Navigating the Seattle housing market as a first-time buyer presents both exciting opportunities and complex financial decisions. Choosing the right mortgage lender first time buyer partnership determines not just whether you qualify for a loan, but how smoothly your path to homeownership unfolds. In competitive markets like Seattle, Bellevue, and Redmond, the difference between a knowledgeable local lender and a transactional bank experience can mean winning your dream home or losing out to better-prepared buyers. Understanding what separates exceptional mortgage guidance from basic loan processing helps you build the foundation for confident homebuying decisions.

Understanding Mortgage Lender Options for First-Time Buyers

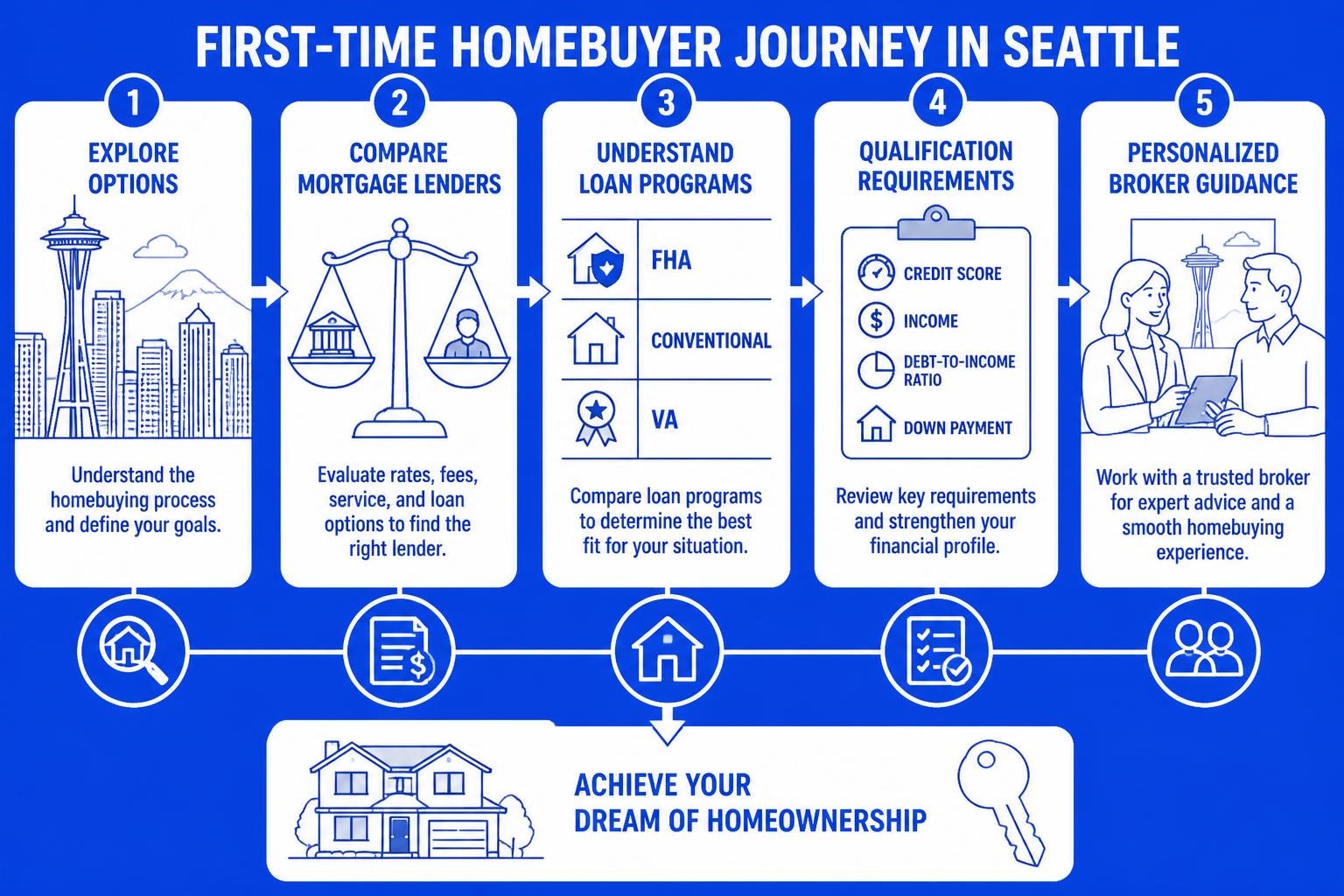

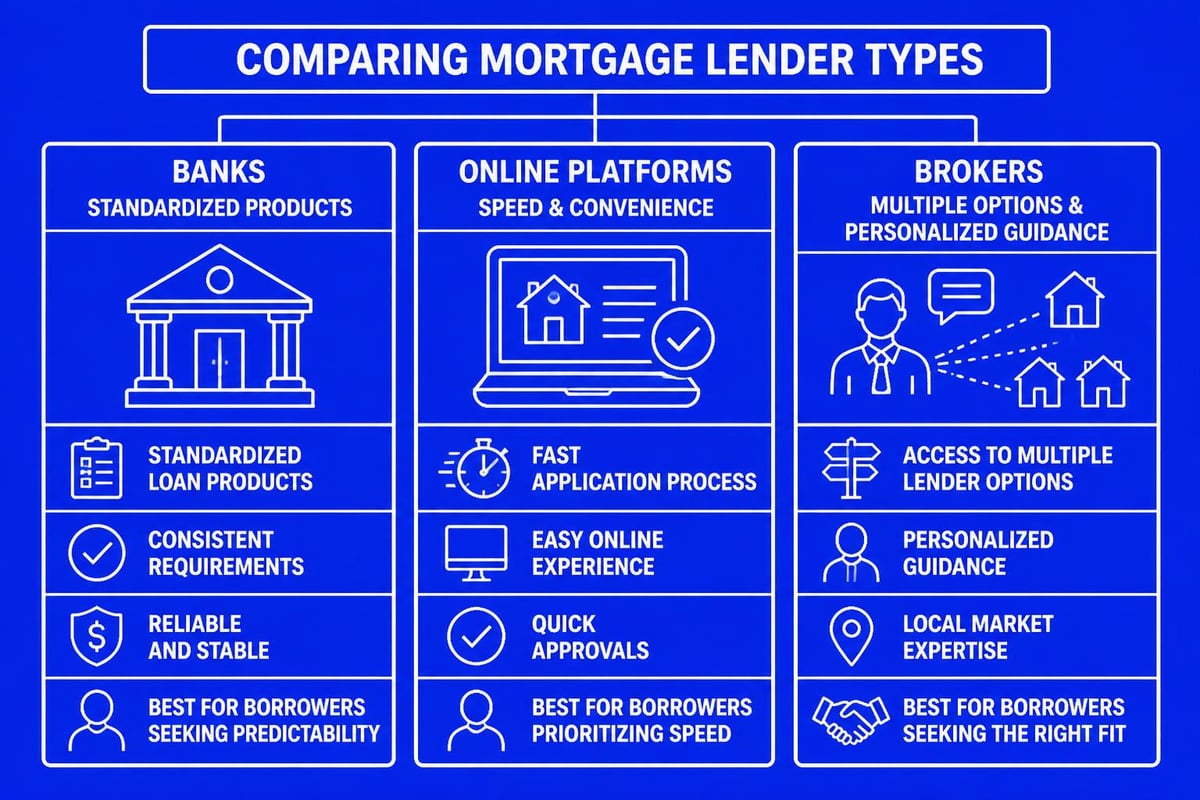

The mortgage landscape offers multiple paths to homeownership, and not all lenders provide equal access to every option. First-time buyers typically work with three main categories of lenders: direct banks, online lenders, and mortgage brokers.

Direct Banks and Credit Unions

Traditional banks offer in-house mortgage products with predictable processes and established reputations. These institutions generally provide competitive rates for borrowers with strong credit profiles and straightforward income documentation. However, their rigid underwriting guidelines often limit flexibility for tech professionals with stock compensation or buyers with non-traditional income sources.

Credit unions typically offer member benefits including reduced fees and personalized service. For first-time buyers in Seattle neighborhoods like Lake Forest Park or Shoreline, local credit unions understand regional market dynamics but may have limited product availability compared to larger mortgage networks.

Online Mortgage Platforms

Digital-first lenders streamline applications through technology, often advertising faster approvals and lower overhead costs. While convenient for simple transactions, these platforms typically lack the personalized guidance crucial when navigating complex scenarios like qualifying RSU income for mortgage applications or coordinating competitive offer strategies in heated markets.

Mortgage Brokers: Maximum Flexibility

Brokers operate differently than captive lenders by accessing multiple wholesale lending partners. This structure enables comparison shopping across dozens of loan programs simultaneously, identifying the optimal combination of rates, terms, and qualification requirements for each buyer's unique situation.

For first-time buyers, this flexibility proves particularly valuable when exploring home loans in Washington for first-time buyers with varying down payment capabilities or credit profiles.

Essential Loan Programs for First-Time Homebuyers

Understanding available mortgage products represents the first step toward informed lender selection. Each program serves different financial profiles and homeownership goals.

| Loan Type | Minimum Down Payment | Credit Score | Key Benefits |

|---|---|---|---|

| Conventional 97 | 3% | 620+ | Low down payment, no upfront MIP |

| FHA | 3.5% | 580+ | Flexible qualification, higher DTI allowed |

| VA | 0% | Varies | No down payment, no PMI (veterans only) |

| USDA | 0% | 640+ | Rural/suburban properties, income limits apply |

Conventional Loans

Conventional home loans remain the most popular choice for first-time buyers with stable employment and solid credit. The 97% LTV option requires just 3% down, making homeownership accessible without years of aggressive saving. Private mortgage insurance (PMI) applies when down payments fall below 20%, but borrowers can request PMI removal once equity reaches 20%.

Seattle-area buyers employed by Amazon, Microsoft, or Google frequently leverage conventional financing to qualify stock compensation income, maximizing purchasing power for competitive neighborhoods in Bellevue and Redmond.

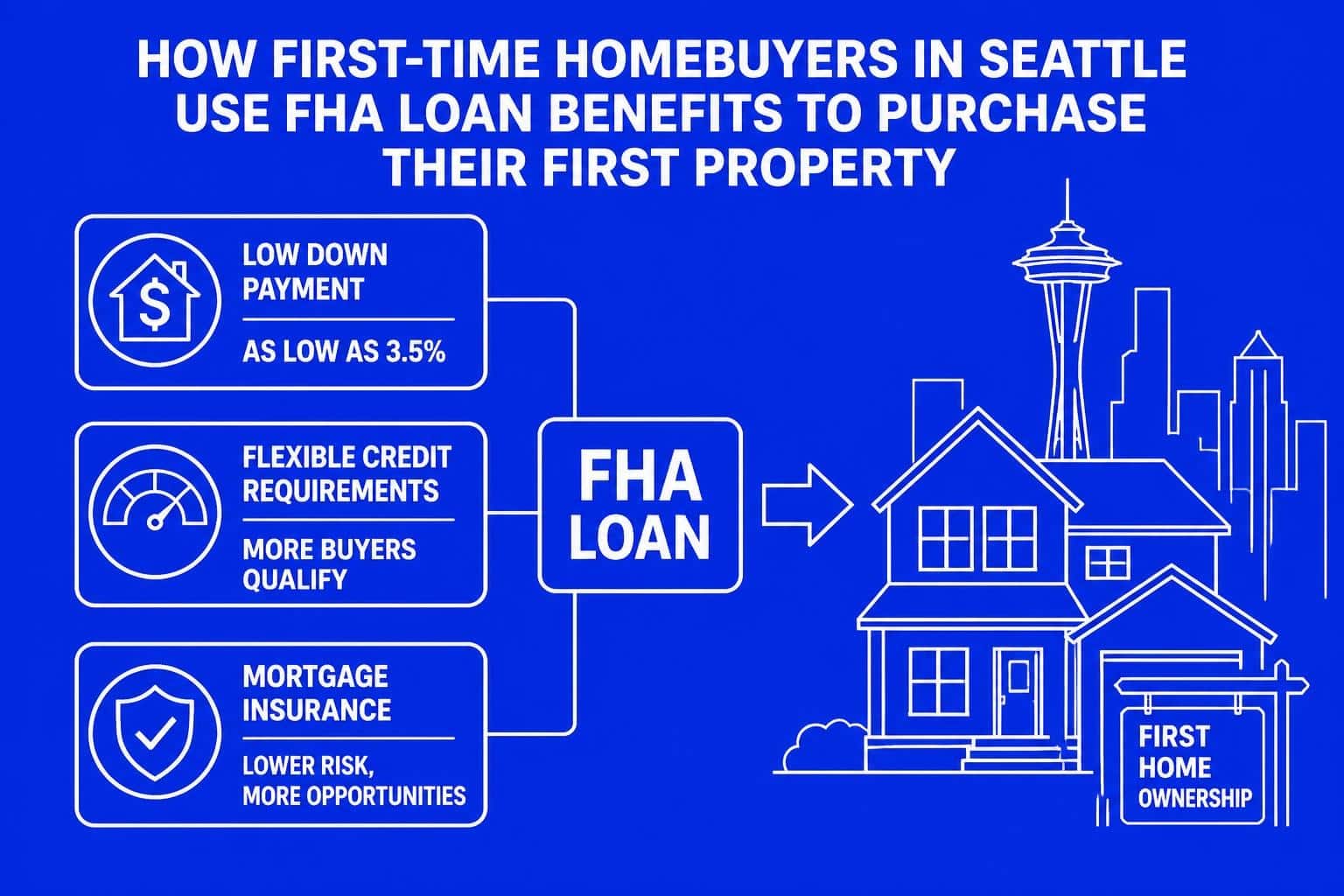

FHA Loans: Accessibility with Flexibility

FHA home loans accommodate buyers with credit scores as low as 580 and debt-to-income ratios up to 50% under certain conditions. According to programs designed for first-time homebuyers, FHA financing provides crucial access for buyers rebuilding credit or carrying student loan debt.

The trade-off involves mandatory mortgage insurance premiums throughout the loan term on most FHA mortgages originated after 2013. First-time buyers should calculate total payment obligations including this ongoing premium when comparing programs.

VA and USDA: Zero-Down Possibilities

VA veterans loans eliminate down payment requirements entirely for eligible service members and veterans. With no PMI requirement regardless of down payment amount, VA financing offers exceptional long-term value. Competitive rates and flexible underwriting make VA loans powerful tools for military-connected buyers.

USDA loans similarly require no down payment for qualifying rural and suburban properties. While Seattle proper doesn't qualify, areas like Mill Creek and Everett may meet USDA eligibility requirements depending on specific location.

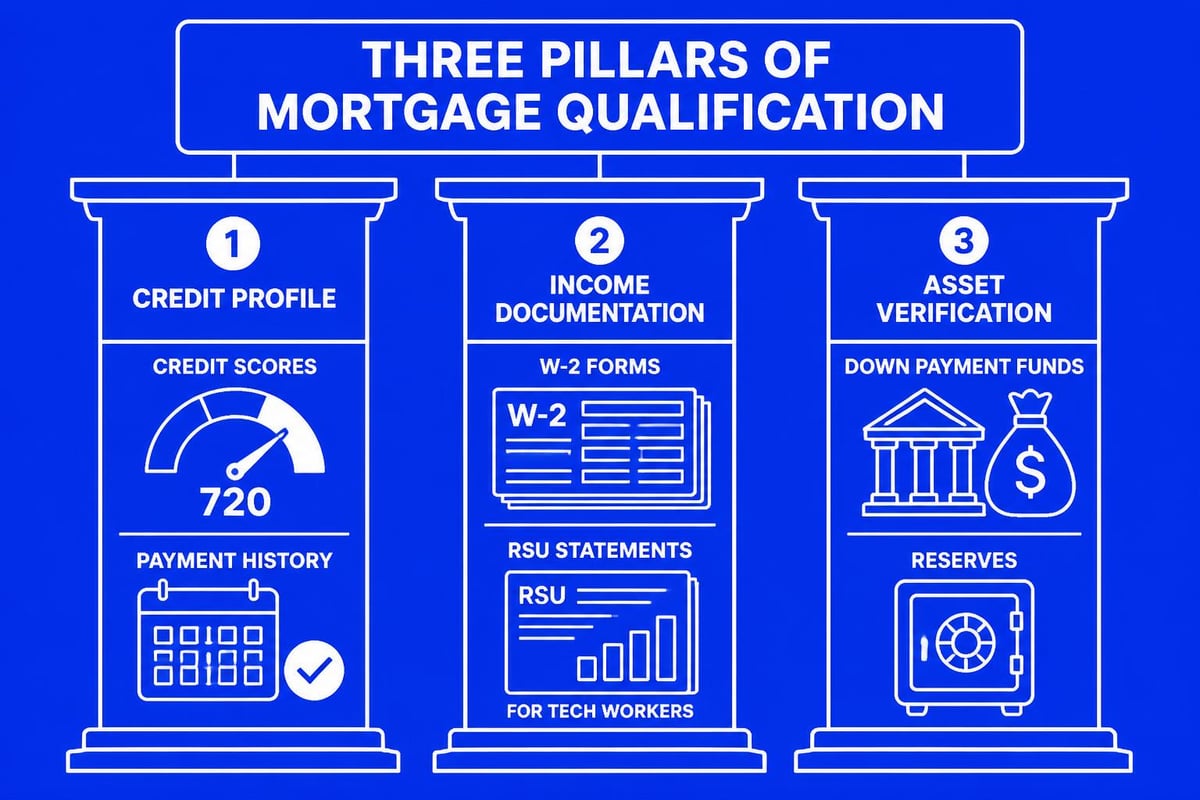

Qualification Requirements and Preparation Strategies

Successful mortgage lender first time buyer relationships begin with clear qualification understanding. Lenders evaluate three primary factors when assessing loan applications.

Credit Profile Optimization

Minimum credit scores vary by program, but higher scores unlock better rates and terms. First-time buyers should review credit reports at least six months before home shopping, addressing any errors or negative items systematically.

Credit improvement strategies include:

- Reducing credit card balances below 30% of limits

- Avoiding new credit inquiries during the mortgage process

- Maintaining consistent payment histories across all accounts

- Requesting goodwill adjustments for isolated late payments

- Becoming an authorized user on established accounts

For Seattle buyers wondering about credit score requirements to buy a home, understanding how scores affect rate pricing helps prioritize credit optimization efforts.

Income Documentation and Employment Verification

Lenders verify income stability through pay stubs, tax returns, and employment verification. Tech professionals with complex compensation packages require lenders experienced in documenting restricted stock units (RSUs), bonuses, and equity compensation.

Most programs require two-year employment history, though recent graduates may qualify with strong credit and reasonable debt-to-income ratios. Self-employed buyers need two years of tax returns demonstrating consistent income, with lenders averaging the two-year period for qualification purposes.

Down Payment Sources and Reserves

Beyond the minimum down payment, lenders assess reserve requirements-liquid assets remaining after closing. Reserve expectations vary by loan type, down payment amount, and property characteristics.

Acceptable down payment sources include:

- Personal savings and checking accounts

- Retirement account withdrawals (with documentation)

- Gift funds from family members (with gift letters)

- Down payment assistance programs

- Employer assistance programs

Understanding loan down payment requirements in Washington State helps first-time buyers set realistic savings goals aligned with their timeline.

Working With Mortgage Lenders: Process and Timeline

The mortgage application journey unfolds through distinct phases, each requiring specific documentation and decision points.

Pre-Approval: Your Competitive Advantage

Pre-approval establishes buying power before house hunting begins. Comprehensive pre-approval involves full credit review, income verification, and asset documentation-providing sellers confidence that your offer includes solid financing.

In competitive Seattle neighborhoods, pre-approval from a respected local lender carries significant weight. Listing agents recognize lenders with strong track records, favoring offers backed by reliable financing over potentially problematic approvals from unknown sources.

According to Bankrate’s first-time homebuyer guide, pre-approval strengthens negotiating position and accelerates closing timelines once offers are accepted.

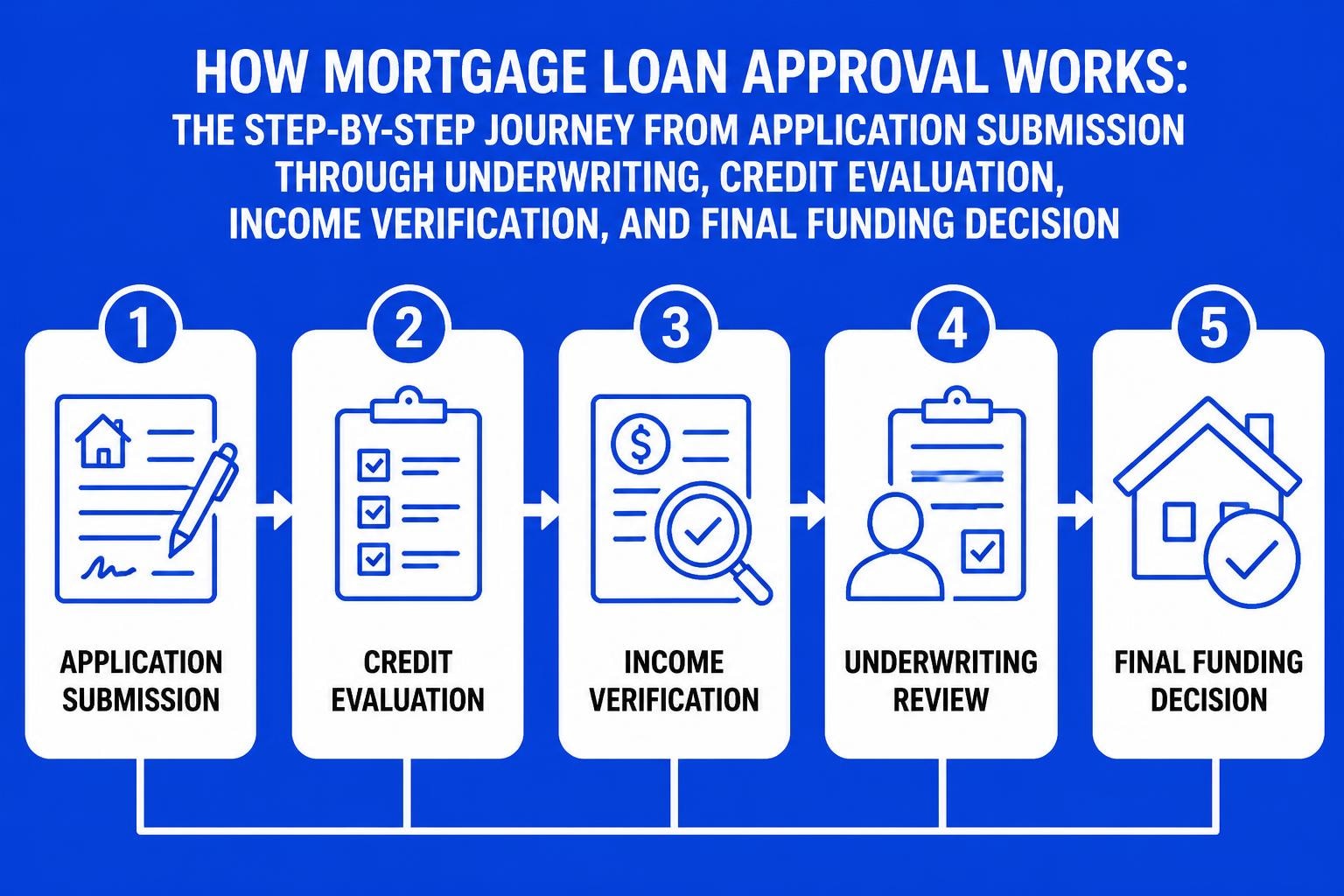

Application Through Underwriting

Once you identify a property and reach mutual acceptance, the formal application process begins. Borrowers submit complete financial documentation while the lender orders appraisals, title reports, and verification documents.

Key process milestones include:

- Initial disclosure delivery (within three business days)

- Appraisal completion (typically 7-14 days)

- Underwriting review (3-7 days for initial decision)

- Conditional approval with outstanding requirements

- Final clear-to-close authorization

Experienced lenders anticipate potential underwriting concerns, proactively addressing documentation gaps before they delay closing. This foresight proves particularly valuable when qualifying jumbo loans for Seattle homebuyers with complex financial profiles.

Closing Timeline Expectations

Standard closing timelines range from 30 to 45 days, though accelerated processes can compress this window. Understanding how long it takes to get a mortgage in Seattle helps first-time buyers set realistic expectations with sellers.

Advanced underwriting capabilities enable some lenders to close transactions in as few as 9 business days when documentation is complete and appraisals are expedited. This speed becomes critical in competitive multiple-offer scenarios where quick closing attracts seller preference.

Evaluating Lender Capabilities and Service Quality

Not all mortgage lender first time buyer experiences deliver equal value. Discerning buyers assess multiple dimensions beyond advertised rates when selecting lending partners.

Rate Transparency and Cost Comparison

Interest rates represent just one component of total borrowing costs. Comparing loan estimates across multiple lenders reveals the complete picture, including origination fees, discount points, and third-party charges.

Critical comparison points include:

| Cost Category | What to Compare | Why It Matters |

|---|---|---|

| Interest Rate | APR vs. note rate | APR includes fees, showing true cost |

| Origination Fees | Points and lender charges | Direct cost for loan processing |

| Rate Lock Period | Duration and extension costs | Protection against rising rates |

| Third-Party Fees | Appraisal, title, escrow | Costs beyond lender control |

First-time buyers should request loan estimates from multiple sources, comparing identical loan scenarios to ensure apples-to-apples evaluation. Understanding the difference between mortgage brokers and banks clarifies how compensation structures affect rate offerings.

Communication and Accessibility

Responsive communication separates exceptional lender experiences from frustrating ones. First-time buyers benefit from lenders who explain complex concepts clearly, answer questions promptly, and provide proactive updates throughout the process.

Consider communication preferences when selecting a lender. Some buyers prefer digital-first interactions with minimal phone contact, while others value face-to-face consultations and regular check-ins. Finding a lender whose style matches your preferences enhances the overall experience.

Local Market Expertise

Lenders familiar with Seattle-area markets understand neighborhood dynamics, property value trends, and regional appraisal considerations. This local knowledge proves invaluable when evaluating properties in diverse communities from urban Capitol Hill to suburban Lynnwood.

According to guidance on why to choose a local lender in Seattle, regional expertise facilitates smoother transactions through established relationships with appraisers, title companies, and real estate professionals.

Special Considerations for Seattle-Area First-Time Buyers

The Greater Seattle housing market presents unique opportunities and challenges requiring specialized lender guidance.

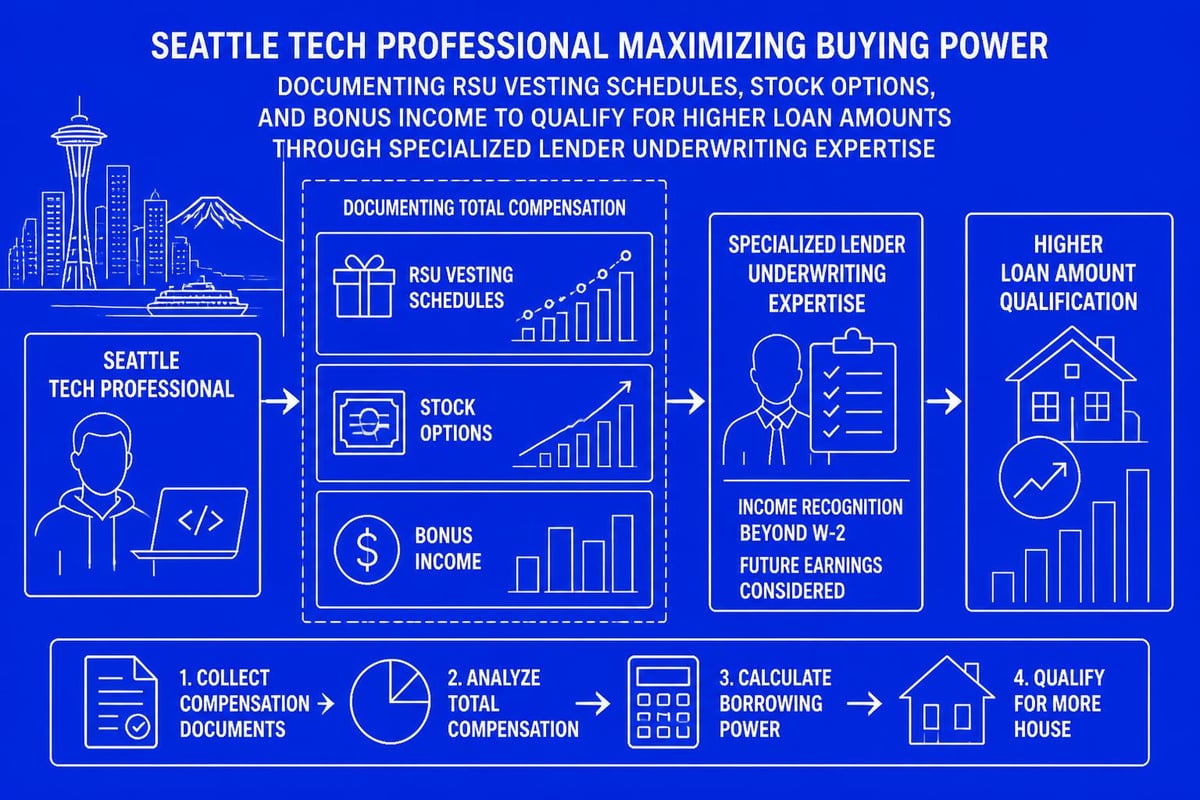

Tech Compensation Qualification

Seattle's concentration of technology employers creates specific mortgage scenarios involving equity compensation. Restricted stock units, employee stock purchase plans, and performance bonuses represent significant income sources that require proper documentation and lender expertise to qualify.

Conservative lenders may exclude or heavily discount variable compensation, while experienced brokers understand how to document and underwrite these income streams effectively. For buyers at companies like Amazon or Microsoft, finding a lender skilled in RSU income qualification maximizes purchasing power.

Jumbo Loan Navigation

Seattle's elevated home prices frequently push buyers into jumbo loan territory-mortgages exceeding conforming loan limits of $806,500 in 2026. Jumbo home loan qualification typically requires higher credit scores, larger down payments, and more substantial reserves than conforming loans.

However, competitive jumbo programs exist offering down payments as low as 10% for qualified buyers. Understanding 10% down jumbo home loan options helps first-time buyers access Seattle's housing market without delaying homeownership for years of additional saving.

Competitive Offer Strategies

Multiple-offer scenarios remain common across Seattle neighborhoods. Strong financing terms enhance offer competitiveness beyond price alone. Elements like larger earnest money deposits, minimal contingencies, and accelerated closing timelines appeal to sellers evaluating multiple bids.

Working with a lender capable of quick closes and reliable execution gives buyers strategic advantages. As detailed in resources about how to win bidding wars in Seattle, financing certainty often influences seller decisions as much as offer price.

Down Payment Assistance and First-Time Buyer Programs

Washington State and local municipalities offer various assistance programs reducing upfront costs for qualified first-time buyers. These programs combine with standard mortgage products to enhance affordability.

State and Local Assistance Programs

Washington State Housing Finance Commission administers down payment assistance programs providing grants or second mortgages to eligible buyers. Income limits and purchase price restrictions apply, but qualifying buyers can access thousands in down payment support.

King County and surrounding jurisdictions offer additional local programs. Exploring first-time buyer programs in Lake Forest Park and similar communities reveals location-specific opportunities for assistance.

Employer Assistance Benefits

Many Seattle-area employers provide homebuyer assistance as employee benefits. These programs may offer forgivable loans, matching contributions, or outright grants toward down payments and closing costs. Tech companies particularly embrace these benefits as retention and recruitment tools.

First-time buyers should investigate employer programs early in the planning process, understanding vesting requirements and qualified use restrictions. Combining employer assistance with conventional or FHA financing can substantially reduce out-of-pocket expenses.

Common First-Time Buyer Mistakes to Avoid

Learning from common pitfalls helps first-time buyers navigate the mortgage process more successfully.

Frequent mistakes include:

- Shopping for homes before securing pre-approval, wasting time viewing properties beyond realistic budgets

- Overlooking total monthly costs beyond principal and interest, including taxes, insurance, and maintenance

- Making major financial changes during the mortgage process, such as changing jobs or opening new credit

- Skipping professional inspections to save costs, potentially inheriting expensive repair obligations

- Choosing lenders based solely on initial rate quotes without evaluating service quality and reliability

- Depleting all savings for down payment, leaving no emergency reserves for unexpected expenses

According to Chase Bank’s tips for first-time homebuyers, understanding the complete picture of homeownership costs prevents buyer's remorse and financial stress.

Building Your First-Time Buyer Team

Successful homebuying involves collaboration among multiple professionals, each contributing specialized expertise.

Selecting a Real Estate Agent

Experienced buyer's agents guide property search, negotiate offers, and coordinate closing logistics. First-time buyers benefit from agents specializing in their target neighborhoods who understand local market conditions and seller preferences.

Agent selection should prioritize communication style compatibility, market expertise, and proven negotiation skills. Interview multiple agents before committing, assessing their understanding of your specific needs and goals.

Additional Team Members

Beyond your mortgage lender first time buyer relationship and real estate agent, consider engaging:

- Home inspectors providing objective property condition assessments

- Real estate attorneys reviewing contracts in complex transactions

- Insurance agents securing appropriate homeowners coverage

- Financial advisors evaluating homeownership within broader financial plans

- Tax professionals understanding deduction implications and strategies

Coordinating this team effectively requires clear communication and realistic timeline expectations. Your mortgage lender and real estate agent typically serve as primary coordinators, facilitating connections among service providers.

Long-Term Mortgage Strategy Considerations

First-time homebuying decisions extend beyond initial purchase, influencing financial flexibility for years to come.

Loan Term Selection

While 30-year fixed mortgages dominate first-time buyer choices, alternative terms may better serve specific situations. Fifteen-year mortgages build equity faster through higher payments and lower interest rates, while adjustable-rate mortgages (ARMs) can reduce initial costs for buyers expecting to relocate within several years.

Evaluating how different mortgage types align with personal timelines and financial goals helps optimize long-term outcomes rather than simply minimizing initial monthly payments.

Future Refinancing Opportunities

Market conditions and personal circumstances evolve over time, creating potential refinancing opportunities. Understanding when refinancing makes sense-whether to reduce rates, eliminate PMI, or access equity-positions homeowners to capitalize on favorable changes.

Resources explaining how to lower your mortgage payment through strategic refinancing help homeowners maximize long-term savings.

Equity Building and Appreciation

Real estate represents both housing and investment, with equity accumulation creating financial options over time. First-time buyers establish wealth-building foundations through homeownership, converting monthly rent payments into equity growth.

Seattle's strong historical appreciation enhances this wealth-building potential, though buyers should maintain realistic expectations about future market performance and avoid overextending based on speculation.

Resources and Educational Tools

Informed decisions require quality information from credible sources. First-time buyers should leverage educational resources throughout the homebuying journey.

Homebuyer.com’s Mortgage 101 guide provides comprehensive explanations of mortgage fundamentals, while Opendoor’s first-time home buyer mortgage guide offers current program details and qualification requirements.

For Seattle-specific guidance, exploring comprehensive resources about how to buy a home with expert guidance provides localized insights beyond generic national information.

Additional valuable perspectives include Fidelity’s step-by-step homebuying guide covering financial planning aspects and Credit.org’s mortgage type comparison helping buyers understand program differences.

Finding the right mortgage lender first time buyer partnership transforms a potentially overwhelming process into a confident journey toward homeownership. The combination of comprehensive loan program knowledge, local market expertise, and personalized guidance ensures you make informed decisions aligned with both immediate needs and long-term financial goals. Whether you're a tech professional in Redmond leveraging stock compensation or a first-time buyer in Shoreline exploring down payment assistance programs, experienced guidance makes all the difference. Keith Akada brings 25+ years of mortgage expertise to first-time buyers across Seattle, Bellevue, and surrounding communities, with 750+ five-star reviews reflecting his commitment to education, transparency, and reliable execution. Connect with Mortgage Reel to start your homebuying journey with a trusted local partner who prioritizes your success.