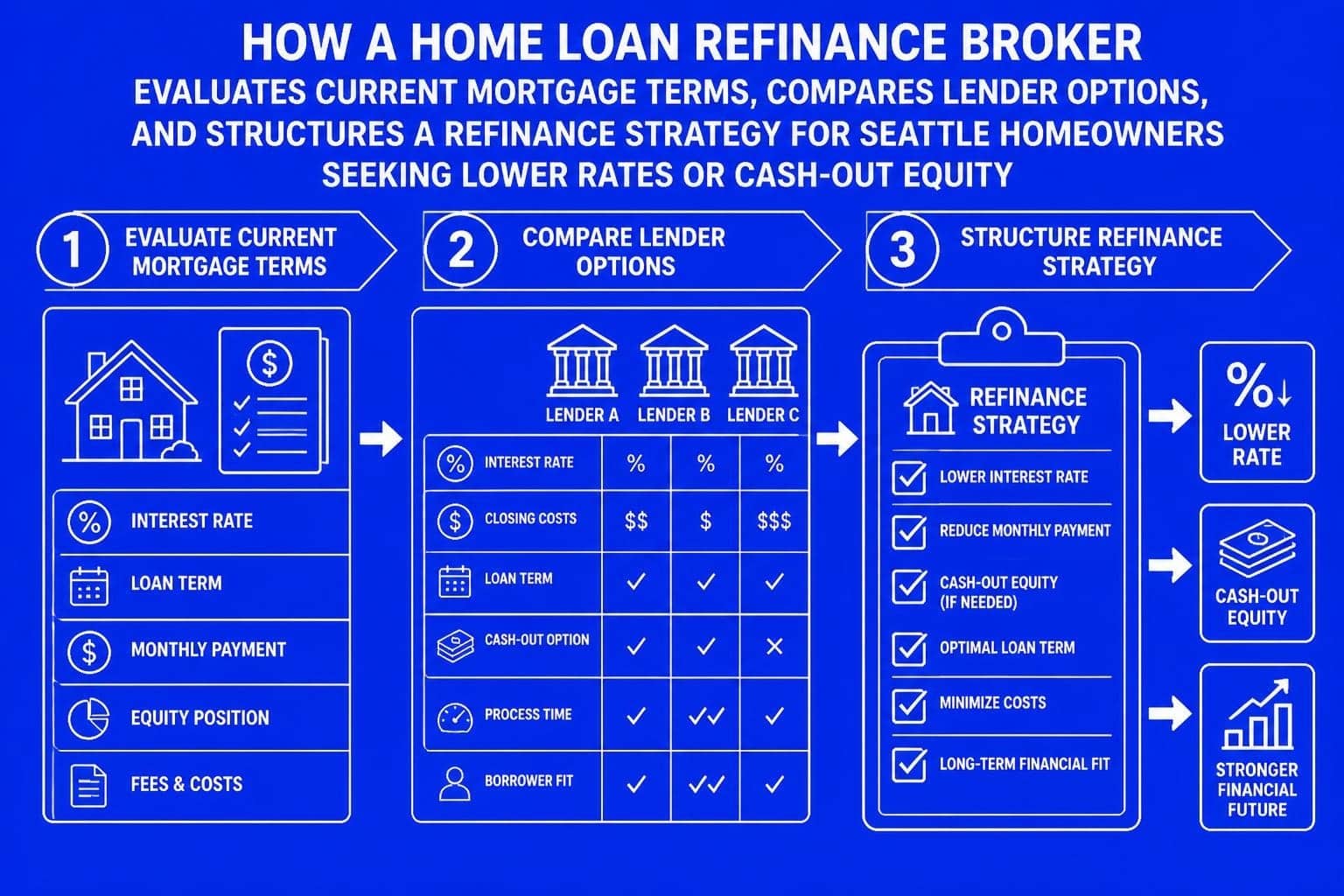

Refinancing your home loan can unlock significant financial benefits, but navigating the complex landscape of lenders, rates, and loan programs requires expertise. A home loan refinance broker serves as your advocate throughout the process, analyzing your current mortgage terms, evaluating market conditions, and connecting you with lending solutions that align with your financial goals. For Seattle homeowners-whether in Bellevue, Redmond, Kirkland, or surrounding areas-working with an experienced refinance broker can mean the difference between marginal savings and a transformative financial outcome. This guide explains how these professionals operate, when refinancing makes sense, and what to expect when partnering with a broker in the competitive Pacific Northwest housing market.

Understanding the Role of a Home Loan Refinance Broker

A home loan refinance broker acts as an intermediary between borrowers and lenders, offering access to multiple loan products rather than the limited options available through a single bank. Unlike loan officers employed by specific institutions, brokers maintain relationships with numerous lenders, enabling them to shop your scenario across various programs to find optimal terms.

How Brokers Differ from Direct Lenders

The distinction between brokers and direct lenders significantly impacts your refinancing experience:

- Access to Multiple Lenders: Brokers submit your application to several institutions simultaneously, increasing approval odds and competitive pricing

- Specialized Expertise: Many brokers focus on complex income scenarios, including stock compensation common among Seattle tech professionals

- Negotiating Power: Established brokers often secure rate concessions or reduced fees through high-volume lender relationships

- Personalized Service: Brokers typically handle fewer clients than bank loan officers, providing more attentive guidance

Direct lenders offer their own products exclusively, which can limit options but may streamline processing if you already have an established banking relationship. For refinancing specifically, the broker model frequently delivers better outcomes because rate differences of even 0.125% compound significantly over loan terms.

Core Services Provided by Refinance Brokers

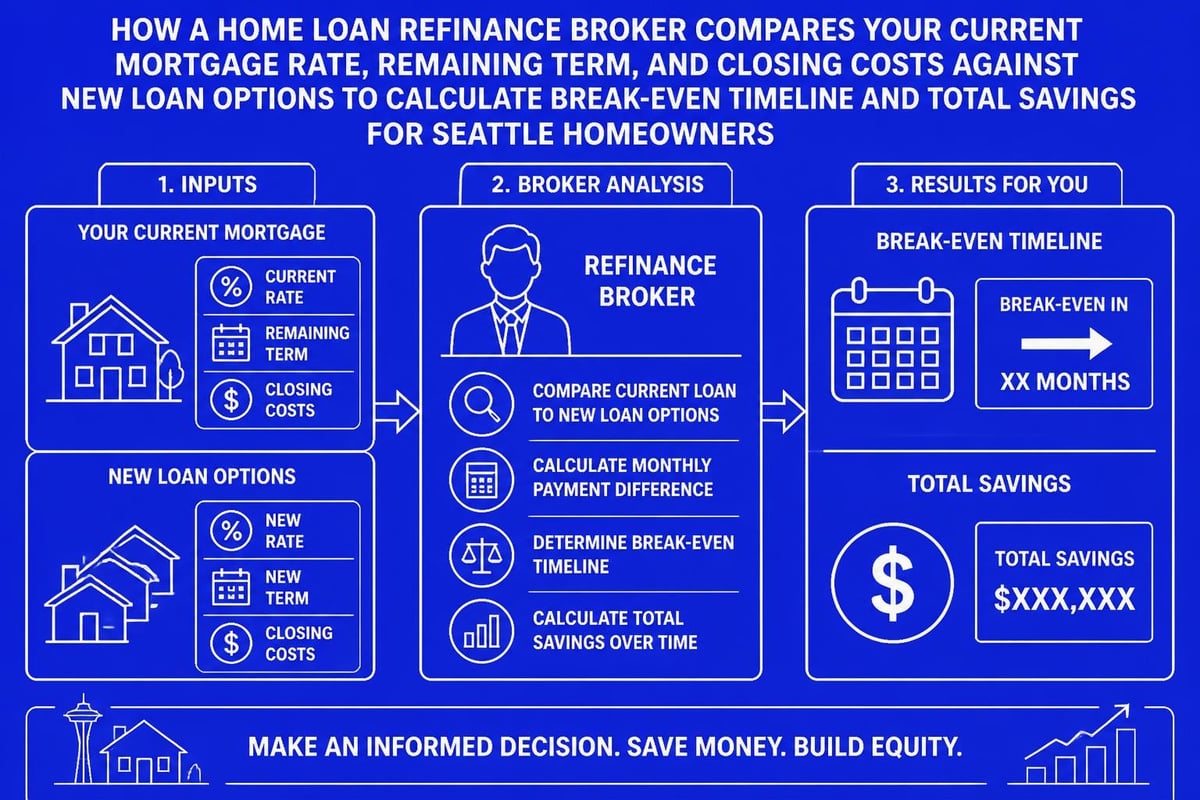

Professional brokers deliver comprehensive support beyond simple loan placement. They analyze your current mortgage against potential replacement options, calculating break-even points to determine whether refinancing makes financial sense. They also prepare your application package, ensuring documentation meets underwriting standards before submission.

Most importantly, experienced brokers educate clients about program guidelines, explaining the implications of loan-to-value ratios, debt-to-income calculations, and credit requirements. This transparency empowers homeowners to make informed decisions rather than accepting the first available offer.

When Refinancing Makes Financial Sense

Refinancing isn't universally beneficial-timing and circumstances determine whether the costs justify the benefits. A knowledgeable home loan refinance broker evaluates multiple factors before recommending action.

Rate Reduction Scenarios

The traditional refinancing trigger involves securing a lower interest rate. Generally, a reduction of 0.5% or more justifies refinancing costs, though this threshold varies based on loan size and remaining term. For a $600,000 mortgage in Seattle-common in neighborhoods like Bellevue and Redmond-reducing your rate from 6.5% to 6.0% saves approximately $185 monthly and $66,600 over 30 years.

However, raw savings don't tell the complete story. Brokers calculate the break-even point by dividing closing costs by monthly savings. If refinancing costs $8,000 and saves $185 monthly, you break even in 43 months. Homeowners planning to relocate before reaching this threshold shouldn't refinance based solely on rate reduction.

Equity Access Strategies

Cash-out refinancing allows homeowners to convert accumulated equity into liquid funds. Seattle's robust appreciation has created substantial equity for many homeowners who purchased before 2020. A home loan refinance broker can structure cash-out scenarios for various purposes:

| Use Case | Typical Amount | Loan-to-Value Limit |

|---|---|---|

| Home improvements | $50,000-$150,000 | 80% conventional |

| Debt consolidation | $25,000-$100,000 | 80% conventional |

| Investment property down payment | $100,000-$300,000 | 75-80% depending on credit |

| Business funding | Variable | 75-80% depending on debt ratios |

When executed strategically, cash-out refinancing provides capital at substantially lower rates than personal loans, credit cards, or home equity lines of credit. Brokers ensure you maintain adequate equity cushion while accessing necessary funds.

Loan Term Modifications

Refinancing from a 30-year to a 15-year mortgage accelerates equity building and reduces total interest paid. Conversely, extending to a longer term lowers monthly obligations, helpful during income transitions or when managing other financial priorities. Understanding mortgage financing options allows you to align your loan structure with evolving financial circumstances.

The Refinancing Process with a Professional Broker

Working with a home loan refinance broker follows a structured timeline, typically spanning 20-45 days from application to closing. Understanding each phase helps set realistic expectations and ensures smooth execution.

Initial Consultation and Strategy Session

The process begins with a comprehensive review of your current mortgage and financial situation. Your broker requests documentation including:

- Current mortgage statement showing principal balance, interest rate, and monthly payment

- Recent pay stubs and W-2s or tax returns for self-employed borrowers

- Asset statements for down payment and reserves

- Credit authorization for preliminary underwriting review

For Seattle tech professionals with equity compensation, brokers specializing in complex income scenarios-like those at firms serving Amazon, Microsoft, and Google employees-know how to properly document RSUs, ESPP income, and annual bonuses for maximum qualifying power. This expertise proves invaluable when conventional documentation approaches understate actual earnings capacity.

Application and Lender Selection

After analyzing your scenario, your broker presents options from multiple lenders with detailed cost-benefit comparisons. This presentation should include:

- Interest rate and annual percentage rate (APR) for each option

- Estimated closing costs broken down by category

- Monthly payment calculations including principal, interest, taxes, and insurance

- Break-even analysis showing when savings exceed costs

- Cash-to-close requirements if applicable

Transparent brokers explain rate lock strategies, helping you decide whether to secure rates immediately or float based on market conditions. With current Seattle mortgage rates subject to daily fluctuation, this timing decision significantly impacts final terms.

Underwriting and Appraisal Coordination

Once you select a lender and lock your rate, the file enters underwriting. Your broker coordinates the appraisal, ensuring the appraiser has access to your property and understands relevant market dynamics. In competitive Seattle submarkets like Kirkland and Shoreline, appraisals occasionally come in below expected values, requiring brokers to advocate for reconsideration or adjust transaction structure.

Underwriters review documentation for accuracy and compliance with lending guidelines. Conditions typically request clarification on income sources, asset deposits, or credit inquiries. Experienced brokers anticipate these requests, often providing explanations proactively to accelerate approval.

Qualifying for Refinancing in Seattle Markets

Refinancing qualification standards mirror purchase requirements but include additional considerations specific to existing mortgages. A professional home loan refinance broker ensures you meet all criteria before submitting applications.

Credit Score Requirements

Minimum credit scores vary by loan type and loan-to-value ratio:

| Loan Program | Minimum Score | Optimal Score for Best Rates |

|---|---|---|

| Conventional | 620 | 740+ |

| FHA | 580 (500 with 10% equity) | 680+ |

| VA | No minimum (lender overlays apply) | 680+ |

| Jumbo | 680-700 | 740+ |

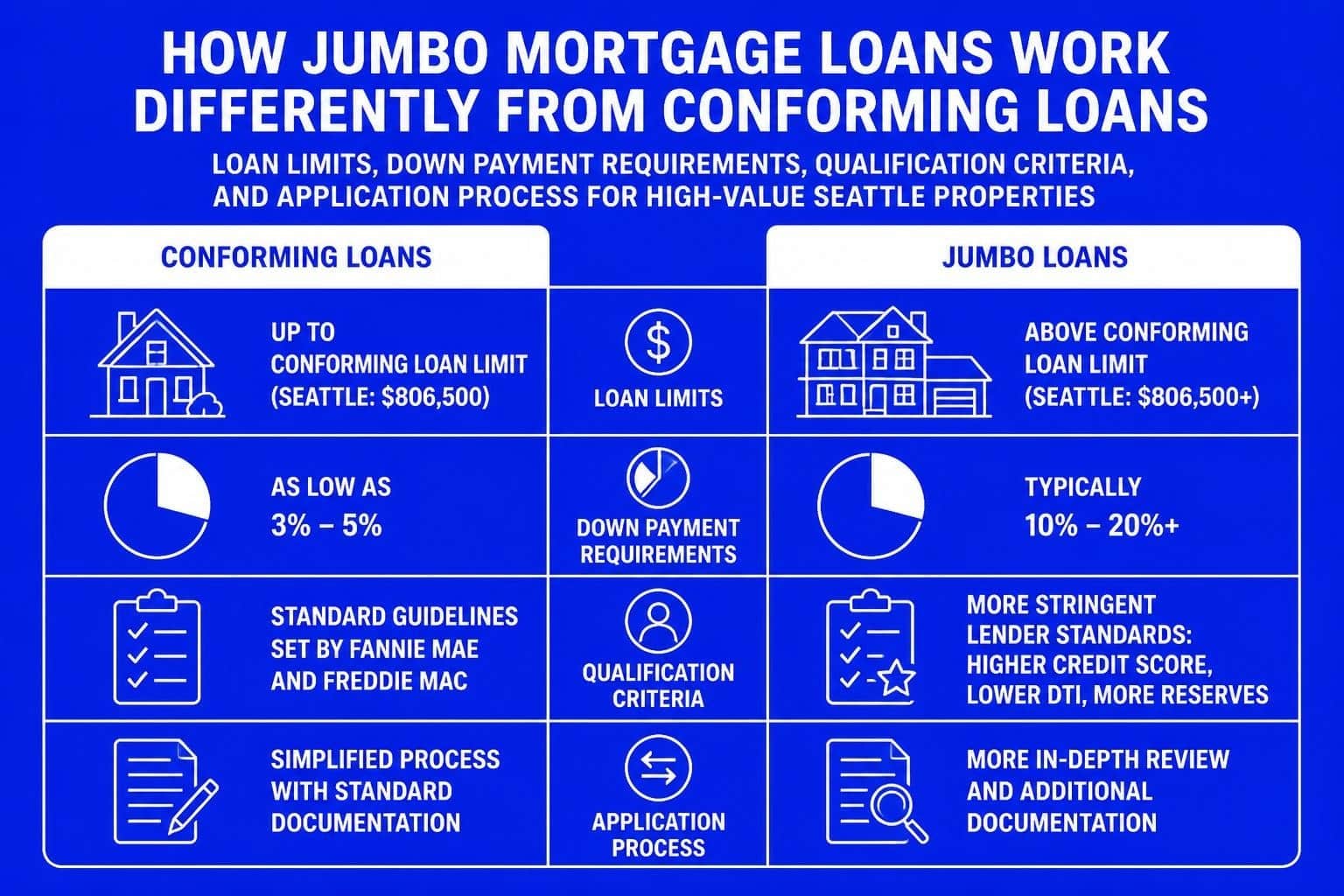

Seattle's high-value homes frequently require jumbo home loan refinancing, where credit standards tighten and score optimization becomes critical. Brokers guide score improvement strategies, including timing payoffs and disputing inaccuracies before application.

Equity and Loan-to-Value Calculations

Most refinance programs require at least 20% equity to avoid private mortgage insurance. Your loan-to-value ratio divides the new loan amount by current property value. For a home valued at $850,000, maintaining 20% equity means refinancing no more than $680,000.

Cash-out refinancing reduces equity, potentially triggering mortgage insurance requirements. Skilled brokers structure transactions to maximize cash access while staying below program thresholds. In appreciating markets like Mill Creek and Lake Forest Park, strategic timing can mean the difference between qualifying for preferred terms or facing restrictive guidelines.

Income Documentation for Complex Earners

Standard W-2 employment documentation suffices for most refinancing scenarios, but Seattle's concentration of tech professionals introduces complexity. Brokers experienced with good mortgage broker practices understand how to qualify:

- Restricted Stock Units (RSUs): Two-year average of vesting schedules with continuation likelihood verification

- Bonuses: Typically requires two-year history demonstrating consistency

- Stock Options: Exercised gains with documentation of vesting terms

- Supplemental Income: Rental property cash flow, investment dividends, or part-time earnings

Properly documenting these income sources maximizes borrowing capacity, potentially qualifying you for better properties or larger cash-out amounts than conventional documentation approaches would allow.

Cost Considerations and Fee Structures

Understanding the complete cost picture enables informed comparison between refinancing offers. A transparent home loan refinance broker itemizes all fees and explains which costs are negotiable versus fixed by third parties.

Typical Closing Costs Breakdown

Refinancing closing costs in Seattle typically range from 2% to 5% of the loan amount. For a $600,000 refinance, expect $12,000 to $30,000 in total costs:

- Lender Fees: Origination, underwriting, processing ($1,500-$3,500)

- Third-Party Services: Appraisal, title insurance, escrow ($2,500-$4,000)

- Prepaid Items: Property taxes, homeowners insurance, interest ($5,000-$15,000 depending on timing)

- Recording and Transfer Fees: County-specific charges ($200-$800)

Some costs remain constant regardless of lender selection, while others vary significantly. Brokers negotiate lender fees, sometimes securing credits that offset third-party costs or reduce your interest rate through discount points.

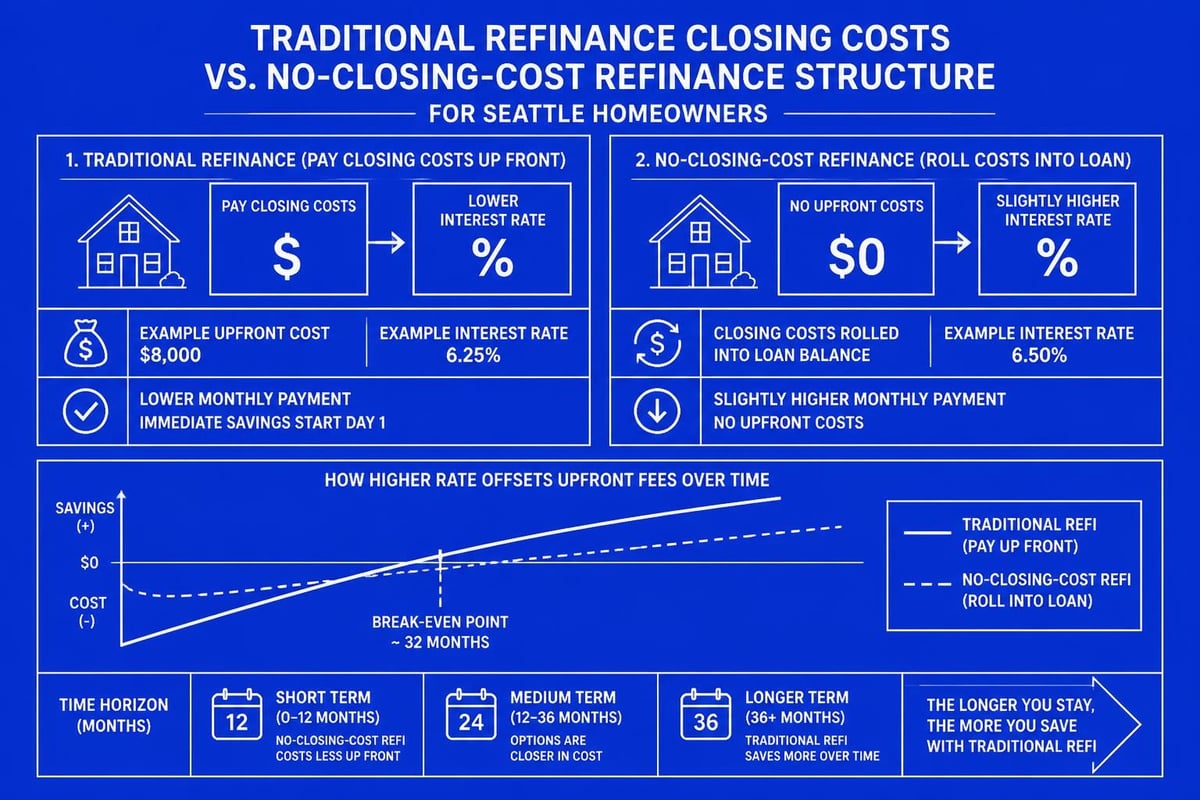

No-Closing-Cost Refinancing Options

Homeowners reluctant to pay upfront costs can choose no-closing-cost refinancing, where the lender covers fees in exchange for a slightly higher interest rate. This approach makes sense for borrowers planning to relocate within five years or expecting rates to drop further, enabling another refinance without recovering initial costs.

Your broker should present both traditional and no-closing-cost scenarios with accurate break-even calculations. Beware of brokers who push one option without explaining alternatives-transparency indicates client-focused service rather than commission optimization.

Selecting the Right Home Loan Refinance Broker

Not all brokers deliver equivalent value. Seattle homeowners should evaluate expertise, reputation, and service quality before committing to a professional relationship.

Essential Qualifications and Experience

Licensed mortgage brokers must hold NMLS credentials and maintain continuing education requirements. Beyond baseline licensing, look for:

- Years of Experience: Minimum five years navigating market cycles and guideline changes

- Local Market Knowledge: Familiarity with Seattle-area appraisal challenges, property tax considerations, and municipality-specific requirements

- Specialization Alignment: If you have complex income, investment properties, or unique scenarios, choose brokers with demonstrated expertise in those areas

- Technology Integration: Brokers leveraging digital documentation, electronic signatures, and online portals streamline the process significantly

Request references from clients with similar financial profiles. A broker experienced with $400,000 condos in Everett may lack the expertise needed for $1.5 million estates in Bellevue requiring specialized jumbo mortgage underwriting.

Reviewing Track Record and Client Feedback

Online reviews provide insight into service quality and execution reliability. Look for consistent themes in feedback:

- Communication Frequency: Do clients feel informed throughout the process?

- Problem Resolution: How does the broker handle appraisal issues, underwriting conditions, or timeline pressures?

- Rate Competitiveness: Do reviewers mention securing favorable terms compared to other quotes?

- Closing Timeline: Does the broker consistently meet projected timelines?

Brokers with 100+ five-star reviews demonstrate sustained service excellence. Be cautious of limited feedback or recent negative patterns indicating deteriorating service quality.

Questions to Ask During Initial Consultations

Schedule consultations with at least three brokers before selecting your refinancing partner. Use these questions to evaluate competency and fit:

- How many lenders do you work with, and which specialize in my loan type?

- What are your current rate quotes for my scenario, and what factors might change those rates?

- How do you charge for your services-lender-paid compensation, borrower-paid fees, or both?

- What's your typical timeline from application to closing, and what drives delays?

- How do you handle appraisals that come in below expected value?

Strong brokers answer confidently with specific examples from recent transactions. Vague responses or pressure to commit immediately suggest less experienced or client-focused service.

Maximizing Refinancing Benefits in 2026

Current market conditions create specific opportunities and challenges for Seattle homeowners considering refinancing. A knowledgeable home loan refinance broker adapts strategies to prevailing economic factors.

Interest Rate Environment Strategies

Mortgage rates in 2026 reflect Federal Reserve policy responses to inflation and employment data. When rates decline from recent highs, refinancing volume surges as homeowners locked into higher rates seek savings. Conversely, rising rate environments reduce conventional refinancing activity but increase interest in adjustable-rate mortgages (ARMs) or alternative strategies.

Your broker should explain rate lock timing options, including float-down provisions that protect against rate increases while allowing you to capture decreases before closing. This flexibility proves especially valuable during volatile rate periods.

Property Value Considerations in Seattle Submarkets

Seattle-area home values vary significantly by neighborhood. Downtown Seattle condos, Lynnwood single-family homes, and Shoreline properties each follow distinct appreciation patterns. Your refinancing strategy should account for local market dynamics:

- High-Appreciation Areas: Recently appraised values may exceed tax assessments, creating cash-out opportunities

- Stable Markets: Reliable valuations simplify refinancing but limit equity extraction

- Cooling Markets: Strategic appraisal timing becomes critical to avoid value gaps that derail transactions

Brokers with deep local knowledge anticipate appraisal challenges and sometimes recommend delaying refinancing until market conditions improve or property improvements increase value beyond refinancing thresholds.

Tax Implications and Deduction Strategies

Refinancing affects tax deductions through mortgage interest and potential points paid at closing. Current tax law limits mortgage interest deductions to $750,000 in loan principal for mortgages originated after December 15, 2017. Cash-out refinancing for investment purposes may maintain deductibility, while personal use funds create more complex tax treatment.

Consult tax professionals about your specific situation, but work with brokers who understand basic tax implications and can coordinate timing to optimize deductibility. For example, closing late in the year maximizes current-year interest deductions if you itemize.

Specialized Refinancing Scenarios

Beyond standard rate-and-term refinancing, home loan refinance brokers structure solutions for unique situations requiring specialized knowledge and lender relationships.

Investment Property Refinancing

Refinancing rental properties follows stricter guidelines than primary residences. Lenders require:

- Higher credit scores (typically 680-720 minimum)

- Lower loan-to-value ratios (70-80% maximum)

- Rental income documentation through leases and tax returns

- Larger reserve requirements (six months of mortgage payments minimum)

Seattle's strong rental market supports investment property ownership across Redmond, Kirkland, and Bellevue. Brokers specializing in investor clients structure refinancing that consolidates debt, extracts equity for additional property purchases, or converts higher-rate commercial loans to residential financing.

FHA Streamline and VA IRRRL Programs

Government-backed mortgages offer streamlined refinancing with reduced documentation:

FHA Streamline Refinancing:

- No appraisal required in most cases

- No income verification needed

- Must demonstrate net tangible benefit (lower payment or stable payment with term reduction)

- Limited cash-out (maximum $500)

VA Interest Rate Reduction Refinance Loan (IRRRL):

- Available to veterans with existing VA loans

- No appraisal typically required

- Minimal documentation

- Funding fee can be financed into loan amount

- Excellent option for VA loan holders seeking rate reductions

These programs expedite refinancing and reduce costs significantly compared to conventional options. Brokers familiar with program nuances ensure you leverage all available benefits while avoiding disqualifying mistakes.

Removing Private Mortgage Insurance

Homeowners who purchased with less than 20% down payment carry private mortgage insurance (PMI), adding $100-$300 monthly to housing costs. Once equity reaches 20% through appreciation or principal paydown, refinancing eliminates this expense permanently.

Calculate whether refinancing costs justify PMI elimination. If your home appreciated from $600,000 to $750,000 and your loan balance dropped to $580,000, your loan-to-value ratio improved from 93% to 77%. Refinancing eliminates $200 monthly PMI, creating $2,400 annual savings that quickly recovers closing costs.

Brokers should compare refinancing against requesting PMI cancellation through your current lender, which may avoid closing costs if your loan-to-value ratio supports removal without refinancing.

Technology and the Modern Refinancing Experience

Digital tools have transformed how home loan refinance brokers serve clients, enabling faster processing, better communication, and enhanced transparency throughout the refinancing journey.

Digital Documentation and Application Systems

Modern brokers utilize secure portals where clients upload documents, sign disclosures electronically, and track application progress in real-time. This technology eliminates mailing delays and creates audit trails ensuring compliance with lending regulations.

Mobile-responsive platforms allow you to complete tasks from any device, particularly valuable for busy professionals balancing work responsibilities with refinancing requirements. Look for brokers offering digital-first experiences while maintaining personal communication for complex questions requiring nuanced explanation.

Automated Underwriting and Faster Closings

Lenders increasingly rely on automated underwriting systems that evaluate loan files against program guidelines within minutes. While human underwriters still review documentation, automation identifies potential issues early, allowing brokers to address concerns before formal submission.

Some lenders now close refinances in as few as 9-15 business days when files include complete documentation and straightforward income verification. This acceleration benefits rate-lock strategy by reducing exposure to market fluctuations between application and closing.

Rate Monitoring and Timing Tools

Sophisticated brokers provide rate tracking tools that alert you when market conditions favor refinancing. These systems monitor your current mortgage against prevailing rates, calculating potential savings and notifying you when thresholds justify action.

This proactive approach ensures you capitalize on favorable rate movements rather than missing opportunities through inattention or delayed response.

Working with an experienced home loan refinance broker provides Seattle homeowners with expert guidance, competitive rate access, and personalized service that self-directed refinancing rarely achieves. By understanding the refinancing process, qualification requirements, and specialized scenarios, you can confidently evaluate whether refinancing aligns with your financial goals and select the right professional to execute your strategy. Keith Akada at Mortgage Reel brings over 25 years of experience helping Seattle, Bellevue, Redmond, and Kirkland homeowners navigate refinancing decisions with transparency, strategic insight, and proven execution. With 750+ five-star reviews and specialized expertise in complex income scenarios including stock compensation and jumbo loans, Keith delivers the personalized guidance and competitive terms you need to make confident refinancing decisions.