Finding the right mortgage professional can mean the difference between a smooth home financing experience and months of frustration. Whether you're purchasing your first home in Lake Forest Park or refinancing a jumbo loan in Bellevue, working with a great mortgage broker provides access to multiple lenders, competitive rates, and expert guidance through every stage of the process. The Seattle housing market presents unique challenges that require specialized knowledge, from qualifying tech compensation to navigating bidding wars in neighborhoods like Capitol Hill and Fremont.

Understanding What Defines a Great Mortgage Broker

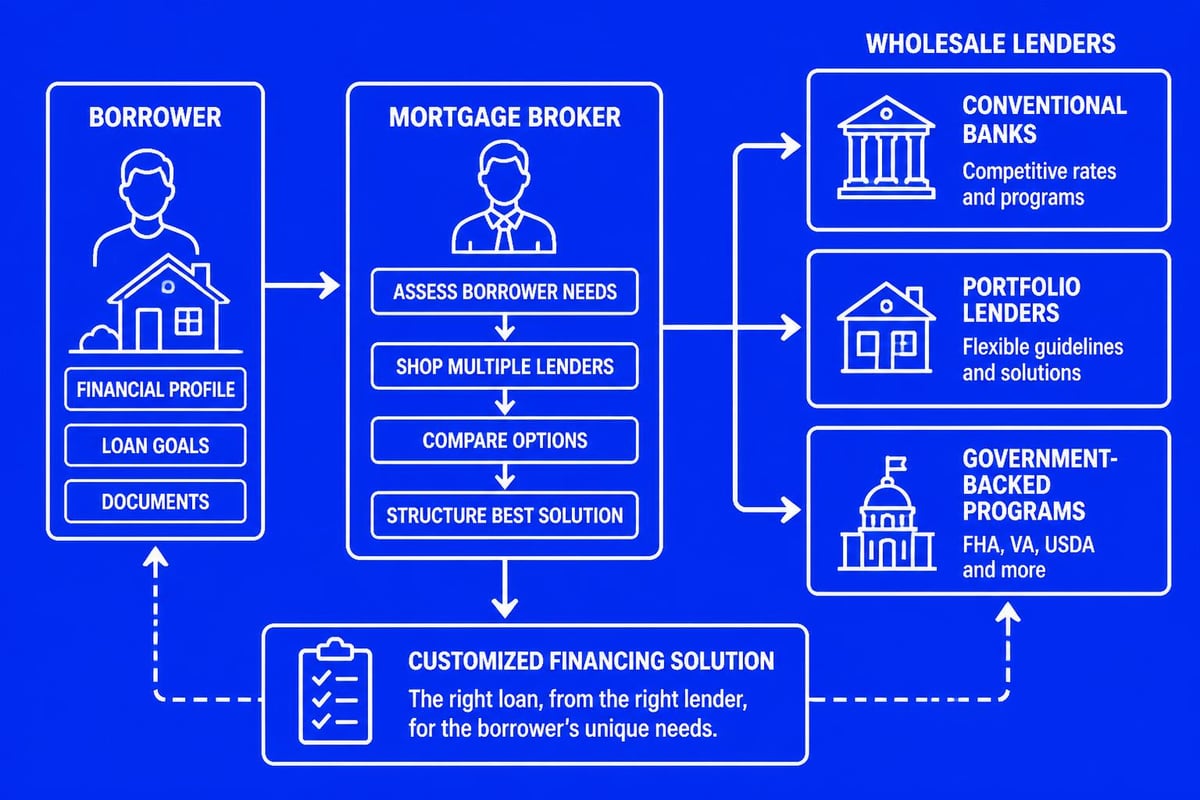

A great mortgage broker serves as your advocate throughout the home financing journey, connecting borrowers with lenders while managing the complex logistics of loan approval and closing. Unlike loan officers who work for a single bank, brokers have relationships with multiple wholesale lenders, creating options that fit diverse financial situations.

Licensing and Professional Credentials

Every state-licensed mortgage broker must complete specific education requirements and pass the Nationwide Multistate Licensing System (NMLS) examination. In Washington State, this means fulfilling 20 hours of pre-licensing education and maintaining continuing education credits annually. A great mortgage broker goes beyond minimum requirements by pursuing additional certifications and staying current with changing regulations.

Look for these professional markers when evaluating potential brokers:

- Active NMLS license with clean disciplinary history

- Years of experience in diverse market conditions

- Specialized training in complex income types (RSUs, bonuses, commissions)

- Lender relationships spanning conventional, government, and portfolio products

- Industry memberships such as the National Association of Mortgage Brokers

According to NerdWallet’s guide on what mortgage brokers do, brokers are compensated by lenders after closing, making their services typically free to borrowers while maintaining incentives to secure competitive terms.

Access to Multiple Lending Partners

The primary advantage of working with a broker versus a retail bank is choice. A great mortgage broker maintains active relationships with 20 to 50 wholesale lenders, each offering different rate structures, underwriting guidelines, and specialty programs. This network becomes particularly valuable for borrowers who don't fit traditional lending boxes.

Consider these scenarios where broker access creates advantages:

| Borrower Profile | Challenge | Broker Solution |

|---|---|---|

| Tech professional with RSU income | Traditional banks discount equity compensation | Portfolio lender counts 100% of vested RSUs |

| Self-employed business owner | Two years of declining income on tax returns | Bank statement loan program using deposits |

| First-time buyer with student debt | High debt-to-income ratio | FHA loan with compensating factors |

| Real estate investor | Four financed properties already | Portfolio lender with expanded capacity |

For Seattle homebuyers competing in fast-moving markets like Shoreline or Mill Creek, having a great mortgage broker with jumbo loan expertise can mean the difference between winning and losing a bid.

Communication Standards That Set Great Brokers Apart

Clear, proactive communication ranks among the most frequently cited qualities in five-star broker reviews. The mortgage process involves dozens of documents, tight deadlines, and coordination among buyers, sellers, real estate agents, title companies, and underwriters. A great mortgage broker manages this complexity while keeping clients informed at every milestone.

Response Time and Availability

In competitive Seattle neighborhoods where homes receive multiple offers within 48 hours, brokers must respond quickly to rate inquiries, pre-approval requests, and lender questions. Top-performing brokers typically return calls within two hours during business days and maintain evening or weekend availability during critical transaction phases.

The best brokers establish clear communication protocols at the start:

- Primary contact method (text, email, phone, or messaging app)

- Expected response windows for routine versus urgent matters

- Backup contact when the broker is unavailable

- Proactive updates at key process milestones

- Document delivery systems using secure portals

For clients relocating to Lake Forest Park or Everett from out of state, consistent communication becomes even more critical when coordinating inspections, appraisals, and closing logistics remotely.

Educational Approach to Complex Topics

Mortgage lending involves substantial jargon that can overwhelm first-time buyers. A great mortgage broker translates complex concepts into plain language, ensuring clients understand their options and obligations. This educational focus builds confidence and helps borrowers make informed decisions aligned with their long-term financial goals.

Effective brokers explain key concepts clearly:

- Loan product differences between conventional, FHA, VA, and jumbo mortgages

- Interest rate components including base rates, discount points, and lender credits

- Closing cost breakdowns with itemized fee explanations

- Underwriting requirements for income, assets, employment, and credit

- Post-closing obligations such as escrow accounts and payment scheduling

When working with Amazon or Microsoft employees on RSU income mortgage qualification, this educational approach helps tech professionals understand how underwriters evaluate equity compensation differently than W-2 salary.

Local Market Expertise in Greater Seattle

National online lenders can offer competitive rates, but they lack the ground-level knowledge that helps Seattle-area buyers navigate specific neighborhood dynamics, property types, and regional lending nuances. A great mortgage broker with deep local roots understands how appraisers value Seattle condominiums differently than Bellevue single-family homes, or how Snohomish County's rural properties require different loan programs than urban Seattle condos.

Understanding Regional Property Challenges

Seattle's diverse housing stock presents unique appraisal and underwriting considerations. A broker familiar with Capitol Hill's historic homes knows which foundation types raise lender concerns, while experience in Redmond's newer construction communities helps navigate HOA review requirements for high-rise condominiums.

Local expertise proves valuable for these property scenarios:

- Older Seattle homes requiring specialized renovation loans

- Condominium financing with specific warrantability requirements

- Multi-family properties in investment-friendly Everett neighborhoods

- Rural properties in Snohomish County needing well and septic approvals

- New construction purchases requiring builder coordination

Understanding conventional loan options for different Seattle neighborhoods helps brokers match borrowers with appropriate lenders who regularly approve loans in specific property types.

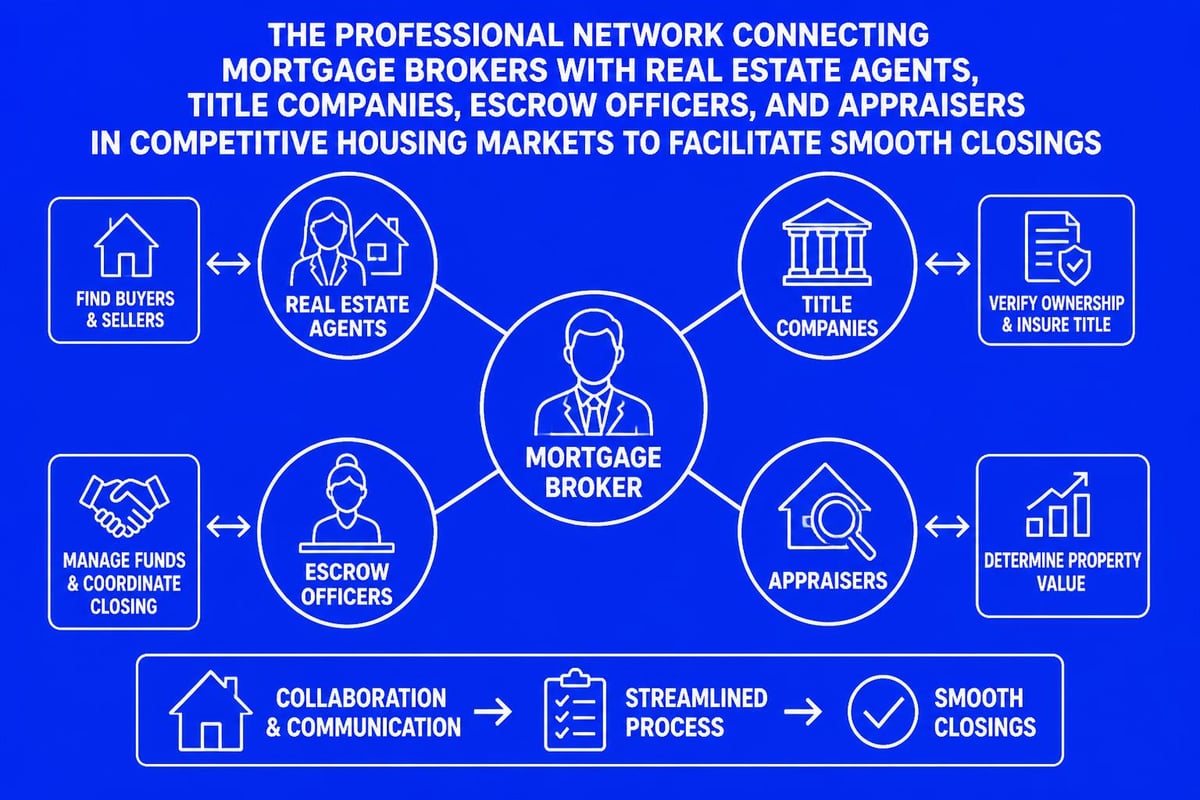

Relationships with Local Real Estate Professionals

A great mortgage broker builds referral relationships with successful real estate agents, title companies, and escrow officers throughout the region. These connections create smoother transactions through established trust and communication patterns. When an agent knows a broker consistently closes loans on time, they're more likely to recommend their mutual clients' offers to sellers.

This local network provides practical advantages:

- Stronger purchase offers when listing agents recognize reliable closing track records

- Faster title work through established escrow relationships

- Efficient appraisal scheduling with appraiser panel familiarity

- Quick problem resolution when unexpected issues arise pre-closing

- Market intelligence about neighborhood trends and pricing dynamics

For buyers relocating to areas like Lynnwood or Mill Creek, a broker's connections with local agents familiar with those markets can provide valuable insights beyond what appears in online listings. When planning a move to the Seattle area, coordinating with services like Movers Inventory for your household goods while your broker handles financing creates a comprehensive relocation strategy.

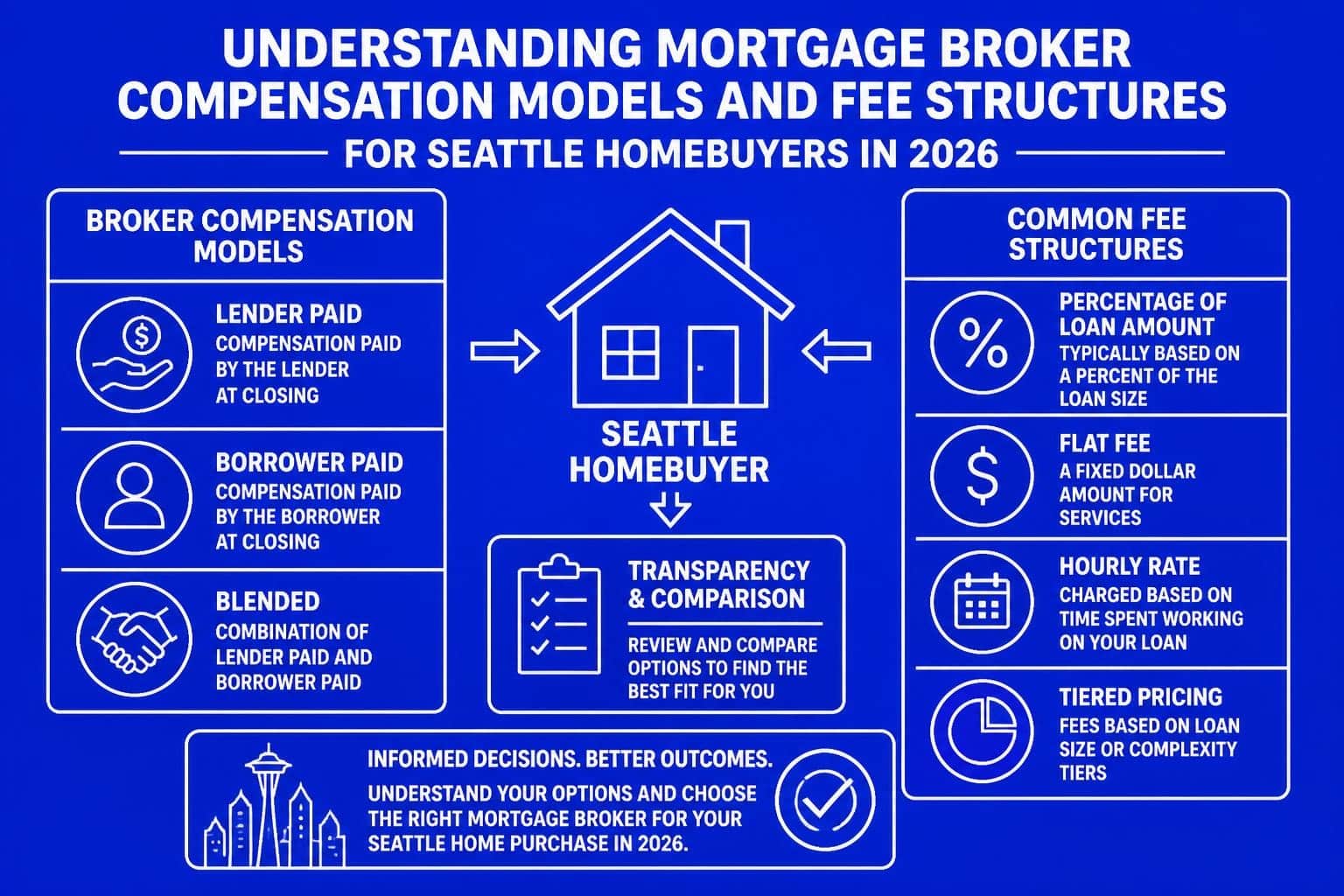

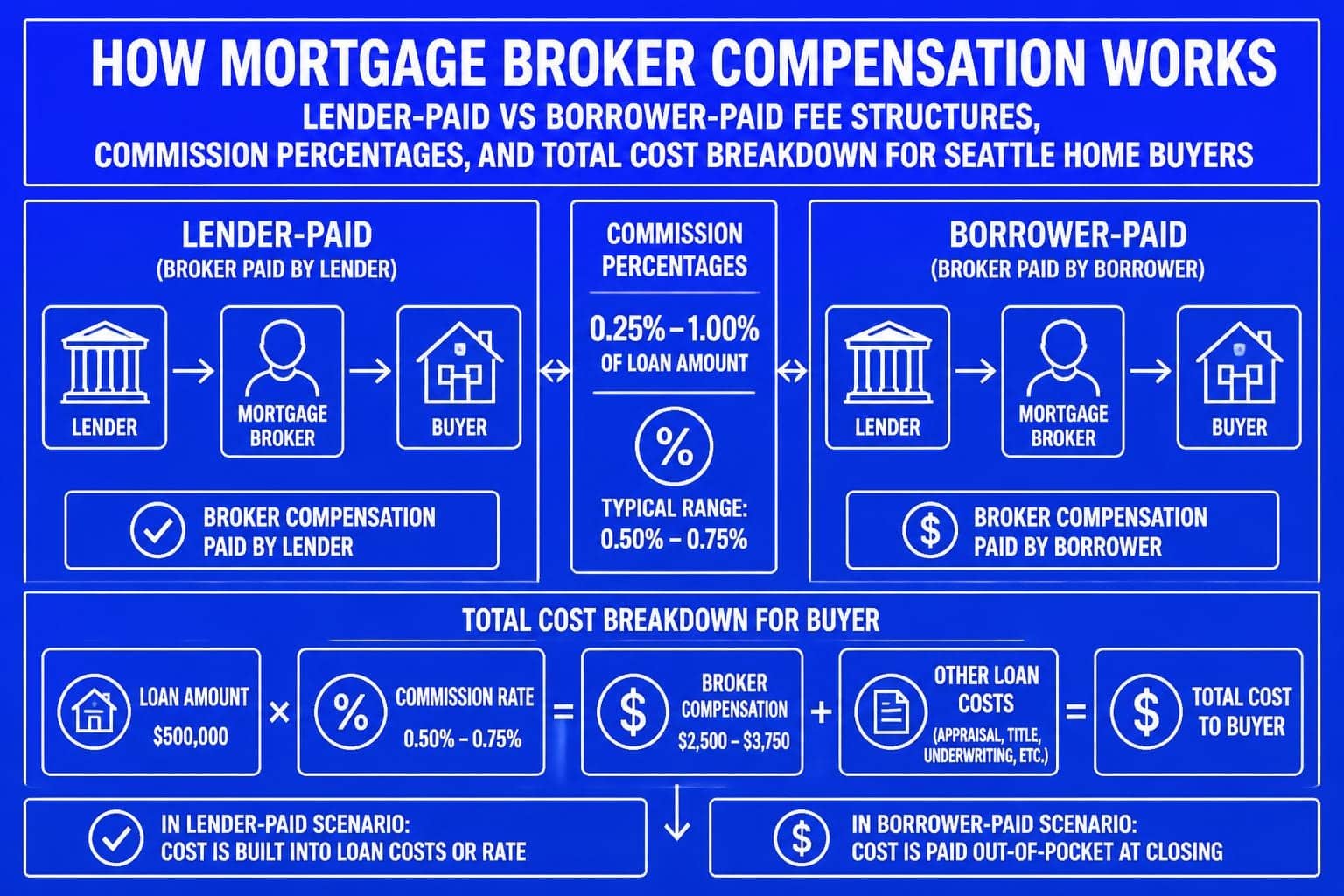

Transparency in Rates, Fees, and Compensation

Trust forms the foundation of successful broker-client relationships, and transparency about costs, compensation, and potential conflicts of interest separates great mortgage brokers from mediocre ones. While brokers don't charge borrowers directly in most transactions, they receive compensation from lenders, creating potential incentive misalignment if not managed ethically.

Clear Rate and Fee Disclosures

Within three business days of receiving a loan application, federal law requires brokers to provide a Loan Estimate detailing all costs, terms, and fees. A great mortgage broker exceeds this minimum by discussing costs upfront, explaining how different rate-point combinations affect monthly payments versus closing costs, and comparing multiple lender options side by side.

Transparent brokers provide itemized breakdowns showing:

| Fee Category | Typical Range | Who Receives Payment |

|---|---|---|

| Origination fee | 0.5% – 1.0% of loan amount | Broker compensation |

| Discount points | 0% – 2.0% of loan amount | Lender (buys down rate) |

| Appraisal fee | $500 – $800 | Appraisal company |

| Credit report | $25 – $75 | Credit bureau |

| Title insurance | $1,000 – $3,000 | Title company |

| Escrow/settlement | $400 – $800 | Escrow company |

When evaluating mortgage financing options, understanding how these fees compare across different lenders helps borrowers identify genuine savings versus marketing gimmicks.

Explaining Lender Compensation

Most borrowers don't realize that wholesale lenders pay brokers differently based on loan type, rate selected, and lender relationship tier. A great mortgage broker explains this compensation structure and discusses whether certain lender incentives might influence recommendations. This disclosure builds trust and ensures borrowers understand the full economic picture.

According to Kiplinger’s mortgage lender selection guide, comparing offers from multiple sources, including both brokers and direct lenders, provides the best opportunity to understand market pricing and identify the most competitive terms.

Specialized Knowledge for Unique Borrower Situations

Seattle's economy creates diverse borrower profiles requiring specialized mortgage expertise. A great mortgage broker develops deep knowledge in specific niches, whether that's qualifying tech compensation, financing investment properties, or helping self-employed business owners document income effectively. This specialization delivers better outcomes than working with generalist loan officers unfamiliar with complex scenarios.

Tech Industry Compensation Expertise

Amazon, Microsoft, Google, and other major Seattle employers structure compensation packages heavily weighted toward equity. Many tech professionals receive 40-60% of total compensation through RSUs, stock options, or bonuses, creating challenges for traditional mortgage underwriting that prioritizes W-2 base salary.

A great mortgage broker with tech industry expertise knows which lenders:

- Count unvested RSUs in qualifying income calculations

- Accept signing bonuses without requiring two-year payment history

- Use total compensation statements rather than tax returns alone

- Understand stock vesting schedules when projecting future income

- Approve jumbo loans at higher debt ratios for strong borrowers

This specialized knowledge frequently adds $200,000 to $400,000 in purchasing power for Seattle tech workers buying in Redmond, Bellevue, or Kirkland. Understanding how RSU income affects mortgage qualification requires staying current with underwriting guideline changes and maintaining relationships with lenders experienced in this borrower segment.

Investment Property Financing

Real estate investors need brokers who understand DSCR loans, portfolio lender guidelines, and creative financing structures for multi-property owners. Traditional conforming loans limit borrowers to financing 10 properties total, but portfolio lenders offer expanded capacity for qualified investors building rental portfolios in markets like Everett or Snohomish County.

Great brokers serving investors provide guidance on:

- Cash-out refinancing to access equity for next purchases

- 1031 exchange financing coordination with tax advisors

- DSCR loan programs that qualify based on rental income, not personal income

- Portfolio lender options for borrowers exceeding conventional limits

- Short-term rental financing for Airbnb or VRBO properties

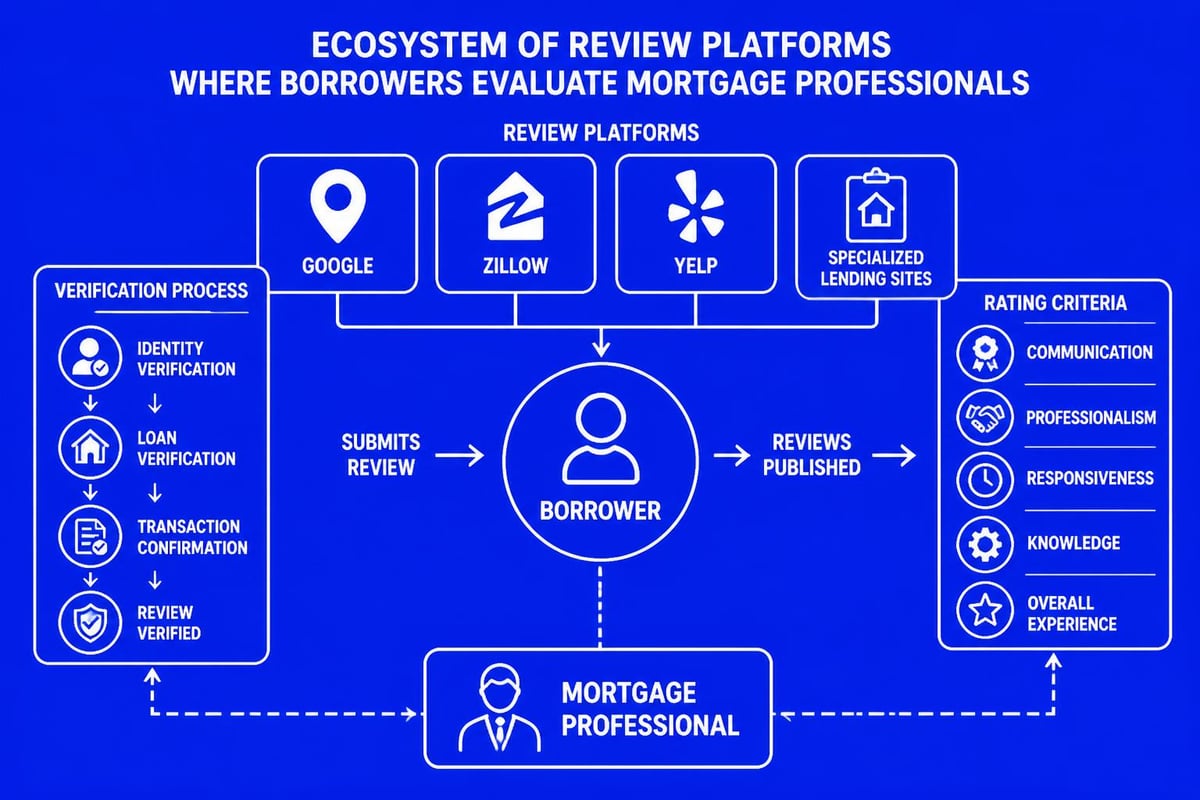

Proven Track Record and Verifiable Reviews

Past performance provides strong indicators of future results in mortgage lending. A great mortgage broker demonstrates consistent success through verified client reviews, on-time closing rates, and professional references. In 2026's digital environment, borrowers can easily research broker reputations across multiple platforms before committing to work together.

Where to Find Authentic Feedback

Start your broker research on these platforms to gather comprehensive feedback:

- Google Business Profile for overall service quality and communication

- Zillow lender reviews from verified purchase transactions

- Yelp ratings with detailed experience narratives

- Better Business Bureau for complaint history and resolution patterns

- NMLS Consumer Access for licensing status and disciplinary records

Pay particular attention to how brokers respond to negative reviews. A great mortgage broker addresses concerns professionally, takes ownership of legitimate issues, and demonstrates commitment to client satisfaction even when problems arise.

Specific Qualities to Look For in Reviews

Beyond star ratings, read detailed reviews for patterns revealing broker strengths and weaknesses. Consistent mentions of specific qualities across multiple reviews provide reliable insights into working style and service delivery.

Look for these recurring themes in positive reviews:

- Proactive communication during stressful transaction phases

- Creative problem-solving when underwriting challenges emerge

- Rate competitiveness compared to other quotes received

- Educational approach that builds borrower confidence

- On-time closings meeting purchase agreement deadlines

- Post-closing support for questions about payments or escrow

For first-time homebuyers in Seattle, finding a broker with strong educational reviews indicates they'll receive patient guidance through unfamiliar processes.

Questions to Ask When Interviewing Potential Brokers

Before committing to work with any mortgage broker, conduct interviews with at least two or three candidates. This comparison shopping helps you evaluate communication styles, expertise levels, and rate competitiveness while building confidence in your final selection.

Essential Questions About Experience and Expertise

Start with basic qualification questions to establish credentials and specialization:

- How many years have you worked as a mortgage broker in the Seattle area?

- What percentage of your clients are first-time buyers versus experienced homeowners?

- Do you have specific experience with my borrower profile? (tech compensation, self-employed, investment properties, etc.)

- Which lenders do you work with most frequently, and why?

- What's your average time from application to closing?

According to NerdWallet’s tips on finding a mortgage broker, understanding broker specialization helps ensure alignment between your needs and their expertise.

Process and Communication Expectations

Clarify how the broker manages transactions and maintains client contact:

- What's your typical response time for emails and phone calls?

- How do you communicate rate changes or underwriting updates?

- Who handles my file if you're unavailable due to vacation or emergency?

- What technology platforms do you use for document collection and status updates?

- How do you coordinate with my real estate agent and other transaction parties?

For buyers working on tight timelines in competitive markets, understanding a broker's ability to close quickly becomes critical. Some brokers offer expedited underwriting through specific lender partnerships that can reduce closing timelines from 30 days to as few as 10-15 days.

Understanding Service Models and Value Propositions

Not all brokers operate identically. Some focus on high-volume, streamlined transactions with lower fees, while others provide white-glove service with extensive hand-holding throughout the process. A great mortgage broker clearly articulates their service model so borrowers know what to expect and can evaluate fit with their preferences.

Full-Service Versus Limited-Service Models

Full-service brokers typically:

- Conduct in-person or video consultations to review goals and finances

- Proactively shop rates across multiple lenders as markets change

- Manage all document collection and underwriting communication

- Coordinate with agents, title companies, and other transaction parties

- Provide post-closing support for questions or refinance timing

Limited-service models might offer lower costs but require borrowers to handle more logistics themselves, such as gathering documents or communicating directly with processors.

For complex situations like jumbo home loan qualification requiring extensive documentation and multiple underwriting reviews, full-service support typically produces better outcomes despite potentially higher costs.

Technology Integration and User Experience

Modern mortgage brokers leverage technology to improve efficiency, transparency, and client experience. A great mortgage broker balances digital convenience with personal service, using platforms that simplify document upload, application status tracking, and secure communication while remaining accessible for phone or video conversations when needed.

Evaluate technology offerings such as:

- Mobile-friendly application portals for document submission

- Real-time status dashboards showing underwriting progress

- Integrated rate-lock platforms with transparent pricing

- Digital closing options reducing in-person signing requirements

- Automated milestone notifications keeping all parties informed

The Importance of Lender Relationship Strength

A broker's value extends beyond simple rate comparison. Great mortgage brokers cultivate deep relationships with specific lenders, earning preferred pricing, faster underwriting, and flexibility when unique situations require senior underwriter attention or guideline interpretations.

How Strong Relationships Benefit Borrowers

Experienced brokers who consistently deliver well-documented, accurately disclosed loans to wholesale partners receive advantages that benefit their clients:

- Pricing exceptions on rate or fees for strong borrower profiles

- Expedited underwriting with priority queue placement

- Guideline flexibility for borderline approval situations

- Direct underwriter access to resolve questions quickly

- Post-closing support for loan modifications or payment issues

These relationship benefits rarely appear in advertised rates but frequently determine whether challenging loans close successfully or fall apart weeks into the process.

For buyers purchasing homes in competitive Seattle neighborhoods, having a broker who can expedite underwriting approval provides negotiating leverage when sellers choose between multiple offers.

Evaluating Cost-Effectiveness Beyond Interest Rates

While interest rates receive the most attention in mortgage discussions, overall cost-effectiveness requires evaluating the full package of rates, fees, closing timeline, and service quality. A great mortgage broker helps borrowers understand these tradeoffs rather than simply chasing the lowest advertised rate without context.

Rate-Point Combinations and Break-Even Analysis

Most lenders offer rate-point combinations where borrowers can pay upfront discount points to secure lower interest rates or accept higher rates in exchange for lender credits covering closing costs. The optimal choice depends on how long you plan to keep the mortgage and your available cash for closing.

A great mortgage broker presents multiple scenarios with break-even analysis:

| Rate Option | Interest Rate | Monthly Payment | Closing Costs | Break-Even Period |

|---|---|---|---|---|

| No points | 6.75% | $3,247 | $8,500 | Baseline |

| 1 point paid | 6.50% | $3,160 | $13,500 | 58 months |

| Lender credit | 7.00% | $3,327 | $5,000 | n/a |

For borrowers planning to refinance within 2-3 years, paying points rarely makes financial sense. Conversely, buyers planning to stay 7+ years in their Shoreline or Lynnwood homes typically benefit from buying down rates through upfront points.

Value of Expertise in Complex Situations

Sometimes the most cost-effective broker charges higher fees but delivers successful outcomes on challenging loans that other brokers would decline or fail to close. Self-employed borrowers, those with recent credit events, or buyers with complex income structures often find that expertise trumps lowest cost.

Consider total value when comparing brokers:

- Approval probability based on experience with your situation

- Closing timeline reliability meeting purchase contract deadlines

- Problem-solving capability when unexpected issues emerge

- Post-closing support for questions or future refinance needs

For tech professionals evaluating 10% down jumbo loan options, working with a broker experienced in reduced-down-payment jumbo products may uncover financing paths that less specialized brokers miss entirely.

Finding a great mortgage broker requires evaluating credentials, communication style, local expertise, transparency, and specialized knowledge relevant to your unique situation. The right broker serves as your advocate, educator, and problem-solver throughout the home financing journey.

Whether you're a first-time buyer in Lake Forest Park, a tech professional maximizing RSU income for a Bellevue purchase, or an investor expanding your Seattle-area portfolio, working with an experienced local broker ensures access to competitive rates and expert guidance. Keith Akada at Mortgage Reel brings 25+ years of Seattle market expertise with 750+ five-star reviews, specializing in tech compensation qualification, jumbo loans, and fast closings for competitive markets across Seattle, Bellevue, Redmond, and Kirkland.