Purchasing your first home represents one of the most significant financial milestones in your life, and navigating the landscape of home loans first home buyers encounter can feel overwhelming without proper guidance. In Seattle's competitive real estate market, where median home prices continue to challenge affordability, understanding your financing options becomes critical to success. This comprehensive guide breaks down the essential mortgage programs, down payment strategies, and qualification requirements that empower first-time buyers across Seattle, Bellevue, Redmond, Kirkland, and surrounding communities to make confident decisions in 2026.

Understanding Home Loan Options for First-Time Buyers

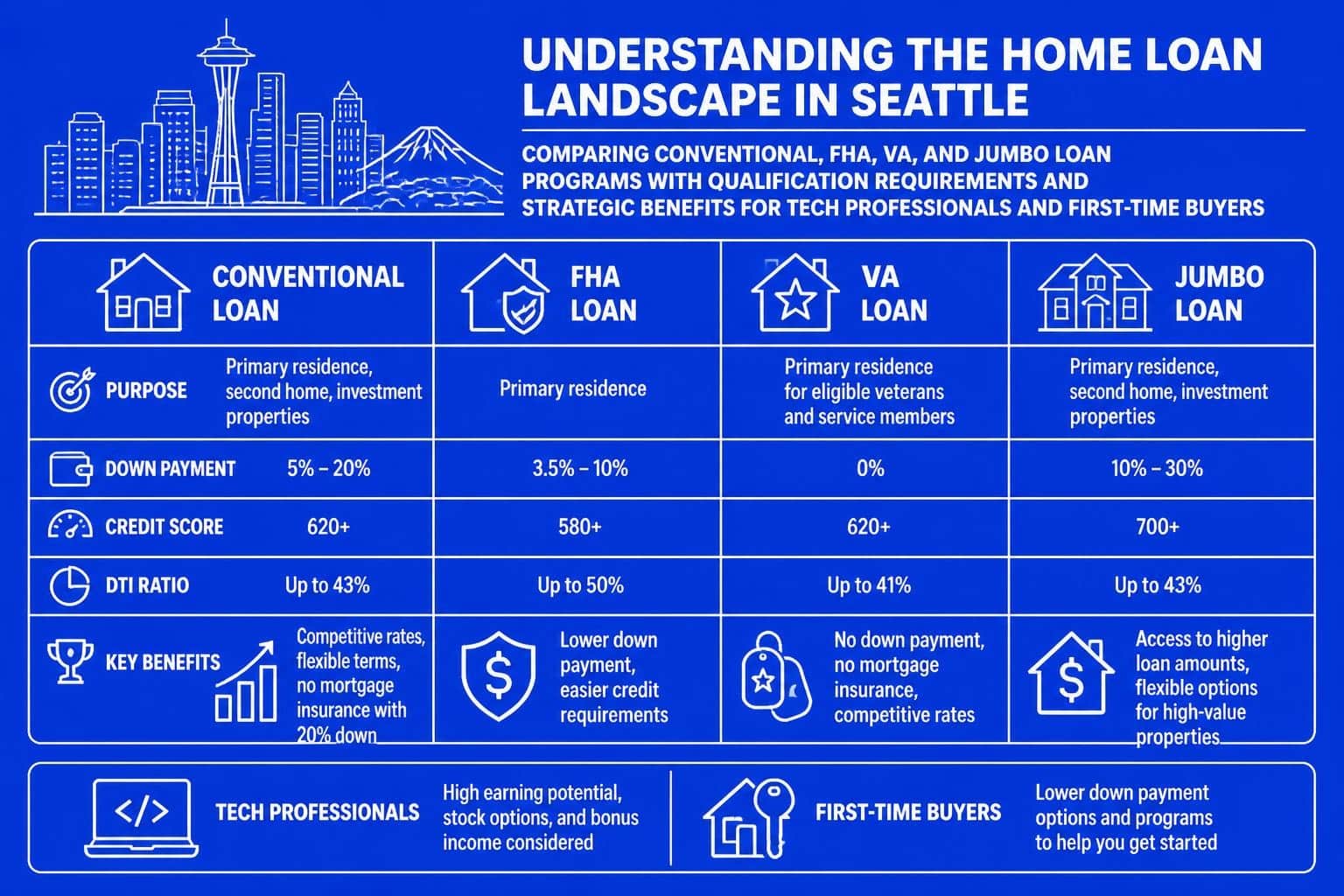

The mortgage industry offers several distinct loan programs designed specifically to help home loans first home buyers can access with varying credit profiles and financial situations. Each program carries unique advantages, requirements, and cost structures that align with different buyer circumstances.

Conventional Loans with Low Down Payment

Conventional mortgages remain the most popular choice for qualified buyers, offering flexibility and competitive rates. Conventional loans with as little as 5% down enable Seattle-area buyers to enter homeownership sooner without waiting years to accumulate a traditional 20% down payment.

Key benefits of conventional financing include:

- Loan amounts up to $806,500 in 2026 for King County conforming limits

- Private mortgage insurance (PMI) that drops off automatically at 78% loan-to-value

- Flexible property type eligibility including condos, townhomes, and single-family homes

- Competitive interest rates for borrowers with strong credit scores

Private mortgage insurance typically adds $50 to $200 monthly for every $100,000 borrowed, depending on your down payment percentage and credit score. This cost decreases as you build equity and disappears completely once you reach 22% equity through payments or appreciation.

For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, conventional loans often provide the best path forward. Stock compensation, RSUs, and bonus income can be qualified when properly documented, significantly increasing purchasing power in neighborhoods like Bellevue, Redmond, and Kirkland where home prices exceed regional medians.

FHA Loans: Accessible Financing with Lower Barriers

Federal Housing Administration (FHA) loans provide an accessible entry point for buyers who may not qualify for conventional financing due to credit challenges or limited savings. These government-backed mortgages require just 3.5% down for borrowers with credit scores of 580 or higher, making them particularly valuable in expensive markets like Seattle.

FHA home loans offer several advantages that benefit first-time buyers:

- Minimum credit scores as low as 580 (some lenders accept 500 with 10% down)

- Gift funds allowed for entire down payment and closing costs

- Seller concessions up to 6% of purchase price permitted

- More lenient debt-to-income ratio guidelines

The trade-off involves mortgage insurance costs. FHA requires both an upfront mortgage insurance premium (1.75% of the loan amount) and monthly mortgage insurance that persists for the life of the loan on purchases with less than 10% down. For a $500,000 purchase in Shoreline with 3.5% down, expect approximately $400 monthly in mortgage insurance costs.

Despite higher insurance costs, FHA loans remain highly valuable for buyers rebuilding credit after financial setbacks or those working in service industries with steady but moderate incomes. Cities like Lynnwood and Everett, where home prices trend below Seattle's core neighborhoods, become more accessible through FHA financing.

VA Loans for Military Service Members

Veterans, active-duty service members, and eligible surviving spouses gain access to arguably the most powerful home loan program available. VA loans require zero down payment, charge no monthly mortgage insurance, and offer competitive interest rates that typically beat conventional options.

The VA program enables qualified buyers to purchase homes throughout the Greater Seattle area without depleting savings for down payments. This preserved capital can fund moving expenses, home improvements, or remain as emergency reserves-a critical advantage in expensive housing markets.

VA loan highlights include:

| Feature | Benefit |

|---|---|

| Down Payment | $0 required |

| Mortgage Insurance | None |

| Closing Costs | Seller can pay up to 4% |

| Credit Requirements | Flexible, no minimum score |

The funding fee (typically 2.3% for first-time use) represents the primary cost, though veterans with service-connected disabilities receive a complete exemption. This fee can be rolled into the loan amount rather than paid upfront, preserving cash for other homeownership expenses.

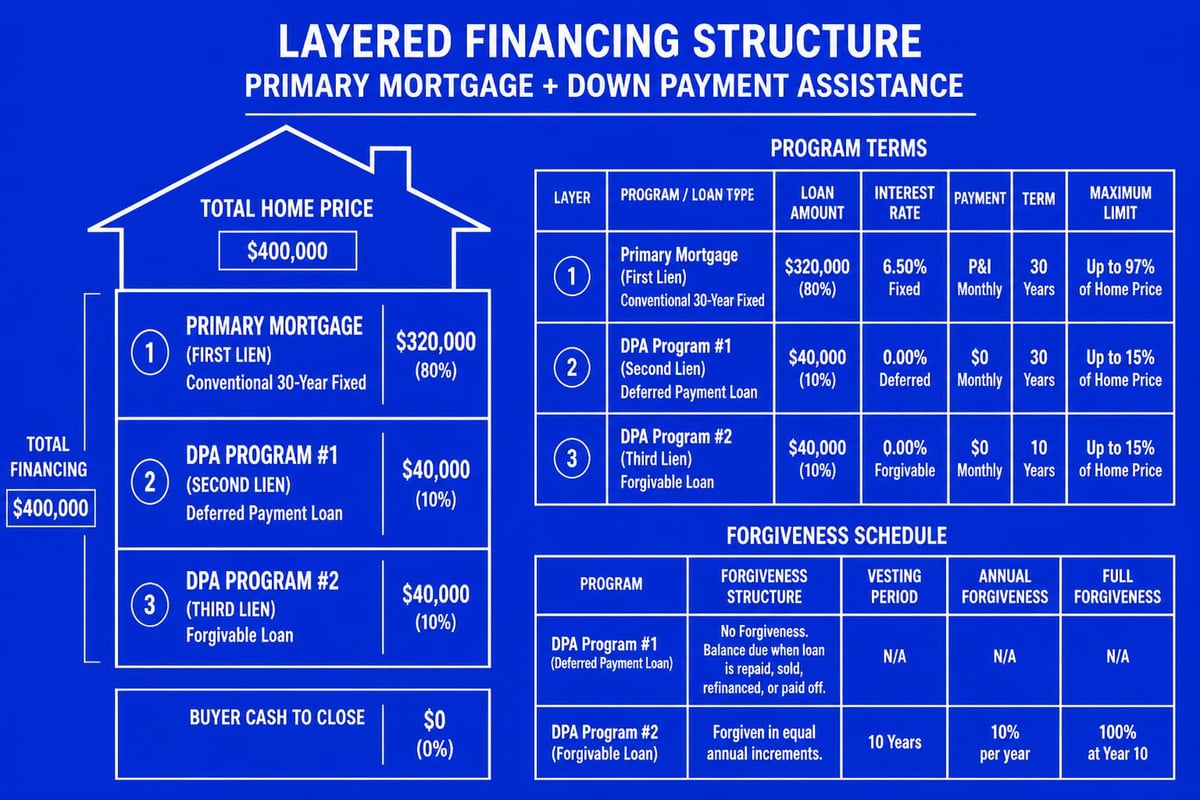

Down Payment Strategies and Assistance Programs

Coming up with a down payment presents the single largest hurdle for home loans first home buyers face in 2026. Seattle's median home price of approximately $800,000 means even a modest 5% down payment requires $40,000-a substantial sum for most first-time buyers.

How Much Down Payment Do You Really Need?

The persistent myth of the 20% down payment requirement prevents countless qualified buyers from exploring homeownership options. In reality, numerous loan programs accept down payments between 3% and 5%, making ownership accessible years earlier than traditional advice suggests.

Minimum down payment requirements by loan type:

- Conventional: 3% for first-time buyers, 5% for repeat buyers

- FHA: 3.5% with 580+ credit score

- VA: 0% for eligible veterans

- USDA: 0% in eligible rural areas (limited availability near Seattle)

A smaller down payment means higher monthly costs due to mortgage insurance, but this trade-off often makes financial sense. Waiting three additional years to save 20% down while paying rent and watching home prices appreciate 4-6% annually can cost significantly more than paying PMI for several years.

For a Mill Creek couple earning $150,000 annually, purchasing now with 5% down versus waiting three years to accumulate 20% illustrates this dynamic. If home prices appreciate just 5% annually, a $600,000 home today costs $695,000 in three years-requiring $139,000 down payment instead of the original $30,000, a difference of $109,000 in additional savings needed.

First-Time Buyer Assistance Programs

Washington State and local municipalities offer several programs that reduce upfront costs for qualified buyers. The Washington State Housing Finance Commission provides down payment assistance loans and favorable interest rates for income-eligible households across Seattle, Lake Forest Park, and surrounding communities.

Various loan options for first-time home buyers combine with local assistance to create affordable pathways. Working with an experienced Seattle mortgage broker ensures you identify and access every available program that matches your situation.

King County's down payment assistance provides up to $75,000 in silent second mortgages for qualifying buyers, though income and purchase price limits apply. These programs require living in the home as your primary residence for specified periods, with forgiveness provisions that eliminate repayment obligations after the retention period.

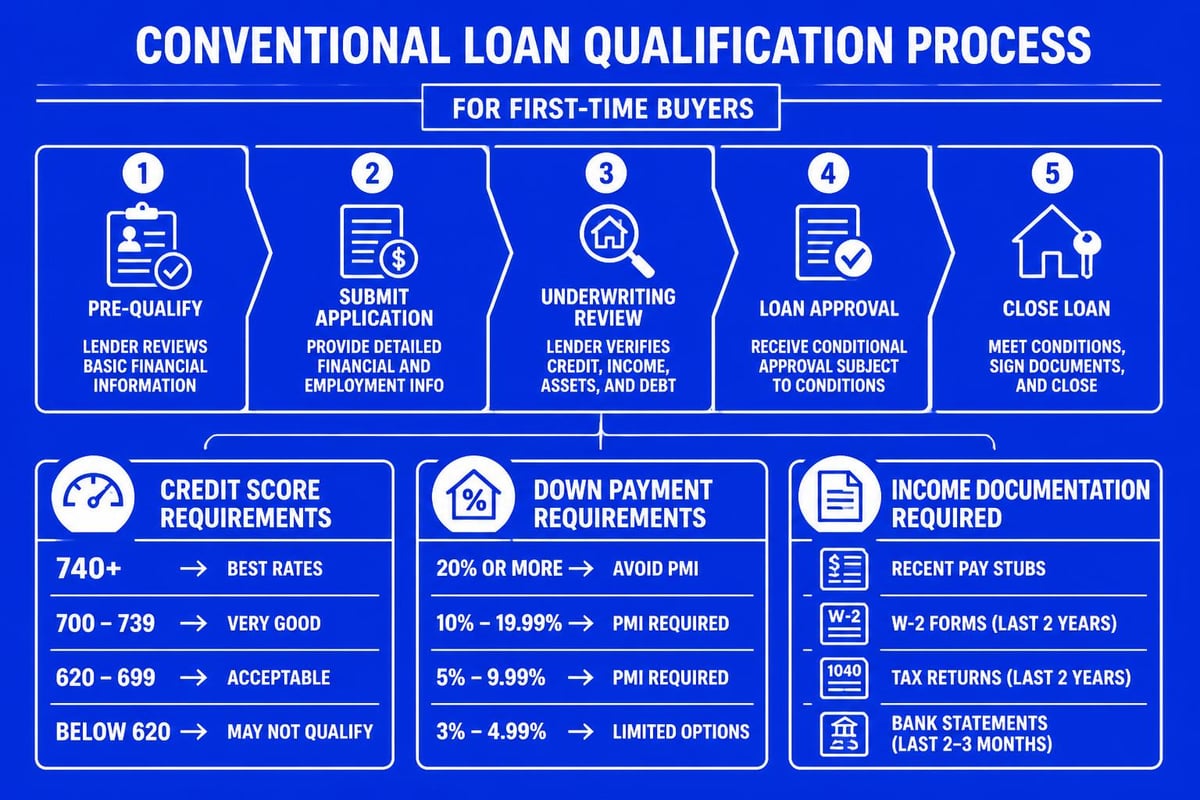

Qualifying for Your First Mortgage: What Lenders Evaluate

Understanding the qualification criteria for home loans first home buyers must meet enables strategic preparation months before you begin house hunting. Lenders evaluate three primary factors when determining approval and interest rates: credit history, income stability, and debt-to-income ratio.

Credit Score Requirements and Impact

Your credit score directly influences both approval likelihood and interest rate pricing. Every 20-point increment can shift your rate by 0.125% to 0.375%, translating to thousands in lifetime interest costs on a $500,000 mortgage.

Minimum credit scores by loan program:

- Conventional: 620 minimum, 740+ for best rates

- FHA: 580 for 3.5% down, 500 for 10% down

- VA: No official minimum, most lenders require 580-620

- Jumbo: Typically 700-720 minimum

For Seattle tech workers with stock compensation, maintaining excellent credit becomes particularly important because jumbo loan pricing (loans exceeding $806,500 in King County) penalizes lower credit scores more aggressively than conforming loans. A 680 credit score might add 0.500% to a jumbo rate compared to a 760 score-approximately $250 monthly on a $1 million mortgage.

Income Documentation for Traditional and Tech Employees

Lenders verify your ability to afford monthly payments through comprehensive income documentation. W-2 employees typically provide two years of tax returns, recent pay stubs, and employment verification. This straightforward process becomes more nuanced for tech professionals receiving substantial stock compensation.

Restricted Stock Units (RSUs), Employee Stock Purchase Plans (ESPPs), and annual bonuses require special handling. Generally, lenders average two years of such income and apply a percentage (often 70-100%) based on consistency. Microsoft employees in Redmond or Amazon workers in Seattle with three years of RSU vesting history can typically qualify the full amount when properly documented.

First-time home buyer specialists understand these nuances and structure documentation to maximize qualifying income. This expertise proves invaluable when competing for homes in Bellevue or Kirkland, where purchase prices frequently require optimizing every dollar of qualifying income.

Debt-to-Income Ratio Guidelines

Your debt-to-income (DTI) ratio compares total monthly debt obligations to gross monthly income. Most conventional loans cap DTI at 50%, though competitive scenarios often require 43% or lower for strong offers.

Common monthly debts included in DTI calculations:

- Proposed mortgage payment (principal, interest, taxes, insurance, HOA)

- Auto loans and leases

- Student loan payments

- Credit card minimum payments

- Personal loans

Notably, federal student loans in deferment or forbearance still require payment calculations based on either 0.5% of the balance or the documented payment amount. A $50,000 student loan balance adds approximately $250 to DTI calculations even when not currently in repayment.

Strategic debt management before applying for home loans first home buyers pursue can dramatically improve approval odds and purchasing power. Paying off a $15,000 auto loan with a $400 monthly payment effectively increases qualifying income by $400, potentially adding $60,000 to $80,000 in purchasing power.

Navigating Seattle's Competitive Housing Market

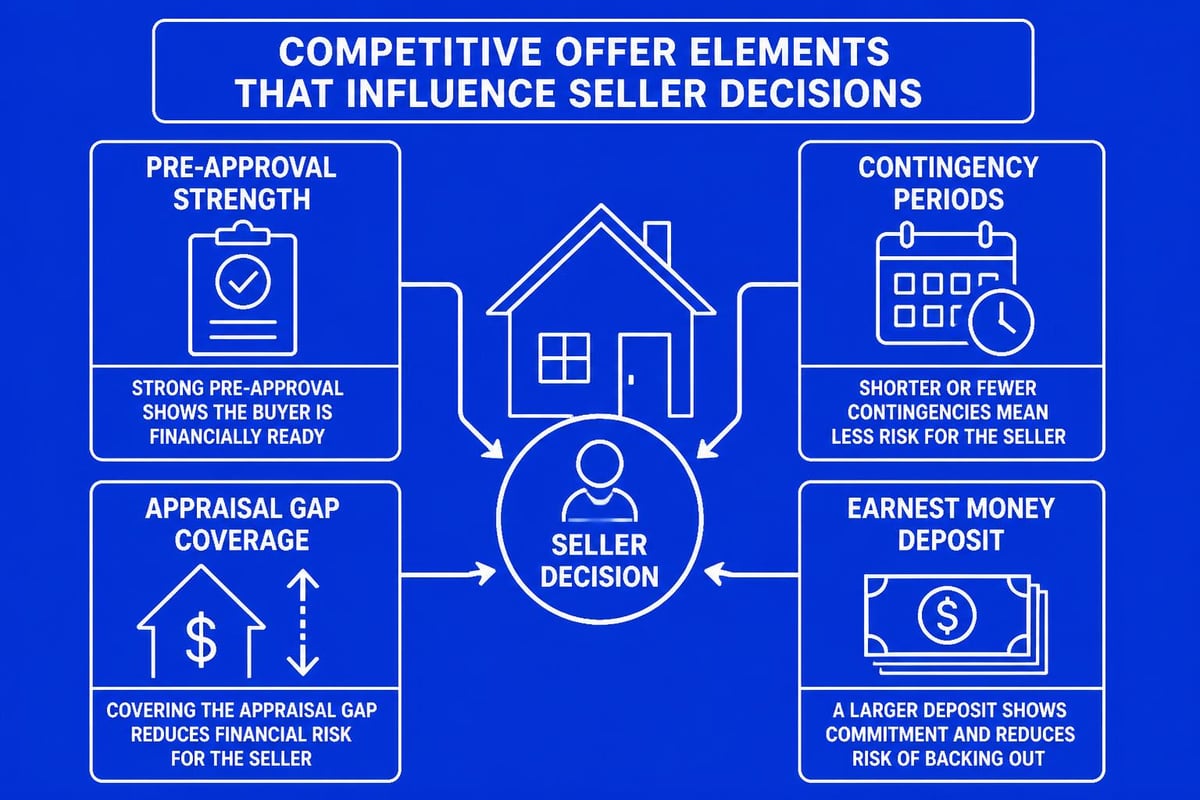

Seattle's real estate market demands strategic preparation beyond simple loan approval. Understanding home loan approval timelines and positioning yourself as a strong buyer creates competitive advantages when multiple offers compete for desirable properties.

Pre-Approval Versus Pre-Qualification

Many first-time buyers confuse pre-qualification with pre-approval, but sellers and listing agents recognize critical differences. Pre-qualification provides a rough estimate based on verbal information without verification. Pre-approval involves comprehensive documentation review, credit analysis, and conditional approval subject only to property-specific conditions.

In competitive Seattle neighborhoods, pre-approval becomes mandatory for serious consideration. Sellers receiving multiple offers prioritize buyers with verified financing, especially when working with reputable local lenders who close reliably. A comprehensive home buying strategy incorporates pre-approval as the foundation, not an afterthought.

Advanced underwriting takes pre-approval further by submitting your complete file to underwriting before finding a home. This process identifies and resolves potential issues early, enabling faster closing timelines that appeal to sellers. The ability to close in 9-12 business days versus the conventional 30-45 days provides a significant competitive edge.

Making Competitive Offers with Financing Contingencies

Wells Fargo’s first-time buyer resources emphasize the importance of understanding contingencies, particularly in competitive markets. The financing contingency protects buyers if loan approval falls through, but extended contingency periods weaken offer attractiveness.

Working with an experienced broker enables shorter contingency periods because pre-approval accuracy reduces uncertainty. A 10-day financing contingency from a trusted local lender carries more weight than a 21-day contingency from an unfamiliar online provider. Sellers recognize that local brokers understand regional appraisal practices and property-specific issues that affect financing.

Appraisal contingencies warrant particular attention in Seattle's market. When offering above comparable sales, consider appraisal gap coverage language that commits to paying $10,000 to $25,000 above appraised value from additional funds. This demonstrates financial capacity while maintaining some protection against significant appraisal shortfalls.

Financial Preparation Beyond the Down Payment

Successful home loans first home buyers secure require planning for costs beyond the down payment that many new buyers overlook. Comprehensive financial preparation prevents surprises and positions you for sustainable homeownership.

Closing Costs and Reserve Requirements

Closing costs typically range from 2% to 5% of the purchase price, adding $12,000 to $30,000 on a $600,000 home in areas like Shoreline or Mill Creek. These expenses include:

| Cost Category | Typical Range |

|---|---|

| Lender Fees | $1,500 – $3,000 |

| Title and Escrow | $2,000 – $4,000 |

| Appraisal | $600 – $800 |

| Pre-paid Property Taxes | $3,000 – $8,000 |

| Homeowner's Insurance | $1,200 – $2,400 |

| HOA Transfer Fees | $0 – $500 |

Reserve requirements ensure you maintain financial stability after closing. Conventional loans typically require two months of total housing payment in reserves, while jumbo loans may demand 6-12 months depending on loan amount and down payment. These reserves must remain liquid-retirement accounts don't count unless you're willing to document hardship withdrawals.

Gift funds from family members can cover down payment and closing costs, though documentation requirements apply. Donors must provide gift letters confirming the money requires no repayment, and paper trails proving fund transfers must be established. Programs assisting children with home purchases outline various structuring options for family support.

Budgeting for Ongoing Homeownership Costs

Monthly mortgage payments represent just one component of total housing costs. Property taxes in King County average 0.9% to 1.1% of assessed value annually-approximately $600 to $800 monthly on a $700,000 home. Homeowner's insurance adds another $150 to $250 monthly, while condo or townhome HOA fees range from $200 to $600+ depending on amenities.

Maintenance reserves prove critical for unexpected repairs and replacements. Financial advisors recommend budgeting 1% of home value annually for maintenance-$7,000 yearly or approximately $580 monthly for a $700,000 property. This fund covers roof repairs, HVAC replacements, and other inevitable expenses that renters never face.

Using budget planning spreadsheets helps visualize total housing costs and ensure mortgage payments don't overextend your finances. These tools enable scenario planning for various price points, helping you identify comfortable payment ranges before beginning your search.

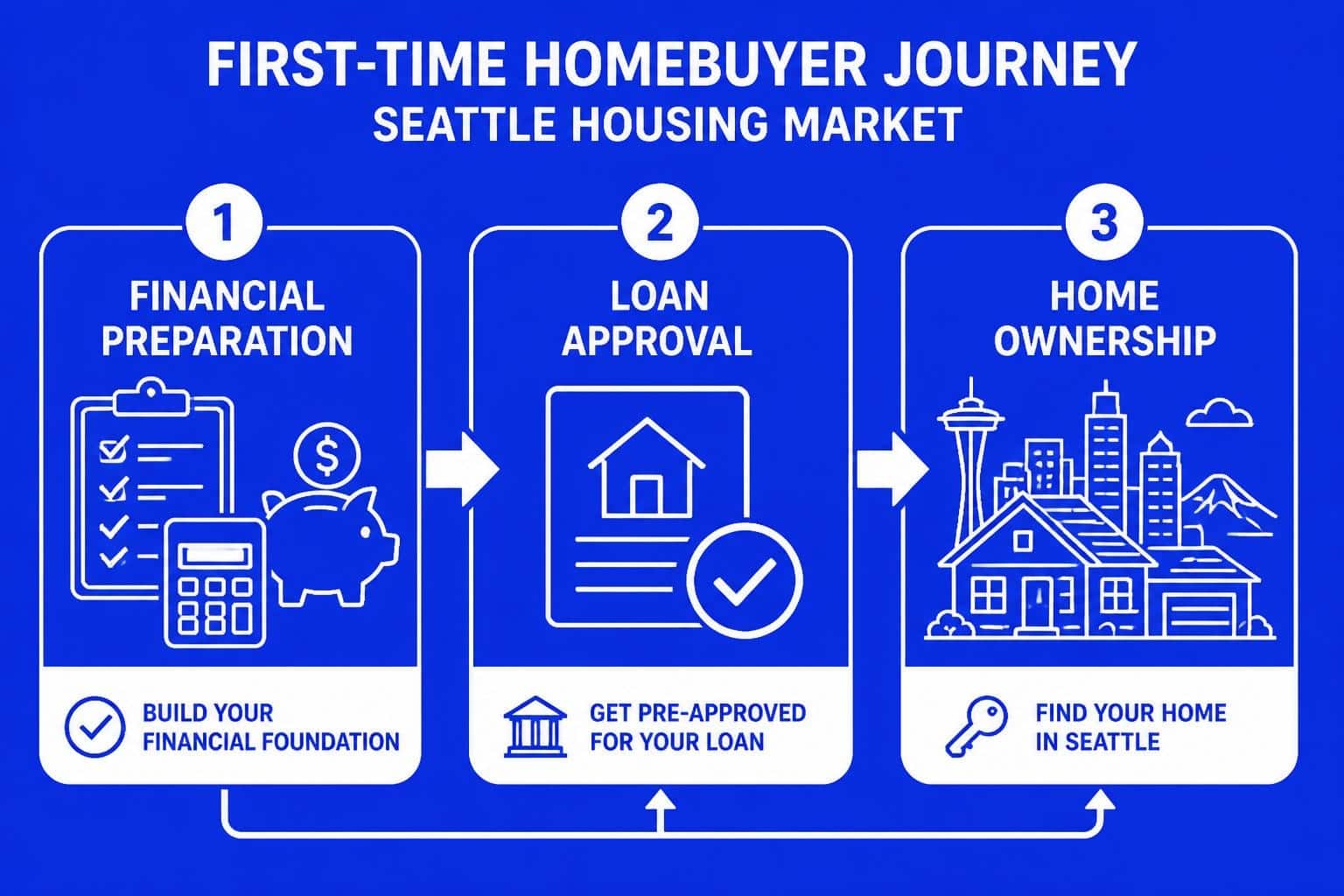

Timeline and Process for First-Time Buyers

Understanding the typical timeline for securing home loans first home buyers need enables realistic planning and reduces stress throughout the process. While each transaction varies, a general framework helps set expectations.

Pre-Purchase Preparation Phase (2-6 Months)

Serious buyers should begin preparation well before actively searching for properties. This phase includes:

- Credit report review and dispute filing for any errors

- Debt paydown strategy implementation for optimal DTI

- Down payment and reserve accumulation

- Pre-approval application and documentation submission

- First-time buyer education course completion (required for many assistance programs)

Programs tailored for Seattle first-time buyers often require educational components that take several hours to complete. Planning for these requirements prevents delays when you find the right property.

Active Search and Offer Phase (1-3 Months)

With pre-approval secured, the home search intensifies. Working with buyer's agents familiar with neighborhoods like Lake Forest Park, Lynnwood, or Everett helps identify properties matching your criteria and budget. Most first-time buyers view 10-20 homes before making offers, though competitive markets often require faster decisions.

The offer-to-acceptance period varies dramatically based on market conditions. In hot markets, sellers may review offers within 24-72 hours, requiring quick decision-making. Cooling markets provide more negotiation time and opportunity for inspections before finalizing offer terms.

Closing Phase (9-45 Days)

Once your offer is accepted, the closing timeline depends on contractual terms and lender efficiency. Traditional lenders average 30-45 days, while streamlined operations close in as few as 9-12 business days. This timeline includes:

- Property appraisal ordering and completion (7-14 days)

- Title search and commitment preparation (10-14 days)

- Final underwriting and clear-to-close status (varies)

- Final walkthrough and closing appointment scheduling

Understanding standard home loan approval timeframes helps you negotiate realistic closing dates that satisfy sellers while providing adequate processing time. Overcommitting to unrealistic timelines creates unnecessary stress and potential contract violations.

Common Mistakes First-Time Buyers Should Avoid

Learning from others' experiences helps home loans first home buyers navigate successfully without costly errors. These common mistakes derail transactions or create long-term financial stress:

Major pitfalls to avoid:

- Making large purchases or opening new credit accounts during the loan process

- Changing jobs or employment structure between pre-approval and closing

- Failing to maintain reserve requirements after down payment transfer

- Skipping professional inspections to save a few hundred dollars

- Draining emergency funds completely for a larger down payment

Job changes deserve special attention. Lenders verify employment immediately before closing, and changing employers-even for higher pay-can delay or derail approval. W-2 employees switching to contract positions face particularly challenging re-qualification because contract income typically requires two years of history.

New credit inquiries raise red flags during the loan process. That new furniture card or auto lease changes your debt profile and may require complete re-underwriting. Maintain status quo on all financial matters from application through closing, then make changes after recording.

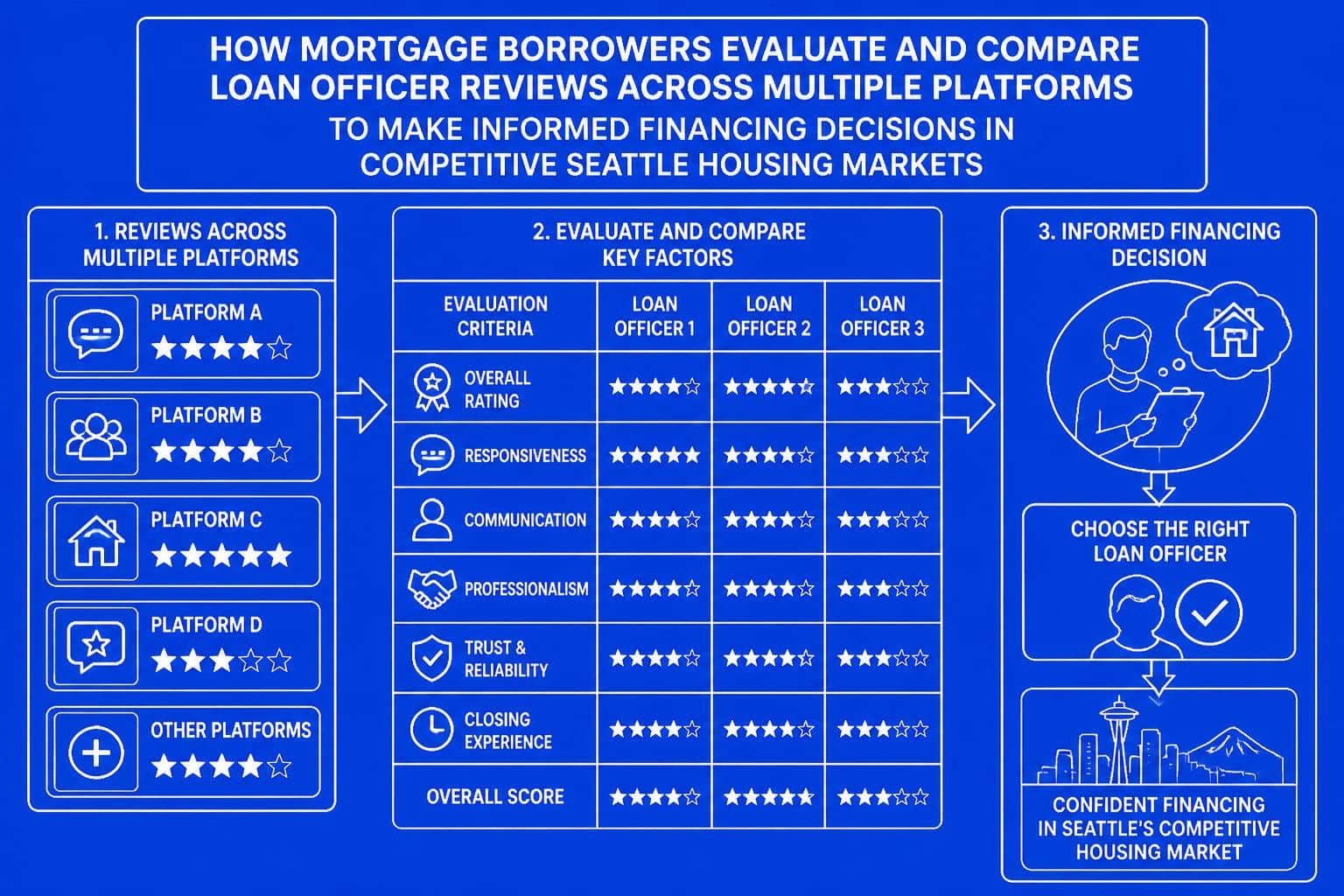

Choosing the Right Mortgage Broker in Seattle

The complexity of home loans first home buyers encounter demands professional guidance from experienced mortgage professionals who understand local market dynamics and lender requirements. Not all brokers provide equal value, particularly in specialized markets serving tech professionals with complex compensation structures.

Benefits of Local Expertise

Working with a Seattle mortgage broker provides advantages online lenders cannot match. Local professionals understand regional appraisal practices, title company nuances, and neighborhood-specific issues that affect financing. A broker familiar with Bellevue condo projects knows which buildings face warrantable status issues with certain lenders, preventing wasted time on properties you cannot finance.

Established relationships with local processors, underwriters, and closing agents enable faster problem resolution when issues arise. A trusted broker can escalate concerns through proper channels rather than navigating anonymous customer service systems. This access proves invaluable when timing matters for competitive offers or rate lock expirations.

Questions to Ask Potential Lenders

Interviewing multiple lenders ensures you select the best fit for your specific situation. Important questions include:

- How many first-time buyers have you helped in the past 12 months?

- What percentage of your business involves Seattle-area tech professionals?

- Can you provide recent client references in my price range?

- What is your average closing timeline, and what percentage close on schedule?

- How do you communicate throughout the process, and how quickly do you respond?

Review platforms like Google, Zillow, and Yelp provide insight into broker performance and client satisfaction. Look for consistent themes in feedback-communication quality, problem-solving ability, and reliability under pressure reveal more than simple star ratings.

Special Considerations for Tech Professionals

Seattle's concentration of major tech employers creates unique opportunities and challenges for home loans first home buyers working at companies like Amazon, Microsoft, Google, and others offering substantial stock compensation.

Qualifying RSUs and Stock Compensation

Restricted Stock Units represent significant income for many Seattle tech workers, but not all lenders qualify this compensation equally. Conservative approaches average two years of vesting and apply 70% of that average. Aggressive but defensible methods use 100% of expected vesting based on documented grant schedules.

For a Microsoft employee in Redmond with $100,000 annual base salary and $80,000 in annual RSU vesting, the difference between 70% and 100% treatment equals approximately $24,000 in qualifying income-translating to roughly $120,000 to $150,000 in additional purchasing power. This variance makes lender selection critical for maximizing buying power.

Stock-heavy compensation packages require specialized documentation including:

- Vesting schedules from equity management platforms

- Historical sale proceeds demonstrating vesting consistency

- Tax returns showing supplemental income reporting

- Employer verification confirming future vesting amounts

Jumbo Loan Considerations

Home prices in Bellevue, Kirkland, and prime Seattle neighborhoods frequently exceed conforming loan limits of $806,500 in 2026. Jumbo loan qualification demands stronger financial profiles with higher credit scores, lower debt ratios, and larger reserves.

Typical jumbo requirements include:

| Requirement | Conforming | Jumbo |

|---|---|---|

| Minimum Credit Score | 620 | 700-720 |

| Maximum DTI | 50% | 43-45% |

| Reserve Requirements | 2 months | 6-12 months |

| Documentation | Standard | Enhanced |

Despite stricter requirements, jumbo rates often compete favorably with conforming rates for well-qualified borrowers. The key involves working with lenders who actively price jumbo products competitively rather than treating them as specialty situations with premium pricing.

Successfully navigating home loans first home buyers need in Seattle's competitive market requires strategic preparation, comprehensive knowledge, and experienced professional guidance. Whether you're a tech professional maximizing stock compensation or a first-time buyer exploring assistance programs, understanding your options empowers confident decisions. Keith Akada brings 25+ years of expertise helping Seattle-area buyers transform homeownership dreams into reality, with 750+ five-star reviews reflecting his commitment to education, transparency, and reliable execution. From first-time buyers in Lynnwood to tech professionals purchasing in Bellevue, Mortgage Reel provides the strategic guidance and responsive service you need to succeed in 2026's housing market.