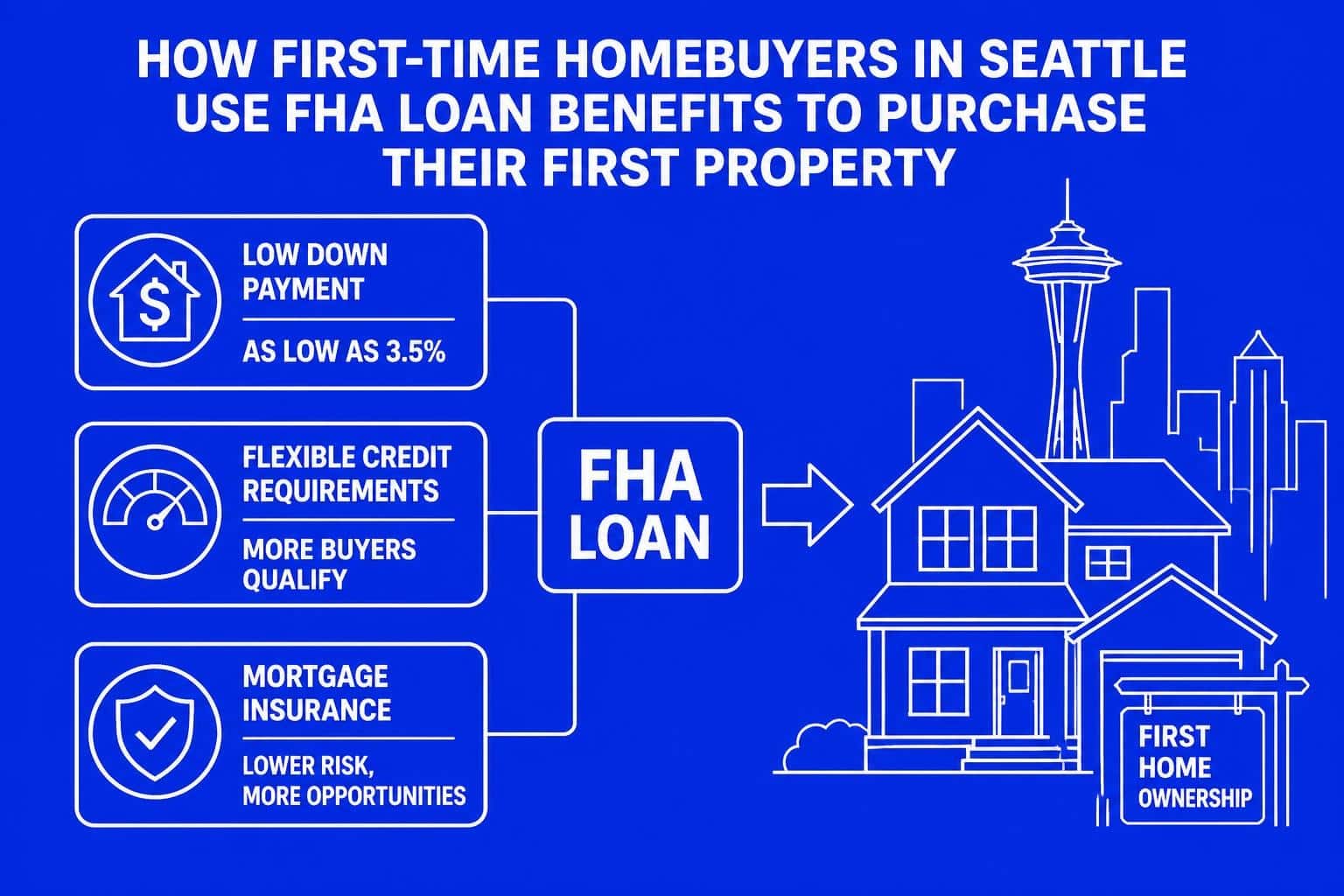

Breaking into Seattle's competitive housing market feels overwhelming for many first-time buyers, especially when saving 20% down seems impossible. A first home buyer FHA loan offers an accessible path to homeownership with just 3.5% down, making it one of the most popular financing options for buyers entering markets like Seattle, Bellevue, Redmond, and Kirkland. Understanding how FHA loans work, what they require, and whether they align with your financial situation can transform your home buying strategy from uncertain to actionable.

What Makes FHA Loans Ideal for First-Time Buyers

Federal Housing Administration (FHA) loans were specifically designed to help Americans achieve homeownership when conventional financing presents barriers. For first-time buyers in Seattle and surrounding areas like Shoreline and Lake Forest Park, these government-backed mortgages reduce the capital required upfront while accommodating various credit profiles.

Lower Down Payment Requirements

The 3.5% minimum down payment represents the most significant advantage for buyers who haven't accumulated substantial savings. In Seattle's median home price environment, this difference becomes substantial:

- Conventional loan with 5% down on a $650,000 home: $32,500 required

- First home buyer FHA loan with 3.5% down: $22,750 required

- Immediate savings: $9,750 that can cover closing costs or reserves

This flexibility proves particularly valuable for tech professionals in Bellevue or Redmond who may have high incomes but limited liquid assets due to equity compensation structures. Those interested in conventional financing options with lower down payments can compare both programs to determine optimal timing.

Flexible Credit Score Standards

FHA loans accommodate borrowers with credit scores as low as 580 for the minimum 3.5% down payment. Buyers with scores between 500-579 may still qualify with 10% down, though this scenario is less common. According to detailed FHA loan requirements for 2026, these guidelines remain more forgiving than conventional programs requiring 620+ scores.

Credit flexibility matters significantly in real-world scenarios:

- Recent college graduates with limited credit history

- Professionals recovering from past financial setbacks

- Self-employed individuals building business credit

- First-time buyers who prioritized student loan repayment over credit building

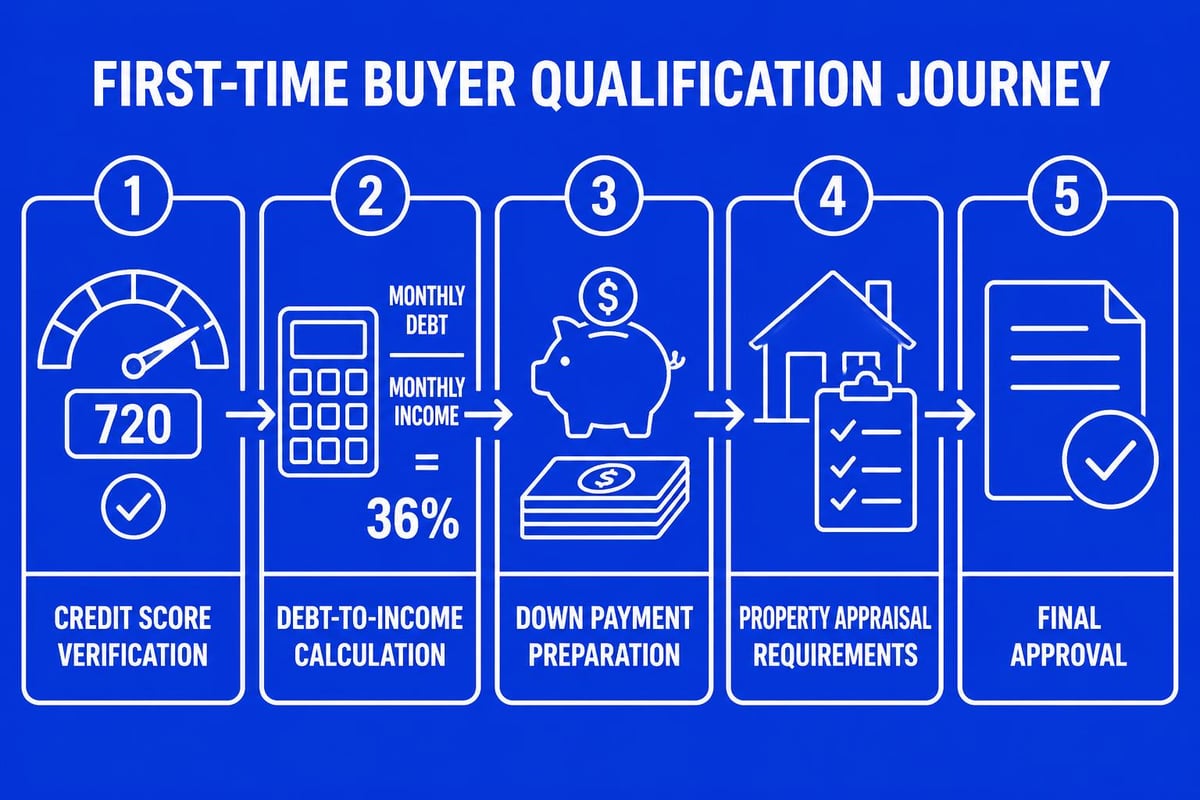

Understanding FHA Loan Requirements and Qualifications

Meeting FHA eligibility extends beyond just credit scores and down payments. The Federal Housing Administration establishes comprehensive standards ensuring both borrower capacity and property quality.

Income and Employment Verification

Lenders must verify stable, reliable income through documentation spanning typically two years. For W-2 employees at Amazon, Microsoft, or Google headquarters in Seattle and Bellevue, this process is straightforward with pay stubs, W-2s, and employment verification.

Qualifying different income types requires specific strategies:

- Base salary: Most straightforward qualification using recent pay stubs and tax returns

- Bonus income: Requires two-year history and continuation likelihood

- RSUs and stock compensation: Needs specialized underwriting for vesting schedules

- Commission income: Averaged over 24 months with stability assessment

- Self-employment: Two years of tax returns with profit/loss statements

The debt-to-income (DTI) ratio typically cannot exceed 43%, though compensating factors may allow flexibility up to 50%. This calculation includes your proposed mortgage payment plus all monthly debt obligations divided by gross monthly income.

Property Standards and Appraisal Requirements

FHA loans require properties to meet minimum property standards (MPS) ensuring safety, security, and structural soundness. The FHA appraisal assesses both market value and property condition, occasionally presenting challenges in Seattle's older housing stock.

| Requirement Category | FHA Standard | Common Seattle Issues |

|---|---|---|

| Foundation | No significant cracks or settling | Older homes in Capitol Hill, Fremont |

| Roof | Minimum 2 years remaining life | 1920s-1940s bungalows needing updates |

| Electrical | Adequate service, proper grounding | Knob-and-tube wiring in historic districts |

| Plumbing | Functional, no major leaks | Galvanized pipe replacement needs |

| Safety | Handrails, egress windows, smoke detectors | Basement conversions without permits |

Buyers pursuing homes in established Seattle neighborhoods like Ballard, Wallingford, or Lake Forest Park should budget for potential repair negotiations or seller concessions addressing FHA appraisal conditions.

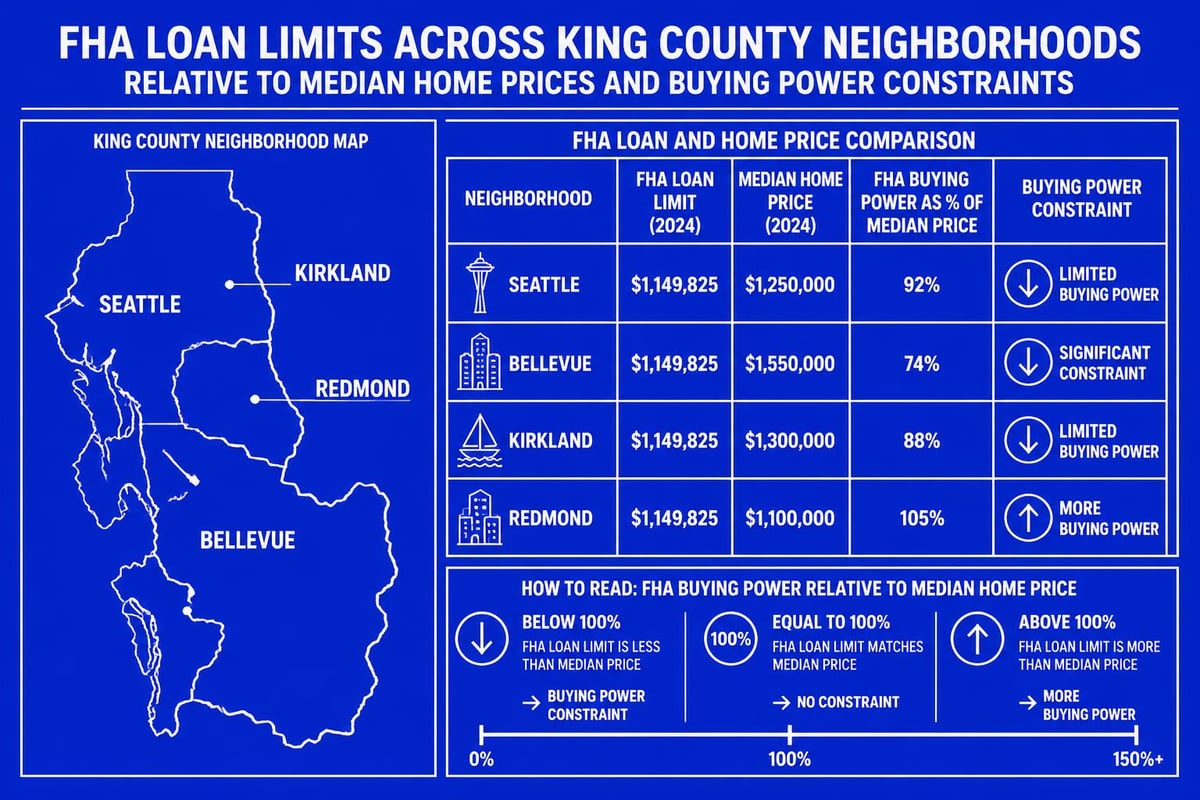

FHA Loan Limits in Seattle and King County

The Department of Housing and Urban Development (HUD) sets maximum loan amounts annually based on median home prices by county. For 2026, King County maintains higher limits reflecting Seattle's elevated housing costs.

2026 FHA loan limits for the Seattle area:

- Single-family homes: $498,257

- Duplexes: $637,950

- Triplexes: $771,125

- Four-unit properties: $958,350

These limits create a ceiling for first home buyer FHA loan amounts, which impacts purchasing power in Seattle's competitive market where median single-family prices exceed $800,000 in many neighborhoods. Buyers targeting homes above FHA limits should explore conventional financing or jumbo loan programs better suited to higher price points.

For condominiums, additional FHA approval requirements apply to the entire complex, not just individual units. Buyers in Bellevue, Redmond, or downtown Seattle high-rises must verify FHA approval status before proceeding, as non-approved buildings disqualify FHA financing regardless of unit price.

Mortgage Insurance Costs and Long-Term Implications

FHA loans require two types of mortgage insurance protecting lenders against default risk. Understanding these costs is essential for accurate monthly payment calculations and long-term financial planning.

Upfront Mortgage Insurance Premium (UFMIP)

The UFMIP equals 1.75% of the base loan amount, typically financed into the mortgage rather than paid at closing. On a $475,000 loan, this represents $8,312.50 added to your principal balance, slightly increasing your monthly payment and total interest paid over the loan term.

Annual Mortgage Insurance Premium (MIP)

Annual MIP varies based on loan amount, loan-to-value ratio, and loan term:

| Base Loan Amount | LTV Ratio | 30-Year Term MIP | 15-Year Term MIP |

|---|---|---|---|

| ? $726,200 | ? 95% | 0.55% annually | 0.45% annually |

| ? $726,200 | > 95% | 0.80% annually | 0.70% annually |

| > $726,200 | ? 95% | 0.75% annually | 0.70% annually |

| > $726,200 | > 95% | 1.00% annually | 0.95% annually |

For most first home buyer FHA loan scenarios with 3.5% down, expect 0.80% annual MIP. On a $475,000 loan, this equals $3,800 annually or approximately $317 monthly.

The critical distinction from conventional PMI: FHA mortgage insurance persists for the loan's entire term when putting less than 10% down. This permanent cost factor makes refinancing into conventional financing attractive once you've built 20% equity and improved your credit profile. Working with an experienced Seattle mortgage broker helps time this transition optimally.

Comparing FHA Loans to Other First-Time Buyer Programs

Seattle-area buyers should evaluate multiple financing options rather than defaulting to FHA without comparison. Each program offers distinct advantages depending on individual circumstances, and various loan types for first-time buyers present different trade-offs.

FHA vs. Conventional Loans

FHA advantages:

- Lower down payment (3.5% vs. 3-5% conventional)

- More flexible credit requirements (580 vs. 620+)

- Higher DTI tolerance

- Easier qualification after financial difficulties

Conventional advantages:

- No upfront mortgage insurance premium

- PMI removable at 20% equity (vs. permanent MIP)

- Higher loan limits for expensive Seattle properties

- Faster closing timelines

- More competitive in multiple-offer situations

For buyers with strong credit (720+) and stable employment, conventional financing often provides better long-term value despite similar down payment requirements. The advantages and disadvantages of FHA loans become clearer through personalized cost analysis comparing total payments over expected ownership duration.

VA Loans for Eligible Veterans

Military veterans, active-duty service members, and qualifying spouses should prioritize VA loans over FHA options. VA financing offers zero down payment, no mortgage insurance, competitive interest rates, and limited closing costs-advantages that significantly outperform FHA benefits. Veterans in Seattle, Everett, or Lynnwood can explore VA loan benefits through specialized lenders.

Washington State First-Time Buyer Programs

The Washington State Housing Finance Commission offers down payment assistance and favorable interest rates through the House Key program, which can pair with FHA financing for even greater accessibility. These programs target moderate-income buyers in King County and surrounding areas, potentially covering 3-5% of the purchase price.

Strategic Considerations for Seattle-Area Buyers

Successfully leveraging a first home buyer FHA loan in competitive Seattle neighborhoods requires understanding local market dynamics and positioning yourself advantageously.

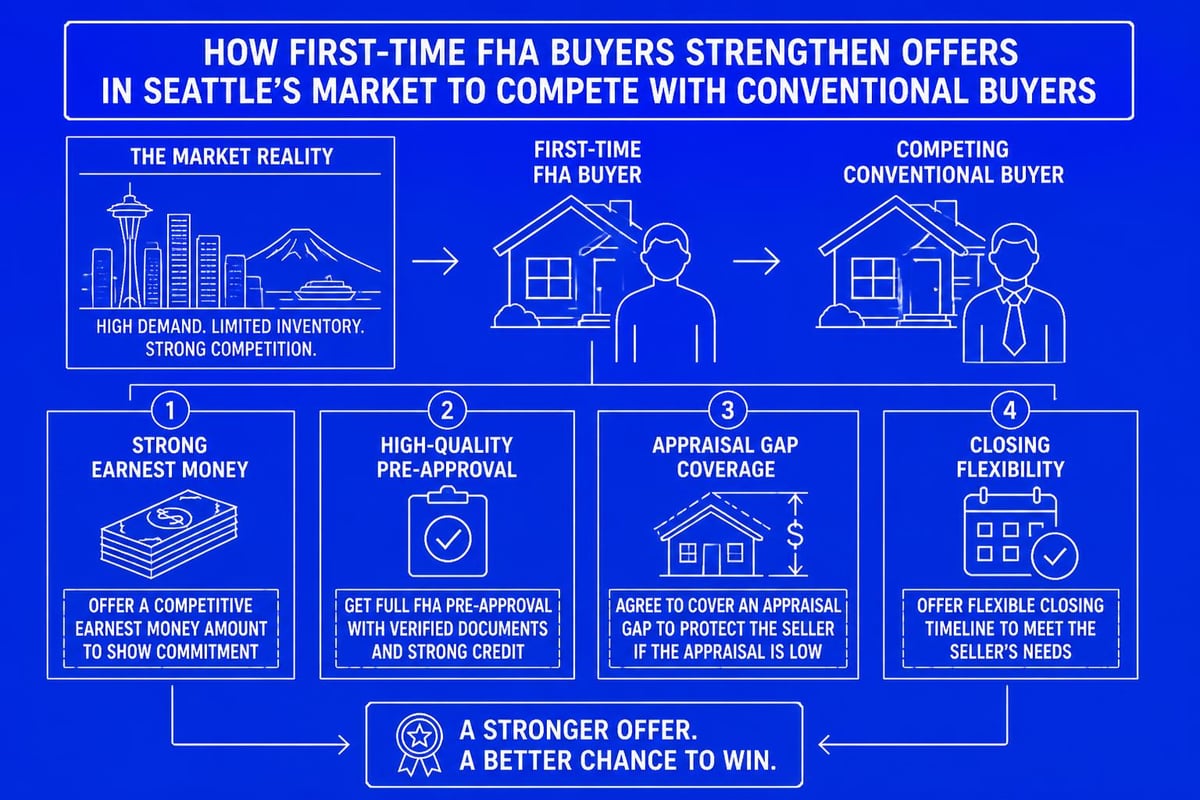

Seller Perception in Multiple-Offer Scenarios

FHA financing carries perceived risks among Seattle sellers:

- Appraisal concerns: Stricter property standards may require repairs

- Closing timeline: Potentially slower than conventional or cash

- Deal certainty: Higher chance of appraisal-related complications

In competitive neighborhoods like Wallingford, Green Lake, or West Seattle, sellers receiving multiple offers may favor conventional financing or cash. Strengthening your FHA offer requires strategic approaches:

- Larger earnest money deposits demonstrating commitment

- Pre-approval from reputable lenders with track records in Seattle

- Flexible closing timelines accommodating seller needs

- Appraisal gap coverage protecting sellers if valuation falls short

- Minimal contingencies beyond standard inspection and financing

Working with a first-time home buyer specialist who understands Seattle's market nuances helps craft competitive offers despite FHA stigma.

Timing Your Purchase and Rate Environment

Interest rates significantly impact affordability calculations. Even quarter-point differences change monthly payments substantially on $450,000+ loans common in Seattle. The home loan approval timeline typically spans 30-45 days for FHA loans, requiring buyers to lock rates strategically.

Rate lock strategies to consider:

- 30-day locks: Standard for firm closing dates, lowest cost

- 45-60 day locks: Added security for complex transactions, slight premium

- Float-down options: Capture rate decreases if market improves before closing

First-time buyers in Mill Creek, Lynnwood, or Shoreline should begin the pre-approval process 60-90 days before serious home shopping, establishing relationships with lenders who monitor rate movements and advise optimal timing.

Common Misconceptions About FHA Financing

Several persistent myths deter qualified buyers from considering first home buyer FHA loan options that might serve them well.

Myth 1: FHA loans are only for low-income buyers

Reality: FHA loans serve middle and upper-middle-income buyers who prioritize preserving liquid assets or have credit profiles below conventional thresholds. Tech professionals earning $150,000+ frequently use FHA financing strategically.

Myth 2: You must be a first-time buyer

Reality: While often utilized by first-time purchasers, FHA loans are available to any qualified borrower. Repeat buyers, investors acquiring primary residences, and those who haven't owned property recently all qualify.

Myth 3: FHA properties must be "fixer-uppers"

Reality: FHA properties must meet minimum standards, but this doesn't restrict purchases to distressed homes. Many well-maintained Seattle-area properties easily satisfy FHA requirements without repairs.

Myth 4: Closing takes significantly longer

Reality: Experienced lenders close FHA loans within standard 30-45 day timelines. Processing differences between FHA and conventional loans are minimal with efficient underwriting systems.

Maximizing Your FHA Loan Success in Seattle

Preparation distinguishes successful FHA buyers from those facing unexpected obstacles or losing homes to competing offers.

Optimize Your Financial Profile

Before beginning your home search:

- Review credit reports from all three bureaus, disputing errors immediately

- Pay down credit card balances below 30% utilization

- Avoid opening new credit accounts or making major purchases

- Accumulate 2-3 months of mortgage payments in reserves beyond down payment

- Organize two years of tax returns, pay stubs, and bank statements

- Document any non-traditional income sources with supporting evidence

For first-time buyers in Seattle juggling high rents while saving, systematic financial optimization creates qualification advantages and demonstrates preparedness to lenders and sellers.

Choose Properties Strategically

Not all Seattle neighborhoods or property types suit FHA financing equally well. Condominiums require FHA building approval, newer construction typically meets property standards easily, and certain price ranges align better with FHA loan limits.

FHA-friendly Seattle property characteristics:

- Single-family homes or townhomes (simpler approval than condos)

- Properties priced within $450,000-$498,000 range (utilizing full FHA limits)

- Well-maintained structures from any era meeting safety standards

- Sellers demonstrating flexibility and understanding of FHA requirements

- Neighborhoods with multiple recent FHA transactions (proven feasibility)

Buyers targeting Lake Forest Park, parts of Shoreline, or South Seattle often find better FHA inventory alignment than in premium neighborhoods where prices consistently exceed FHA limits.

Partner with Specialized Professionals

FHA transactions benefit tremendously from experienced professional guidance. Lenders familiar with FHA underwriting nuances, real estate agents who successfully navigate FHA offers in competitive markets, and inspectors understanding FHA appraisal standards all contribute to smoother transactions.

Key professional relationships for FHA success:

- Mortgage broker with FHA expertise: Understanding guideline flexibility and alternative documentation

- Buyer's agent experienced in first-time purchases: Crafting competitive FHA offers

- Home inspector familiar with FHA standards: Identifying potential appraisal issues early

- Insurance agent: Securing homeowner's coverage meeting FHA requirements

- Real estate attorney (optional in Washington): Reviewing contracts and contingencies

Working with professionals serving Seattle, Bellevue, Kirkland, and surrounding communities ensures local market knowledge supplements technical FHA expertise, particularly valuable when navigating Seattle’s unique home buying strategies.

Alternative Scenarios When FHA May Not Be Optimal

Despite significant advantages, certain buyer profiles or situations favor alternative financing approaches over first home buyer FHA loan programs.

High-Credit, Stable Employment Buyers

Buyers with credit scores exceeding 740, stable W-2 income, and 5-10% down payment capacity often secure better long-term value through conventional financing. Lower interest rates (typically 0.25-0.50% better than FHA) and removable PMI offset the slightly higher down payment requirement.

Quick comparison for a $475,000 Seattle home:

| Loan Type | Down Payment | Monthly P&I | Monthly MI | Total Monthly | MI Duration |

|---|---|---|---|---|---|

| FHA (3.5%) | $16,625 | $2,578 | $317 | $2,895 | Permanent |

| Conventional (5%) | $23,750 | $2,466 | $175 | $2,641 | Until 20% equity |

Over 7-10 years of typical Seattle homeownership, conventional financing saves thousands despite requiring additional upfront capital.

Buyers Exceeding FHA Loan Limits

Seattle's median home prices push many desirable properties above the $498,257 FHA limit. Buyers targeting homes in Bellevue, Mercer Island, or premium Seattle neighborhoods require conventional or jumbo financing regardless of preference for FHA features.

Understanding when down payment strategies shift based on price points helps buyers plan appropriate savings timelines for their target neighborhoods.

Investment Property Purchases

FHA loans require owner-occupancy, disqualifying them for investment properties or second homes. Real estate investors in Everett, Lynnwood, or other Seattle-area markets need conventional investment property loans with typically 15-25% down requirements and higher interest rates.

Documentation and Application Process

Understanding required documentation streamlines your first home buyer FHA loan application and prevents delays during underwriting.

Essential Documentation Checklist

Identity and employment verification:

- Government-issued photo ID (driver's license or passport)

- Social Security card or verification

- Two years of W-2 forms from all employers

- Most recent 30 days of pay stubs showing year-to-date earnings

- Employment verification letters confirming position and salary

Income documentation for specialized scenarios:

- Complete tax returns (1040 with all schedules) for self-employed buyers

- K-1 statements for partnership or S-corporation income

- Vesting schedules and grant documentation for RSU/stock compensation

- Profit and loss statements for current-year self-employment income

- Social Security, pension, or disability award letters for fixed income

Asset verification:

- Two months of bank statements for all accounts (checking, savings, investments)

- Retirement account statements if using for down payment or reserves

- Gift letters and donor bank statements for down payment assistance from family

- Documentation explaining large deposits exceeding 50% monthly income

Credit and debt information:

- Authorization for credit report pulls (provided by lender)

- Explanation letters for recent credit inquiries or score changes

- Current statements for all debts (student loans, auto loans, credit cards)

- Divorce decrees, separation agreements, or bankruptcy discharge papers if applicable

Buyers working with experienced Seattle mortgage professionals receive detailed documentation checklists customized to their specific employment and income situations, particularly valuable for tech workers with complex compensation packages.

Timeline Expectations

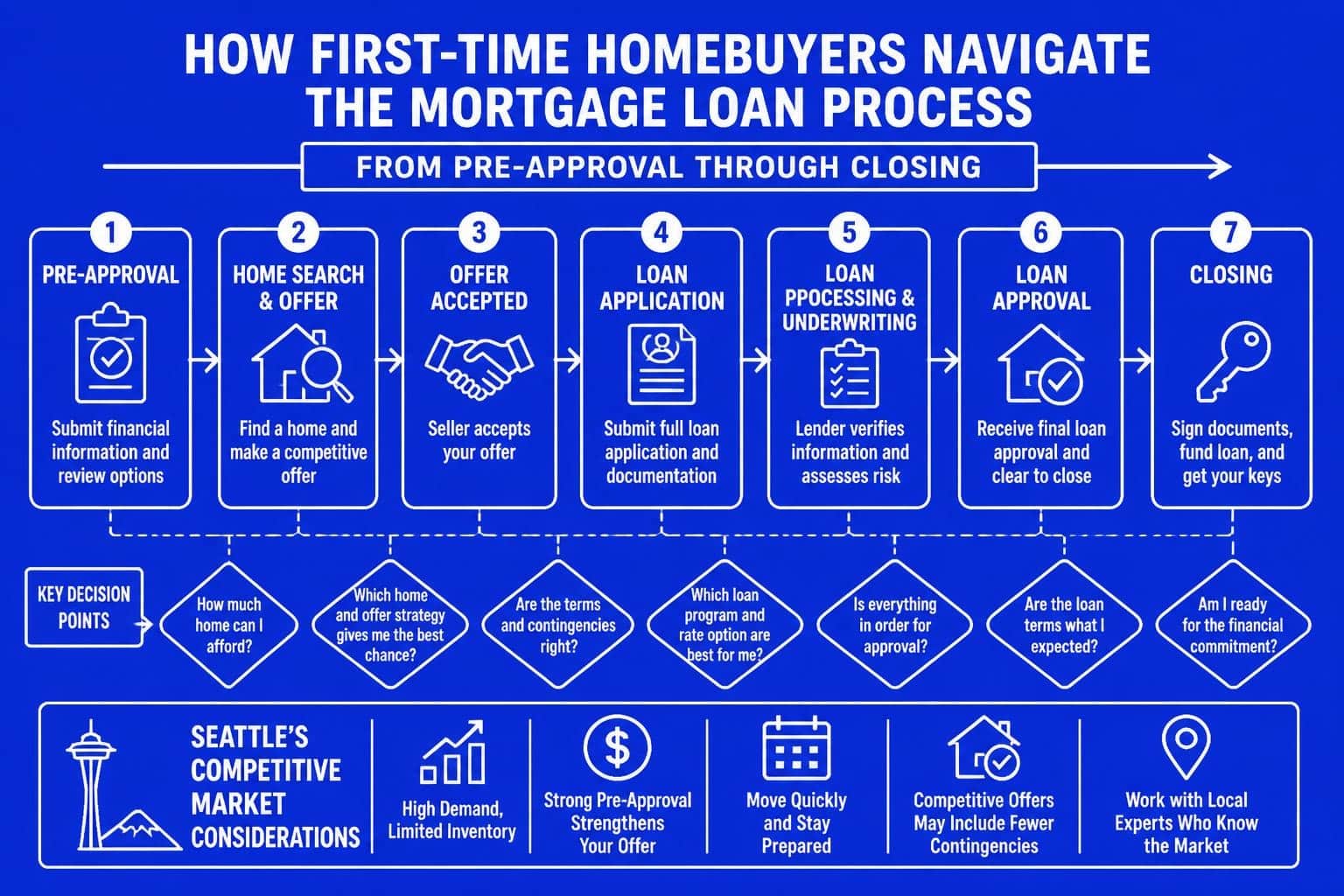

Typical FHA loan process in Seattle:

- Pre-approval (3-5 days): Initial application, credit review, preliminary approval

- Home search (varies): Active shopping with pre-approval in hand

- Offer acceptance (immediate): Signed purchase agreement with financing contingency

- Processing (7-10 days): Complete documentation submission and initial underwriting

- Appraisal ordering (1-2 days): Lender orders FHA-approved appraiser

- Appraisal completion (7-14 days): Property inspection and valuation report

- Underwriting (7-10 days): Comprehensive file review and conditional approval

- Clear to close (2-3 days): Final conditions satisfied, closing disclosure issued

- Closing (1 day): Sign documents, fund loan, receive keys

Total timeline: 30-45 days from offer acceptance to closing, though experienced lenders with streamlined processes can compress this to 21-30 days when buyers provide complete documentation promptly and properties appraise without complications.

Preparing for Closing Costs and Cash Requirements

Beyond the 3.5% down payment, first home buyer FHA loan transactions require additional cash for closing costs and potential reserves.

Typical Closing Cost Breakdown

Closing costs generally total 2-5% of the purchase price, though FHA allows sellers to contribute up to 6% toward buyer closing costs-a valuable negotiation tool in balanced markets.

Standard closing cost categories:

- Lender fees: Origination, underwriting, processing ($1,500-$3,000)

- Third-party services: Appraisal, credit report, title search ($800-$1,500)

- Title and escrow: Title insurance, escrow fees, recording ($2,000-$4,000)

- Prepaid items: Property taxes, homeowner's insurance, prepaid interest ($2,500-$5,000)

- Upfront MIP: 1.75% of base loan amount (typically financed, not paid at closing)

On a $475,000 purchase in Seattle with a $458,375 loan amount (3.5% down), expect $12,000-$18,000 in closing costs before seller credits. Negotiating seller-paid closing costs reduces out-of-pocket requirements significantly, particularly valuable when preserving reserves for post-purchase expenses.

Reserve Requirements

FHA doesn't mandate specific reserve amounts, but lenders typically require 1-3 months of PITI (principal, interest, taxes, insurance) in liquid assets after closing. Higher reserves strengthen applications and provide financial cushion for unexpected homeownership expenses.

Reserve calculation for a $2,800 monthly PITI:

- Minimum (1 month): $2,800

- Preferred (2 months): $5,600

- Strong (3+ months): $8,400+

Seattle's high cost of living makes adequate reserves particularly important, as maintenance costs, utilities, and potential HOA fees consume significant monthly budget even beyond mortgage payments.

A first home buyer FHA loan provides an accessible, realistic path to homeownership in Seattle's competitive market when conventional financing requirements seem out of reach. Understanding qualification standards, costs, strategic positioning, and long-term implications helps you make informed decisions aligned with your financial goals. Keith Akada at Mortgage Reel brings 25+ years of experience guiding first-time buyers through FHA loans and alternative programs, with specialized expertise qualifying complex income for Seattle-area tech professionals and over 750 five-star reviews reflecting his commitment to education, transparency, and reliable execution throughout the home buying journey.