Choosing the right lender can make or break your home financing experience in Seattle's competitive real estate market. With median home prices continuing to climb across neighborhoods from Capitol Hill to Bellevue, understanding how home loan lenders operate and what sets them apart has never been more critical. Whether you're a first-time buyer navigating down payment options or a tech professional leveraging stock compensation for a jumbo loan, knowing how to evaluate lenders ensures you secure favorable terms and close on time.

Understanding Different Types of Home Loan Lenders

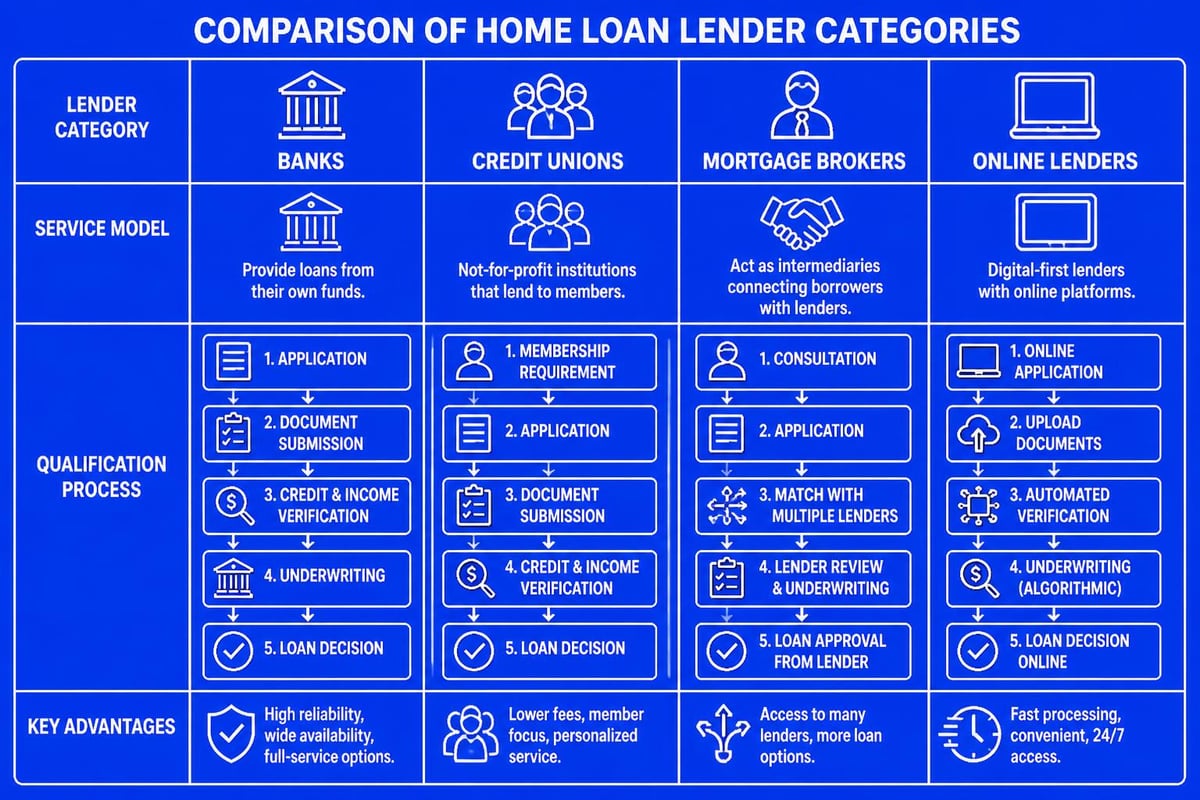

The lending landscape offers multiple pathways to financing your home purchase. Each type of lender brings distinct advantages and potential limitations.

Banks and Credit Unions

Traditional banks offer stability and established reputations, often providing competitive rates for customers with strong banking relationships. Credit unions typically deliver lower fees and more personalized service to their members, making them attractive for borrowers seeking community-focused support.

Key advantages include:

- Established brand recognition and regulatory oversight

- Potential relationship discounts for existing customers

- In-house underwriting and servicing

- Direct access to decision-makers

However, banks may have stricter qualification requirements and slower processing times compared to specialized lenders. Credit unions often require membership, which can limit accessibility for some Seattle-area borrowers.

Mortgage Brokers

Brokers serve as intermediaries who connect borrowers with multiple wholesale lenders. This access creates opportunities to compare numerous loan programs simultaneously, particularly valuable for borrowers with unique income sources like RSUs or complex financial situations.

Working with good mortgage brokers provides several strategic benefits in markets like Seattle, Shoreline, and Redmond. Brokers can match your specific financial profile with lenders most likely to approve your application under favorable terms.

| Lender Type | Best For | Typical Timeline |

|---|---|---|

| Traditional Banks | Strong credit, simple income | 30-45 days |

| Credit Unions | Members seeking lower fees | 30-40 days |

| Mortgage Brokers | Complex income, comparison shopping | 15-30 days |

| Online Lenders | Tech-savvy, streamlined process | 20-35 days |

Online Lenders

Digital-first lenders have transformed the mortgage industry by offering streamlined applications, rapid pre-approvals, and competitive rates. These platforms excel at transparency, providing instant rate quotes and status updates throughout the process.

For tech professionals in Bellevue and Kirkland, online platforms often integrate seamlessly with digital workflows. However, they may lack the personalized guidance needed for complex scenarios like qualifying substantial equity compensation.

Essential Qualifications Home Loan Lenders Review

Understanding what home loan lenders evaluate during the approval process helps you prepare documentation and strengthen your application before shopping for rates.

Income Verification and Documentation

Lenders assess income stability and sufficiency through multiple documentation types. W-2 employees provide the most straightforward verification, while self-employed borrowers face additional scrutiny with tax returns and profit-loss statements spanning two years.

For Seattle's significant tech workforce, qualifying RSUs, stock options, and performance bonuses requires specialized expertise. Conventional loan lenders may apply different calculations for equity compensation, typically averaging two years of vesting history to establish reliable income.

Required documentation typically includes:

- Two years of W-2s and tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements

- RSU vesting schedules and sale documentation

- Bonus history and employer verification letters

Credit Profile Assessment

Your credit score directly impacts interest rates and program eligibility. Most conventional programs require minimum scores of 620, while FHA loans may accept scores as low as 580 with larger down payments.

Beyond the numerical score, lenders examine your credit report for recent late payments, collections, bankruptcies, and debt-to-income ratios. Seattle borrowers should review their reports months before applying to address errors or resolve outstanding issues.

Asset Requirements and Reserves

Down payment funds must be sourced and documented through bank statements showing consistent balances. Gift funds from family members require specific documentation confirming the donor's ability to give and the non-repayment nature of the transfer.

Reserve requirements vary by loan type and property use. Investment properties in Lake Forest Park or Mill Creek typically require 6-12 months of reserves, while primary residences may need minimal reserves depending on the loan program.

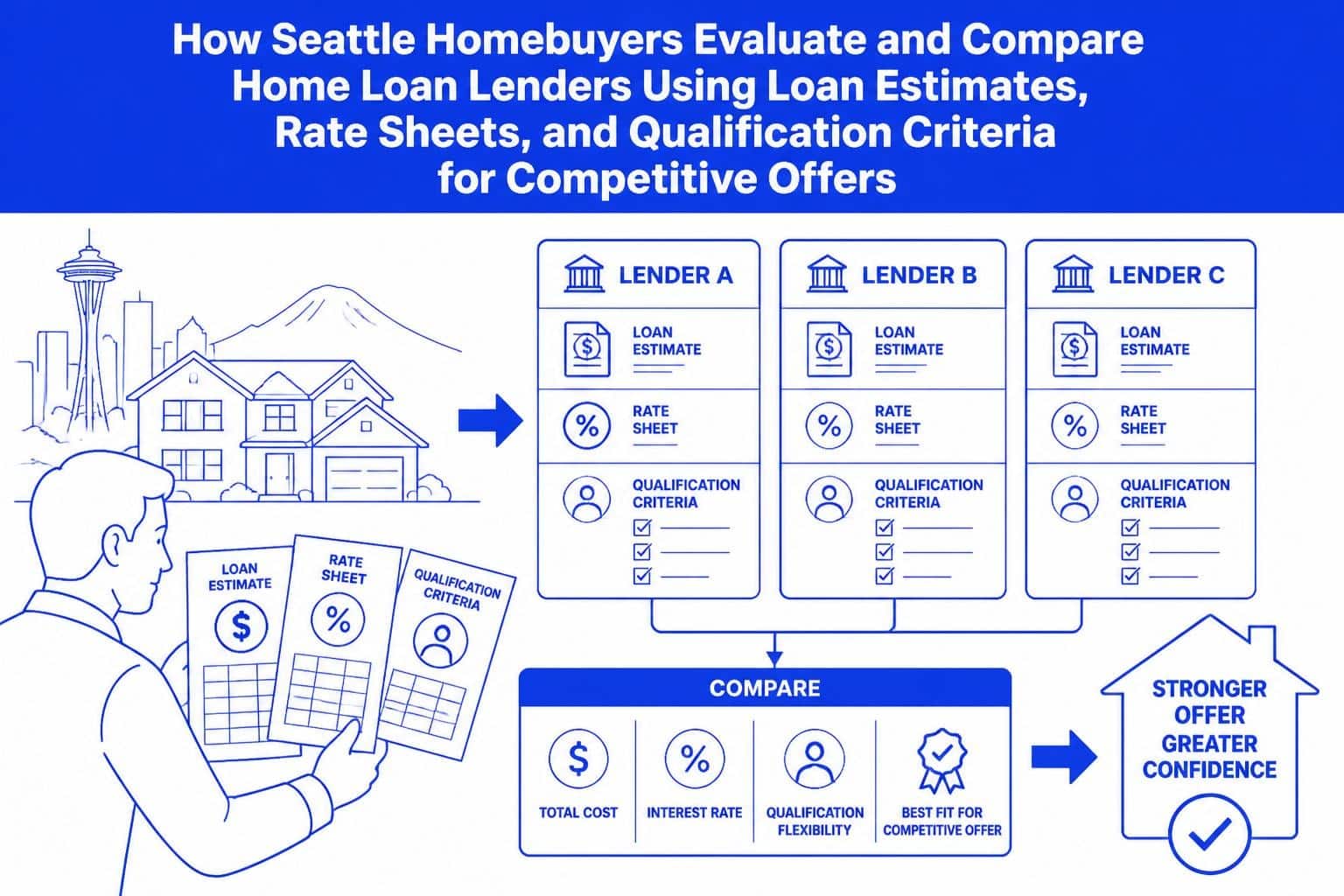

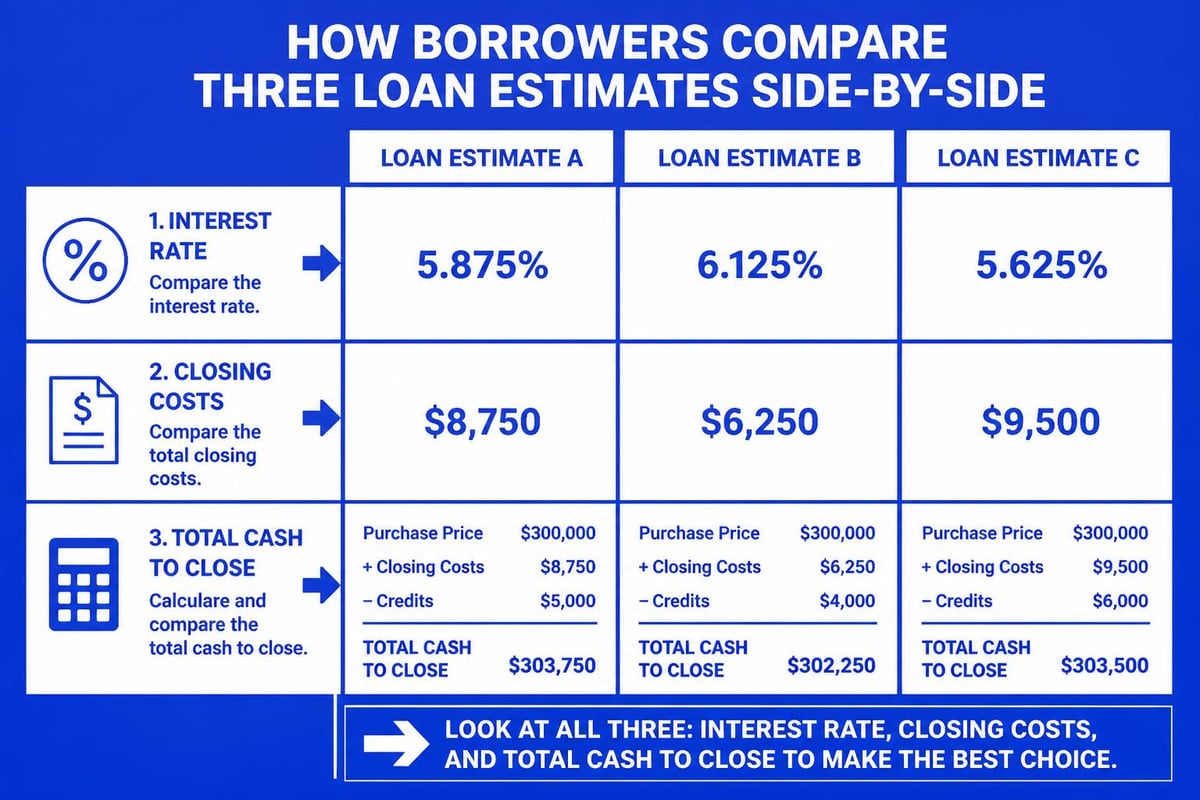

Comparing Loan Offers From Multiple Lenders

The Consumer Financial Protection Bureau emphasizes contacting multiple lenders to ensure you receive competitive terms. This comparison process protects you from overpaying and reveals which lenders offer the most favorable overall package.

Analyzing the Loan Estimate

Every lender must provide a standardized Loan Estimate within three business days of receiving your application. This three-page document details interest rates, monthly payments, closing costs, and loan terms in identical formats, enabling direct comparisons.

Critical sections to compare include:

- Interest rate and APR – The APR incorporates fees, providing a more complete cost picture

- Loan terms – Confirm the loan amount, term length, and prepayment penalties

- Projected payments – Review principal, interest, taxes, insurance, and HOA fees

- Closing costs – Compare origination charges, third-party services, and lender credits

- Cash to close – Total funds needed at closing after credits and down payment

Understanding Rate Lock Strategies

Interest rates fluctuate daily based on economic indicators and bond markets. A rate lock guarantees your quoted rate for a specified period, typically 30-60 days. In volatile markets or during busy seasons affecting Shoreline and Lynnwood, longer lock periods provide security but may carry higher costs.

Timing your rate lock strategically balances protection against rate increases with flexibility if rates drop. Some lenders offer float-down options allowing one-time rate adjustments if market conditions improve before closing.

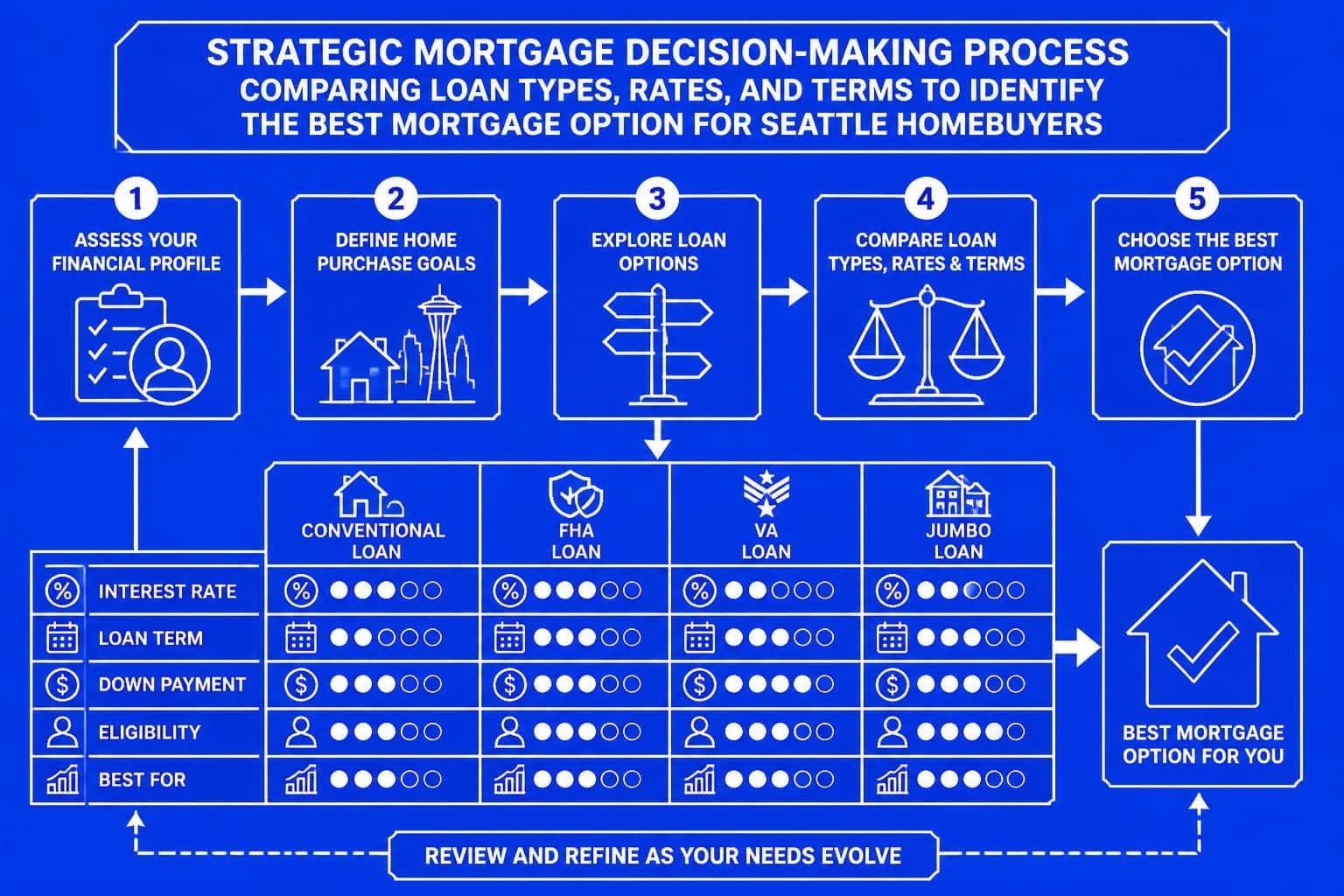

Specialized Loan Programs and Lender Expertise

Different home loan lenders specialize in particular programs based on their funding sources, underwriting capacity, and market positioning. Understanding these specializations helps you target lenders most likely to approve your specific scenario.

Jumbo Loan Specialists

Seattle's high home prices frequently push borrowers into jumbo territory, with conventional loan limits in 2026 set at $806,500 for single-family homes in King County. Jumbo home loans require enhanced qualification standards, larger reserves, and specialized underwriting.

Not all lenders offer competitive jumbo programs. Those specializing in this segment can structure loans exceeding $2 million while accommodating complex income sources prevalent among Bellevue and Redmond tech professionals.

Government-Backed Loan Programs

The Consumer Financial Protection Bureau explains different loan options including FHA, VA, and USDA programs, each serving specific borrower populations with unique advantages.

FHA loans accommodate lower credit scores and down payments as low as 3.5%, making them valuable for first-time home buyers in Everett and Mill Creek. VA loans provide zero-down financing for qualifying veterans and active military personnel, while USDA loans serve eligible rural areas.

| Program Type | Min. Down Payment | Credit Score | Best For |

|---|---|---|---|

| Conventional | 3% | 620+ | Strong credit, standard income |

| FHA | 3.5% | 580+ | Lower credit, smaller down payment |

| VA | 0% | No minimum | Veterans, active military |

| Jumbo | 10-20% | 700+ | High-value properties |

Specialty Income Programs

Tech professionals with significant equity compensation need lenders experienced in qualifying RSUs, ISO stock options, and non-qualified stock options. Standard underwriting may discount or exclude this income entirely, reducing buying power substantially.

Lenders with advanced capability assess vesting schedules, historical sale patterns, and employer stock performance to establish reliable qualifying income. This expertise can increase buying power by $100,000 or more for Amazon, Microsoft, and Google employees throughout the Seattle metro area.

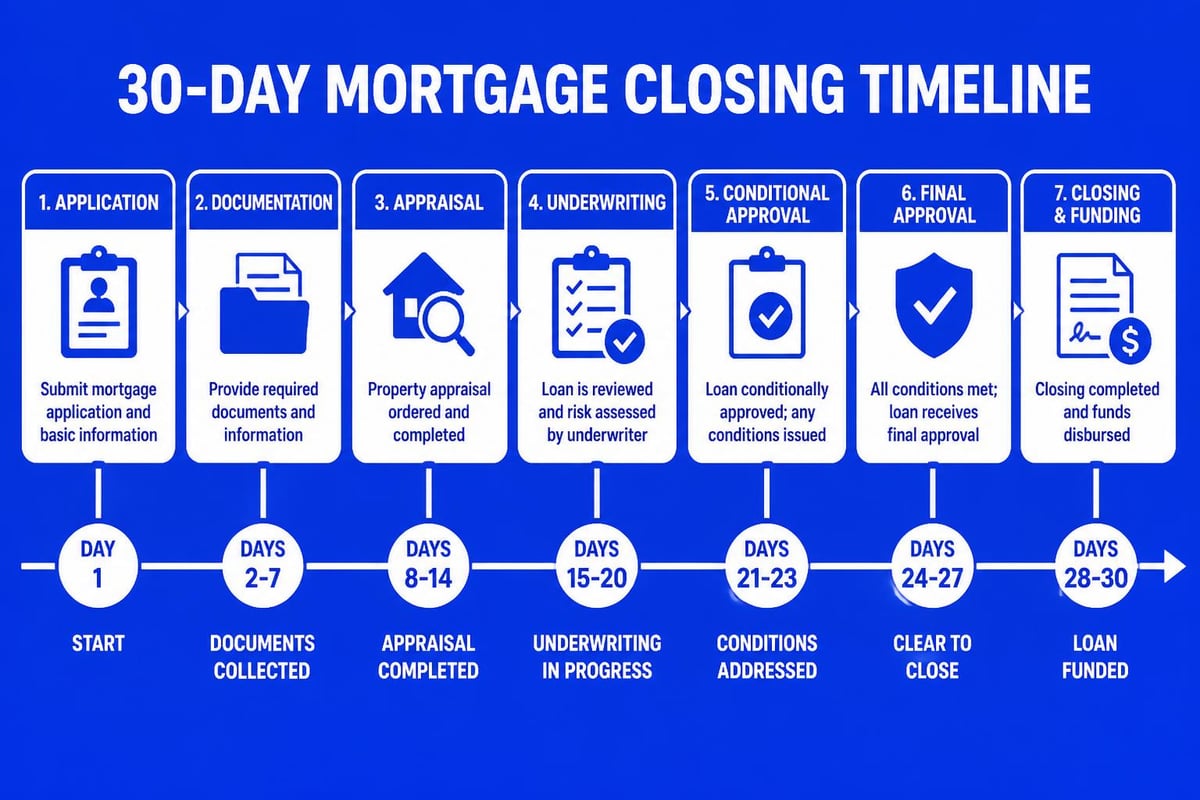

Timeline Expectations and Closing Speed

Understanding realistic timelines helps you plan purchase offers and coordinate with sellers. While some home loan lenders advertise ultra-fast closings, actual timelines depend on loan complexity, property type, and documentation completeness.

Standard Processing Timelines

Conventional loans with complete documentation typically close in 30-45 days. This period includes application, processing, underwriting, appraisal completion, and final approval. Government-backed loans may extend slightly longer due to additional certification requirements.

Typical milestone timeline:

- Days 1-3: Application and Loan Estimate delivery

- Days 4-7: Initial documentation collection and review

- Days 8-15: Appraisal ordered and completed

- Days 16-25: Underwriting review and conditions issued

- Days 26-30: Final approval and clear to close

- Days 31-35: Closing preparation and funding

Expedited Closing Capabilities

Advanced lenders with in-house underwriting and strong appraisal networks can compress timelines significantly. Closings in 9-15 business days become possible when borrowers provide complete documentation immediately and properties appraise without complications.

For competitive Seattle markets where sellers prioritize quick closings, demonstrating this capability in your offer strengthens your position. Working with mortgage financing professionals who consistently deliver on promised timelines builds realtor relationships and wins bidding wars.

Technology and Communication Standards

Modern lending requires sophisticated technology platforms and proactive communication protocols. Evaluating these factors during lender selection prevents frustration and delays throughout your transaction.

Digital Application and Tracking

Leading home loan lenders provide secure portals where borrowers upload documents, track application status, and communicate with their loan team. Mobile apps extend this accessibility, enabling real-time updates while commuting through downtown Seattle or traveling for work.

Automation accelerates routine tasks like income verification and asset validation through integrations with payroll providers and financial institutions. This technology reduces manual review time and catches discrepancies earlier in the process.

Loan Officer Accessibility

Your loan officer serves as your primary contact and advocate throughout the process. Responsive communication, proactive updates, and clear explanations distinguish exceptional service from adequate processing.

Evaluate accessibility during initial conversations. Do they respond promptly to emails and calls? Can they explain complex concepts in understandable terms? Will they be available evenings and weekends as closing approaches? These factors significantly impact your experience, especially in fast-moving markets across Kirkland and Redmond.

Evaluating Lender Reputation and Reviews

Third-party reviews and regulatory records provide objective insights into lender performance and reliability. This research complements rate comparisons and helps identify potential issues before committing to a lender.

Online Review Platforms

Research lenders across multiple platforms including Google, Zillow, Yelp, and the Better Business Bureau. Look for patterns in feedback rather than isolated complaints. Consistent themes about communication, closing delays, or unexpected fees signal systemic issues.

Pay attention to how lenders respond to negative reviews. Professional, constructive responses demonstrate accountability and commitment to customer satisfaction. Defensive or dismissive replies suggest problematic cultures.

Regulatory Compliance History

The Office of the Comptroller of the Currency provides mortgage information including consumer protection resources. Research whether lenders have faced enforcement actions, licensing issues, or consumer complaints through state and federal databases.

Key resources for vetting lenders:

- Nationwide Mortgage Licensing System (NMLS)

- Consumer Financial Protection Bureau complaint database

- State Department of Financial Institutions records

- Better Business Bureau ratings and complaint history

Cost Structures and Fee Transparency

Understanding how home loan lenders structure costs helps you identify the best value and avoid unnecessary expenses. All legitimate fees appear on your Loan Estimate, but explanations vary widely in clarity and completeness.

Origination and Processing Fees

Lender compensation comes through origination fees (direct charges to borrowers) or yield spread premiums (compensation from investors for delivering higher interest rates). Some lenders offer no-cost loans by accepting higher rates, while others charge upfront fees for lower rates.

Neither approach is inherently superior. The optimal choice depends on how long you plan to keep the loan. If refinancing within three years seems likely, accepting a higher rate with no upfront fees may cost less overall. For long-term ownership in Lynnwood or Everett, paying points to secure a lower rate generates substantial savings.

Third-Party Service Costs

While lenders don't control third-party fees like title insurance, appraisals, and recording charges, they influence total costs through vendor selection. Established lenders with strong vendor relationships often negotiate better pricing than smaller operations.

Compare third-party costs across Loan Estimates carefully. Significant variations may indicate inflated fees or inefficient vendor networks. Resources for comparing loan offers help you understand which costs you can shop for and which remain fixed.

Pre-Approval Strength and Underwriting Standards

Pre-approval quality varies dramatically among home loan lenders. Understanding these differences helps you present the strongest possible offer in competitive situations.

Comprehensive vs. Basic Pre-Approvals

Basic pre-qualification involves minimal documentation and provides rough affordability estimates. These letters carry little weight with sellers and their agents, particularly in multiple-offer scenarios common throughout Seattle neighborhoods.

Comprehensive pre-approvals include full income verification, credit review, asset documentation, and preliminary underwriting approval. Some lenders submit complete files to underwriting before issuing pre-approval letters, providing the highest confidence level possible before finding a property.

Conditional Approval Advantages

The strongest pre-approvals come from lenders who complete full underwriting based on your financial documentation, issuing conditional approval subject only to property-specific items like appraisal and title. This approach nearly eliminates financing contingency risk from the seller's perspective.

For buyers competing in hot markets across Bellevue and Kirkland, demonstrating this approval strength can differentiate your offer from competitors with weaker financing commitments. Realtors recognize which lenders consistently deliver on these commitments and factor this reliability into offer strategy.

Questions to Ask Prospective Lenders

Direct conversations with potential home loan lenders reveal important details that don't appear in marketing materials or rate sheets. Prepare these questions before initial consultations to gather comparable information.

Essential qualification questions:

- What documentation do you need to verify my income type (W-2, RSUs, bonus, self-employed)?

- How do you calculate qualifying income for stock compensation?

- What credit score and debt-to-income ratios do you require for my target loan amount?

- Can you provide a detailed breakdown of all costs associated with my loan scenario?

- What is your current average timeline from application to closing for loans similar to mine?

Service and process questions:

- Who will be my primary point of contact throughout the process?

- How do you communicate status updates and respond to questions?

- Do you offer a mobile app or online portal for document upload and tracking?

- Can you provide references from recent clients with similar financial profiles?

- What happens if issues arise during underwriting or appraisal?

Lender responses reveal their expertise, technology capabilities, and service philosophy. Hesitant or vague answers about timelines, costs, or processes suggest potential problems ahead.

Local Market Expertise and Realtor Relationships

Seattle's diverse neighborhoods present unique challenges from condo financing rules in Capitol Hill high-rises to land-lease properties in certain areas. Home loan lenders with local expertise navigate these situations more effectively than national operations unfamiliar with regional nuances.

Understanding Regional Property Challenges

King County presents specific appraisal challenges, HOA documentation requirements, and property type limitations. Lenders experienced in Seattle markets know which condo buildings meet financing standards, how to address land-lease situations, and which appraisers deliver reliable valuations in niche neighborhoods.

This knowledge prevents surprises late in the transaction when addressing issues becomes costly and time-sensitive. For properties in Lake Forest Park or Mill Creek, confirming your lender's experience with similar transactions protects your earnest money and timeline.

Realtor Network Integration

Strong relationships between lenders and local realtors create collaboration benefits throughout your transaction. Realtors recommend lenders they trust to close on time with minimal complications. Lenders who consistently deliver on commitments earn these referrals through proven performance.

When interviewing lenders, ask which real estate teams they work with regularly and request references. Established local presence indicates market knowledge and operational excellence that benefits your transaction from offer through closing.

Selecting the right home loan lender requires evaluating multiple factors beyond advertised interest rates, from specialized expertise and technology platforms to communication standards and proven closing timelines. For Seattle-area homebuyers, particularly tech professionals with complex compensation structures, partnering with experienced local experts who understand regional market dynamics and can qualify diverse income sources maximizes your buying power and streamlines your financing experience. Keith Akada brings over 25 years of mortgage expertise to clients throughout Seattle, Bellevue, Redmond, and Kirkland, with specialized knowledge in qualifying RSUs, stock options, and bonus income for tech professionals at Amazon, Microsoft, and Google. With 750+ five-star reviews and the ability to close loans in as few as 9 business days, Mortgage Reel delivers the proactive guidance and reliable execution you need to succeed in competitive Pacific Northwest real estate markets.