Purchasing your first home in Seattle represents a significant financial milestone, and securing the right first buyers mortgage can make the difference between a smooth transaction and months of unnecessary stress. With median home prices in Seattle, Bellevue, and surrounding areas remaining elevated in 2026, understanding mortgage options, qualification requirements, and available assistance programs becomes critical for first-time buyers. This comprehensive guide walks through everything you need to know about obtaining a first buyers mortgage, from evaluating your financial readiness to closing on your new home in the Greater Seattle area.

Understanding First Buyers Mortgage Options

A first buyers mortgage isn't a single product, but rather a category of loan programs designed to help people purchase their first home with more accessible qualification standards and down payment requirements. These programs recognize that first-time buyers typically have less cash saved and shorter credit histories than repeat buyers.

Conventional Loans for First-Time Buyers

Conventional mortgages backed by Fannie Mae and Freddie Mac offer some of the most competitive rates available. Many first-time buyers in Seattle, Shoreline, and Lynnwood can qualify with as little as 3% down through programs like Fannie Mae's HomeReady or Freddie Mac's Home Possible.

Key conventional loan features include:

- Down payments starting at 3% for qualified buyers

- Competitive interest rates for borrowers with strong credit

- Private mortgage insurance (PMI) that can be removed once you reach 20% equity

- Flexible income qualification that works well for W-2 employees and salaried tech professionals

For buyers working at Amazon, Microsoft, or other Seattle-area tech companies, conventional loans offer the flexibility to qualify stock compensation and RSUs as part of your qualifying income, potentially boosting your purchasing power significantly.

FHA Loans: Lower Down Payments and Credit Flexibility

Federal Housing Administration (FHA) loans remain one of the most popular first buyers mortgage options nationwide. These government-backed loans allow down payments as low as 3.5% and accept credit scores starting at 580, making homeownership accessible to buyers who might not qualify for conventional financing.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% | 3% |

| Minimum Credit Score | 580 (typically) | 620 |

| Mortgage Insurance | Required for life of loan (if under 10% down) | Can be removed at 20% equity |

| Loan Limits (Seattle 2026) | $644,000 | $766,550 |

FHA loans work particularly well for first-time buyers in Mill Creek, Lake Forest Park, and Everett, where home prices may be more accessible than in central Seattle. The mortgage insurance requirements differ from conventional loans, staying in place for the life of the loan if you put down less than 10%, so understanding these long-term costs is essential.

VA Loans for Military Service Members

Veterans, active-duty service members, and eligible surviving spouses can access VA loans, which offer zero down payment requirements and no ongoing mortgage insurance. For those who qualify, VA loans represent one of the strongest first buyers mortgage options available.

USDA Loans in Rural Areas

While Seattle proper doesn't qualify, some areas north of Everett may be eligible for USDA loans offering 100% financing in designated rural zones. These loans serve moderate-income buyers purchasing in less densely populated areas.

First Buyers Mortgage Qualification Requirements

Understanding what lenders evaluate when reviewing your first buyers mortgage application helps you prepare effectively and address potential issues before they derail your timeline.

Credit Score Expectations

Your credit score significantly impacts both your ability to qualify and the interest rate you'll receive. Most conventional loans require a minimum 620 credit score, while FHA loans may accept scores as low as 580.

Steps to improve your credit before applying:

- Review your credit reports from all three bureaus for errors

- Pay down high credit card balances to below 30% utilization

- Avoid opening new credit accounts in the six months before applying

- Keep all existing accounts current with on-time payments

- Don't close old credit cards, as this reduces your available credit

Seattle-area lenders typically see stronger credit profiles among tech employees, but even minor issues like a missed payment or high utilization can impact your rate. Taking time to assess your finances before house hunting pays significant dividends.

Debt-to-Income Ratio Standards

Lenders calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your gross monthly income. Most first buyers mortgage programs require a DTI below 43%, though some allow up to 50% with compensating factors.

Monthly debts included in DTI calculations:

- Proposed mortgage payment (principal, interest, taxes, insurance, HOA)

- Car loans and leases

- Student loan payments

- Credit card minimum payments

- Personal loans

- Child support or alimony obligations

For Redmond and Bellevue buyers with high incomes but significant student debt, understanding how different loan programs calculate student loan payments can dramatically impact your qualification amount.

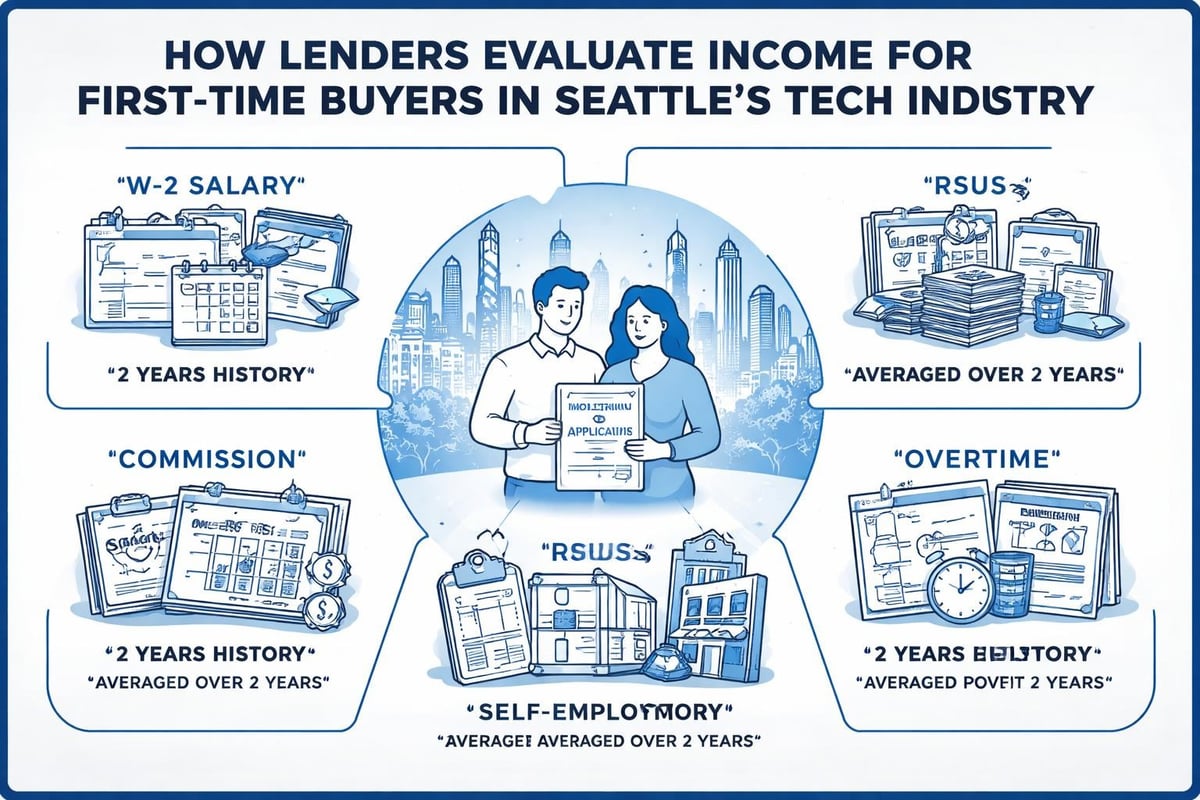

Income Documentation and Employment Verification

Standard W-2 employees need two years of employment history in the same field, recent pay stubs, and tax returns. Self-employed buyers face more extensive documentation requirements, typically needing two years of business tax returns and profit-and-loss statements.

Tech professionals in Seattle benefit from specialized expertise in qualifying equity compensation. When structured properly, RSUs, stock options, and performance bonuses can significantly increase your borrowing capacity under the right first buyers mortgage program.

Down Payment Requirements and Assistance Programs

The down payment represents the largest upfront cost for most first-time buyers. Understanding your options and available assistance programs can make homeownership achievable sooner than you might expect.

How Much Do You Really Need?

Contrary to popular belief, 20% down payments are not required for most first buyers mortgage programs. Here's what different loan types actually require:

- Conventional: 3% to 5% down

- FHA: 3.5% down

- VA: 0% down (for eligible veterans)

- USDA: 0% down (in eligible areas)

While larger down payments reduce your monthly payment and eliminate mortgage insurance on conventional loans, many Seattle buyers choose to put down less and preserve cash for closing costs, moving expenses, and emergency reserves.

Washington State First-Time Buyer Programs

Washington State Housing Finance Commission offers first-time homebuyer programs that provide down payment assistance and competitive interest rates. These programs often combine with FHA, VA, or conventional financing to reduce your upfront costs.

The House Key program, for example, offers down payment assistance loans that can be combined with a first mortgage, helping Seattle-area buyers overcome the down payment hurdle. Income and purchase price limits apply, but many moderate-income buyers in Shoreline, Lynnwood, and Everett qualify.

Employer Assistance Programs

Major Seattle employers including Amazon, Microsoft, and Boeing offer various homebuyer assistance benefits. Some provide down payment grants, others offer forgivable loans, and certain programs include homebuyer education credits. Checking with your HR department before starting your home search can uncover valuable resources.

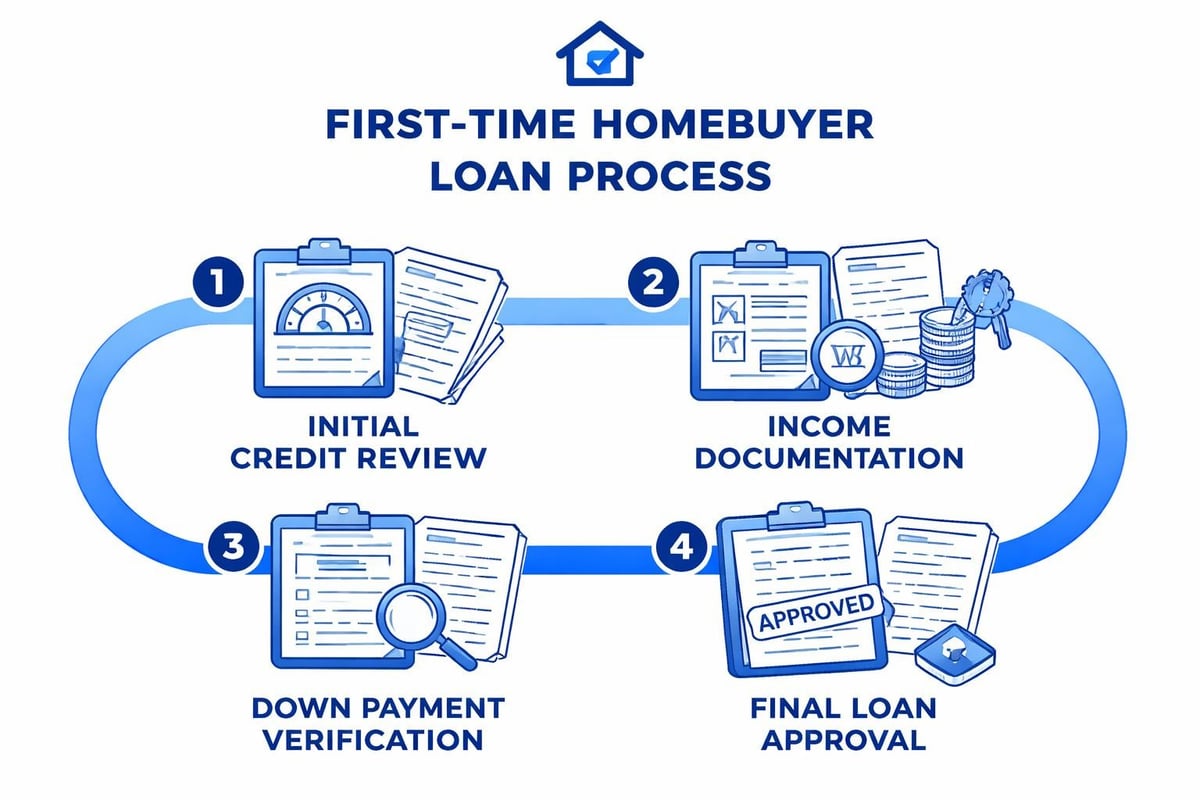

The First Buyers Mortgage Application Process

Understanding the mortgage process timeline helps you plan effectively and avoid common pitfalls that delay closings.

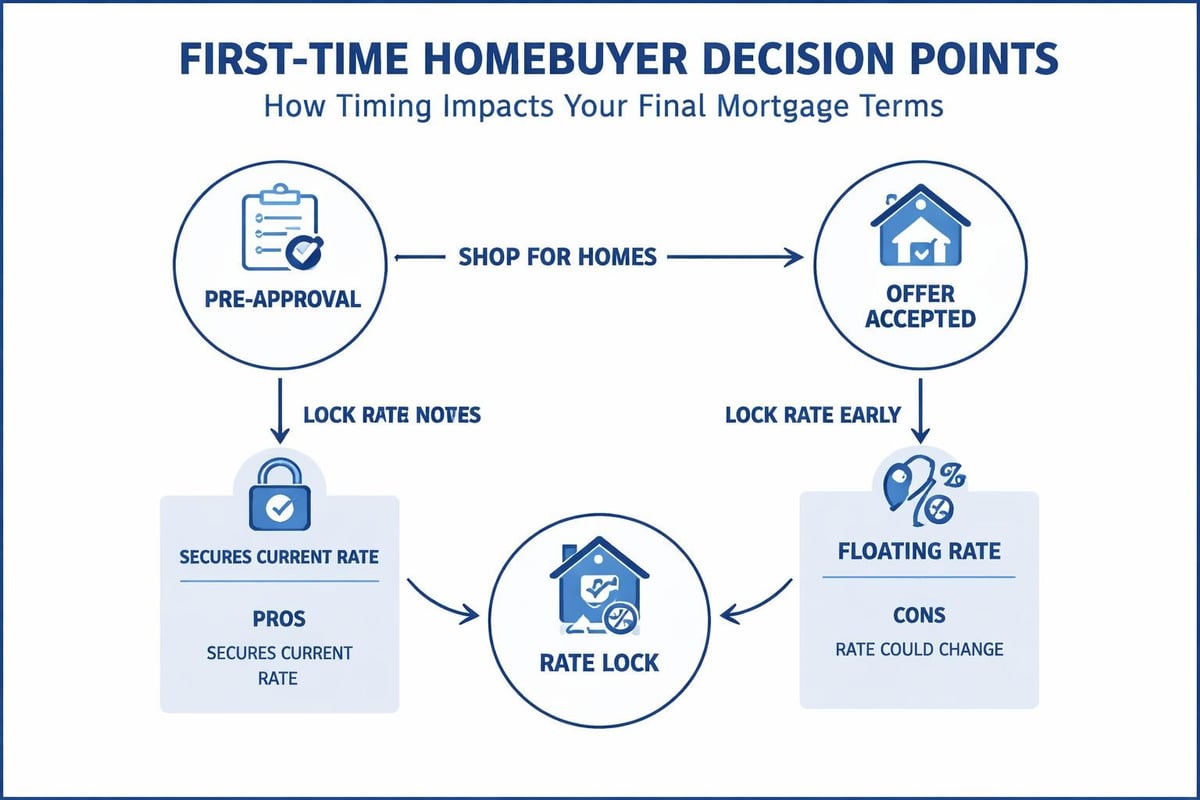

Getting Pre-Approved vs. Pre-Qualified

Pre-qualification provides a rough estimate based on basic information you provide. Pre-approval involves submitting documentation, running credit, and receiving conditional approval from an underwriter. In competitive Seattle-area markets, sellers expect pre-approval letters from serious buyers.

Documents needed for pre-approval:

- Two years of W-2s and tax returns

- Recent pay stubs (30 days)

- Two months of bank statements for all accounts

- Documentation for any other income sources

- Photo ID and Social Security card

- Rental history or current mortgage statement

Gathering these documents before contacting a lender speeds up the pre-approval process significantly.

Shopping for the Best Rate

Different lenders offer varying rates, fees, and service levels. Getting quotes from at least three lenders helps you compare options effectively. When evaluating first buyers mortgage offers, look beyond the interest rate to include:

| Comparison Factor | What to Evaluate |

|---|---|

| Interest Rate | Quoted rate and whether it's locked |

| Annual Percentage Rate (APR) | True cost including fees |

| Lender Fees | Origination, processing, underwriting |

| Closing Timeline | Ability to meet your purchase deadline |

| Loan Officer Expertise | Experience with your situation (tech income, etc.) |

Working with an experienced Seattle mortgage broker provides access to multiple lenders through a single application, often resulting in better rates and terms than approaching individual banks directly.

Lock Your Rate at the Right Time

Interest rates fluctuate daily. Once you have an accepted offer, locking your rate protects you from increases during the closing process. Most locks last 30 to 60 days, though longer periods are available for new construction purchases.

Common First Buyers Mortgage Mistakes to Avoid

Even well-prepared buyers make errors that can derail their mortgage approval or cost thousands in unnecessary expenses.

Making Large Purchases Before Closing

Financing a car, opening new credit cards, or making major purchases on credit changes your debt-to-income ratio and credit profile. Lenders re-verify employment and credit before closing, and new debts can cause your loan to be denied even after initial approval.

Financial moves to avoid during the mortgage process:

- Applying for new credit cards or loans

- Making large deposits without documenting the source

- Changing jobs or employment status

- Co-signing loans for others

- Making major purchases on credit

These restrictions typically apply from the time you start shopping for homes until after your loan closes and funds.

Skipping the Home Inspection

While not directly related to your first buyers mortgage, waiving inspections to win in competitive markets can lead to discovering expensive repairs after closing. Most loan programs allow inspection contingencies, and finding major issues gives you negotiating leverage or an exit option.

Overlooking Total Homeownership Costs

Your mortgage payment represents only part of homeownership expenses. Property taxes in Seattle, Bellevue, and King County run higher than many other areas. Homeowners insurance, HOA dues, maintenance, and utilities add substantially to your monthly housing costs.

A realistic budget includes:

- Principal and interest payment

- Property taxes (often 1% to 1.2% of home value annually in Seattle area)

- Homeowners insurance ($1,200 to $2,000+ annually)

- HOA dues if applicable

- Maintenance reserve (1% of home value annually recommended)

- Utilities and services

Understanding these costs prevents buyers from stretching too far on purchase price and becoming house-poor.

Special Considerations for Seattle-Area Buyers

The Greater Seattle housing market presents unique challenges and opportunities for first-time buyers pursuing a first buyers mortgage.

Competitive Market Strategies

Seattle's housing market remains competitive in 2026, particularly for well-priced homes in desirable neighborhoods. Working with experienced professionals who understand local market dynamics and can structure competitive offers becomes essential.

Strong offers in competitive situations often include:

- Pre-approval from a reputable local lender

- Larger earnest money deposits showing commitment

- Flexible closing timelines matching seller needs

- Clean offers with minimal contingencies when appropriate

- Personal letters to sellers (where permitted)

Understanding Seattle-Area Property Taxes

King County property taxes fund schools, transit, and local services. Annual tax bills typically range from 1.0% to 1.2% of assessed value, though this varies by specific location and voted levies. These taxes significantly impact your monthly payment, so accurate estimates are critical during budgeting.

Condo vs. Single-Family Considerations

Condos in Seattle, Bellevue, and downtown areas often provide more affordable entry points than single-family homes. However, condo financing requires additional review of the HOA's financial health, insurance coverage, and owner-occupancy ratio. Some buildings don't qualify for certain loan programs, making lender expertise in condo financing valuable.

Working with the Right Mortgage Professional

Choosing an experienced mortgage broker or loan officer familiar with first buyers mortgage products and Seattle-area markets streamlines your homebuying experience considerably.

Questions to Ask Potential Lenders

When interviewing mortgage professionals, consider asking:

- How many first-time buyers do you work with annually?

- What loan programs do you recommend for my situation and why?

- What's your average timeline from application to closing?

- How do you communicate during the process?

- Can you provide references from recent clients?

- Do you have experience qualifying the type of income I earn?

Responses to these questions reveal expertise level, communication style, and whether the lender fits your needs.

The Value of Local Expertise

Lenders familiar with Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett understand local appraisal challenges, common inspection issues, and how to structure offers that win in competitive situations. This local market knowledge often proves more valuable than getting a rate quote one-eighth of a percent lower from an online lender unfamiliar with Pacific Northwest real estate dynamics.

Specialized Tech Income Expertise

For the many technology professionals purchasing homes in the Seattle area, working with lenders experienced in qualifying RSUs, stock options, and bonus income makes a substantial difference in buying power. Standard lenders may discount or exclude equity compensation entirely, while specialists know how to document and maximize this income for qualification purposes.

Timeline and Next Steps

Understanding the typical first buyers mortgage timeline helps you plan effectively and set realistic expectations.

Standard purchase timeline:

- Pre-approval (1-3 days): Submit application and documentation

- Home shopping (2-12 weeks): Work with realtor to find properties

- Offer and acceptance (1-7 days): Negotiate purchase agreement

- Inspection period (7-10 days): Complete home inspection

- Appraisal (7-14 days): Lender orders property valuation

- Underwriting (5-10 days): Loan review and conditional approval

- Clear conditions (3-7 days): Provide additional documentation

- Final approval (1-3 days): Loan cleared to close

- Closing (1 day): Sign documents and receive keys

While experienced lenders can close loans in as few as 9 business days when necessary, allowing 30 to 45 days from accepted offer to closing provides comfortable cushion for any issues that arise.

Making Your First Buyers Mortgage Work Long-Term

Securing your first buyers mortgage is just the beginning of your homeownership journey. Building equity and managing your mortgage strategically sets you up for long-term financial success.

Building Equity Faster

While your loan amortizes over 30 years, making additional principal payments accelerates equity building and reduces total interest paid. Even modest extra payments can shave years off your mortgage and save tens of thousands in interest.

Refinancing Opportunities

As you build equity and potentially improve your credit and income, refinancing opportunities may arise. Refinancing to eliminate mortgage insurance, reduce your rate, or adjust your loan term can significantly improve your financial position.

Planning for the Future

Your first home likely won't be your forever home. Understanding how your first buyers mortgage positions you for future moves helps you make strategic decisions. Building equity, maintaining good credit, and managing your finances responsibly sets you up for easier subsequent purchases and better loan terms on future properties.

Securing the right first buyers mortgage requires understanding your options, preparing your finances, and working with experienced professionals who prioritize your success. Whether you're a tech professional in Redmond leveraging RSU income or a first-time buyer in Everett seeking down payment assistance, the path to homeownership becomes clearer with expert guidance. Keith Akada and the team at Mortgage Reel bring over 25 years of experience helping Seattle-area buyers navigate complex mortgage decisions with transparency and strategic insight. Ready to explore your first buyers mortgage options? Visit Mortgage Reel to start your homebuying journey with confidence.