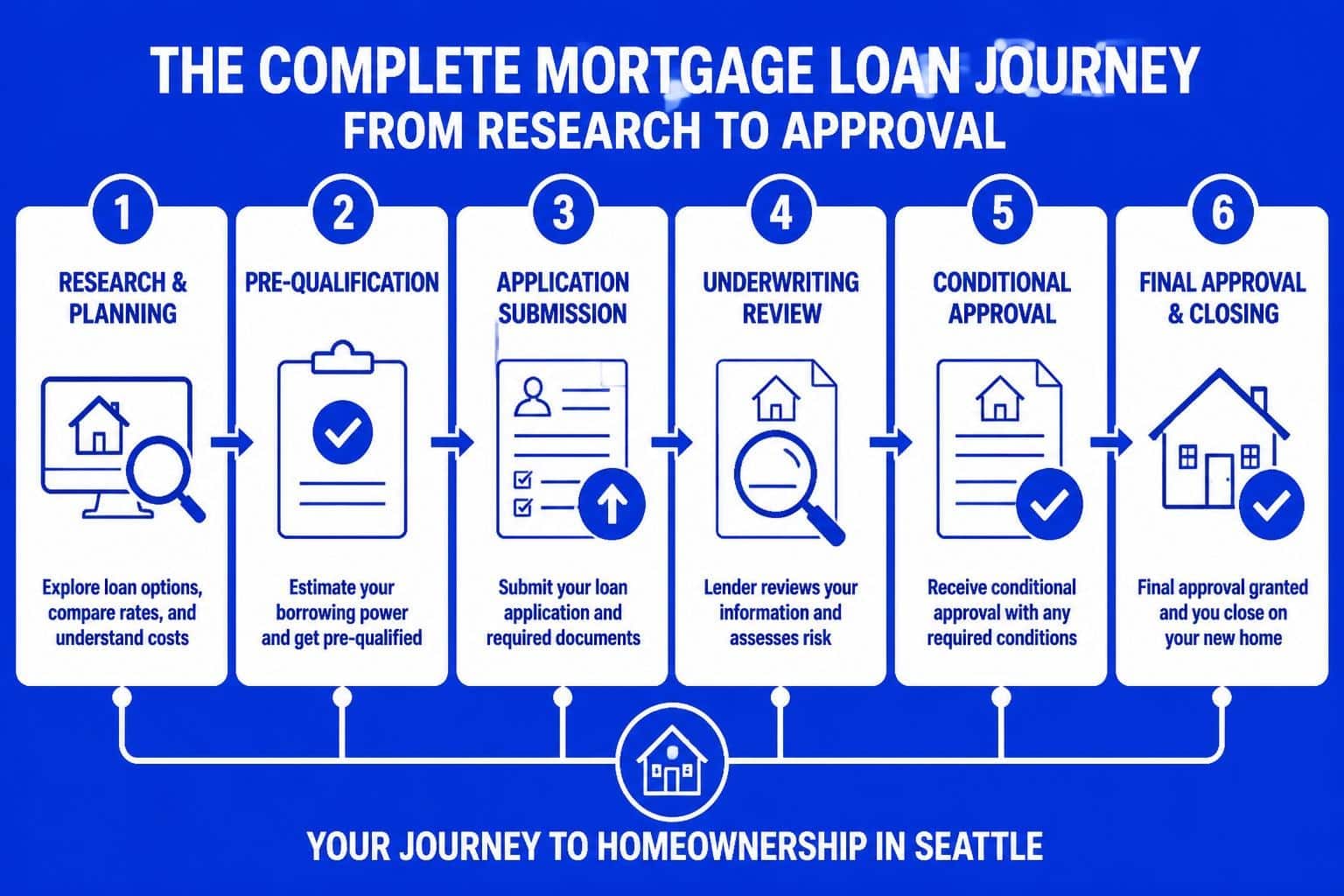

Timeline and Process with Conventional Loan Lenders

Understanding the conventional loan timeline helps you set realistic expectations and coordinate with real estate agents, sellers, and moving schedules. Processing speed varies dramatically between lenders.

Application to Approval Timeline

Most conventional loan lenders complete underwriting within 7-21 business days, though this varies based on complexity, documentation completeness, and lender capacity.

Standard conventional loan timeline:

- Pre-approval (1-2 days): Initial credit review and documentation

- Purchase agreement executed: Submit complete application

- Processing (3-5 days): Document collection and verification

- Underwriting (5-10 days): Detailed file review and conditions

- Approval to clear-to-close (2-5 days): Final condition satisfaction

- Closing (1 day): Document signing and funding

Experienced lenders with efficient processes close conventional loans in 15-21 days routinely. Some specialized lenders offer expedited timelines as short as 9 business days for well-documented borrowers with strong profiles.

Documentation Requirements and Preparation

Conventional loan lenders require comprehensive documentation verifying income, assets, employment, and identity. Preparing these documents before application accelerates processing.

Standard documentation checklist:

- Last 2 years W2s and tax returns

- Most recent 30 days pay stubs

- 2 months bank statements for all accounts

- Retirement account statements if using for reserves

- Gift letter and donor bank statements if applicable

- Purchase agreement and any addendums

- Homeowners insurance quote

- Driver's license and Social Security card

For self-employed borrowers or those with complex income, additional documentation including business tax returns, profit and loss statements, and client contracts may be necessary. Working with conventional loan lenders experienced in complex scenarios prevents surprise delays.

Choosing the Right Conventional Loan Lender for Your Situation

Selecting your financing partner requires evaluating multiple factors beyond just interest rates. The lowest rate quote often comes with service trade-offs, documentation challenges, or hidden costs.

Evaluation Criteria Beyond Interest Rates

Critical lender selection factors:

- Processing speed and closing reliability: Can they meet your timeline?

- Communication and accessibility: Will you reach a person when issues arise?

- Complex income expertise: Do they understand your compensation structure?

- Local market knowledge: Are they familiar with Seattle-area appraisal and inspection norms?

- Lock period flexibility: Do they offer extended locks for new construction?

- Rate lock policies: When do they lock and what are extension fees?

For buyers in competitive Seattle neighborhoods like Wallingford, Fremont, and Capitol Hill, lender reputation with agents and sellers matters significantly. A strong pre-approval from a respected lender carries more weight than one from an unknown online platform.

Questions to Ask Potential Lenders

Before committing to a conventional loan lender, ask specific questions that reveal their expertise and fit for your needs:

- How do you document and qualify RSU income from my employer?

- What is your average timeline from application to closing?

- Do you underwrite loans in-house or send them to a central location?

- What percentage of your applications close successfully?

- Can you provide references from recent Seattle-area clients?

- What happens if my appraisal comes in low?

- How do you handle rate locks and extension scenarios?

Sophisticated borrowers recognize that the answers to these questions matter more than a rate quote that may not materialize at closing.

Investment Property and Multi-Unit Financing

Conventional loan lenders provide financing for investment properties and multi-unit dwellings, though requirements increase compared to primary residence loans. Understanding these distinctions helps real estate investors structure acquisitions properly.

Investment Property Loan Requirements

Conventional loans for investment properties require larger down payments, higher credit scores, and greater reserves than primary residence loans.

Investment property requirements:

- Minimum 15-25% down payment (varies by lender)

- Credit scores typically 680 or higher

- 6-12 months reserves (PITI) required

- Debt-to-income ratios below 45%

- Property must appraise with positive rental income potential

Seattle's strong rental market makes investment property financing attractive for buyers in Everett, Shoreline, and Lake Forest Park where cash flow potential remains positive even with higher interest rates.

Multi-Family Property (2-4 Units) Advantages

Conventional loan lenders treat 2-4 unit properties differently than single-family rentals when you occupy one unit as your primary residence. This "house hacking" strategy allows lower down payments and the use of rental income for qualification.

| Property Type | Min. Down Payment | Occupancy Requirement | Rental Income |

|---|---|---|---|

| Single-family rental | 15-25% | None | Used for qualification |

| 2-4 unit owner-occupied | 5-15% | 12 months | 75% included in income |

| 2-4 unit investment | 15-25% | None | Used for qualification |

Young professionals in Seattle often use multi-family conventional loans to reduce living costs while building equity and rental income streams simultaneously.

Refinancing with Conventional Loan Lenders

Refinancing your existing mortgage with a conventional loan provides opportunities to reduce rates, eliminate PMI, access equity, or adjust loan terms. Understanding refinance types and timing maximizes value.

Rate and Term Refinancing Strategies

Rate and term refinances replace your existing loan with a new conventional loan, adjusting either the interest rate, the loan term, or both. In 2026, many homeowners who purchased in 2022-2023 at higher rates are exploring refinancing as rates moderate.

Refinance timing considerations:

- Break-even analysis: When do monthly savings exceed closing costs?

- Rate improvement threshold: Generally 0.75% or greater reduction makes sense

- Remaining loan term: Avoid extending repayment unnecessarily

- PMI removal opportunity: Refinance when reaching 80% LTV through appreciation

Seattle homeowners who purchased in 2023 often gained substantial equity through appreciation, creating opportunities to refinance into better terms while removing PMI simultaneously.

Cash-Out Refinancing for Various Purposes

Cash-out refinances allow you to access home equity while restructuring your mortgage. Conventional loan lenders limit cash-out refinances to 80% LTV for primary residences and 75% for investment properties.

Common cash-out refinance uses:

- Home renovations and improvements

- Debt consolidation at lower interest rates

- Investment property down payments

- Education funding

- Emergency reserves and financial flexibility

For tech professionals with growing equity in Seattle homes, strategic cash-out refinancing can fund additional real estate investments while maintaining tax-advantaged debt structures.

Common Challenges and How to Overcome Them

Even qualified borrowers encounter obstacles during the conventional loan process. Understanding common challenges and solutions prevents surprises and delays.

Appraisal Issues in Competitive Markets

Low appraisals create financing gaps when the property value comes in below the purchase price. In Seattle's competitive market, this occurs more frequently during bidding wars and with unique properties.

Solutions for low appraisals:

- Request reconsideration with additional comparable sales

- Increase down payment to cover the gap

- Negotiate purchase price reduction with seller

- Obtain second appraisal opinion (if lender allows)

- Use appraisal contingency to exit contract if necessary

Working with conventional loan lenders experienced in Seattle-area appraisal challenges helps navigate these situations strategically rather than emotionally.

Employment Changes During Underwriting

Job changes during the mortgage process create verification challenges. Conventional loan lenders require verbal verification of employment (VOE) immediately before closing, and unexpected employment changes can delay or derail approval.

Managing job transitions:

- Delay start dates until after closing if possible

- Ensure new position is in the same field with comparable income

- Obtain offer letter showing start date, salary, and employment type

- Avoid changing from W2 to self-employment during the process

- Communicate changes to your lender immediately

Seattle's dynamic tech employment market creates frequent job transitions. Experienced lenders help borrowers navigate these changes while maintaining loan approval integrity.

Working with Real Estate Professionals and Conventional Loan Lenders

Successful home purchases require coordination between borrowers, real estate agents, and lenders. Understanding how these relationships function improves outcomes.

Pre-Approval Strength and Seller Confidence

In competitive Seattle neighborhoods, pre-approval quality influences seller decisions significantly. Strong pre-approvals from reputable lenders demonstrate buyer credibility and transaction viability.

Elements of strong pre-approvals:

- Full credit review with formal underwriting

- Complete documentation review before offer submission

- Lender reputation known to listing agents

- Realistic loan amounts based on verified income

- Minimal contingencies and fast closing timelines

Buyers working with conventional loan lenders offering thorough pre-approval processes compete more effectively than those with automated online pre-qualifications lacking substance.

Communication Protocols Throughout the Process

Clear communication between all parties prevents delays and misunderstandings. Establish expectations early regarding response times, documentation requests, and status updates.

Real estate agents appreciate lenders who provide regular updates, respond quickly to questions, and manage client expectations realistically. This professional relationship often determines whether agents recommend specific conventional loan lenders to future clients.

Selecting the right conventional loan lender significantly impacts your financing costs, closing timeline, and overall homebuying experience. For Seattle-area homebuyers, working with professionals who understand local market dynamics, complex income qualification, and rapid closing timelines creates competitive advantages that translate to successful outcomes. Whether you're a first-time buyer in Lake Forest Park, a tech professional in Bellevue maximizing RSU income, or an investor building a rental portfolio across King and Snohomish Counties, Keith Akada and the team at Mortgage Reel bring 25+ years of experience, 750+ five-star reviews, and the ability to close in as few as 9 business days-giving you the expertise, speed, and personalized service that makes the difference in competitive markets.