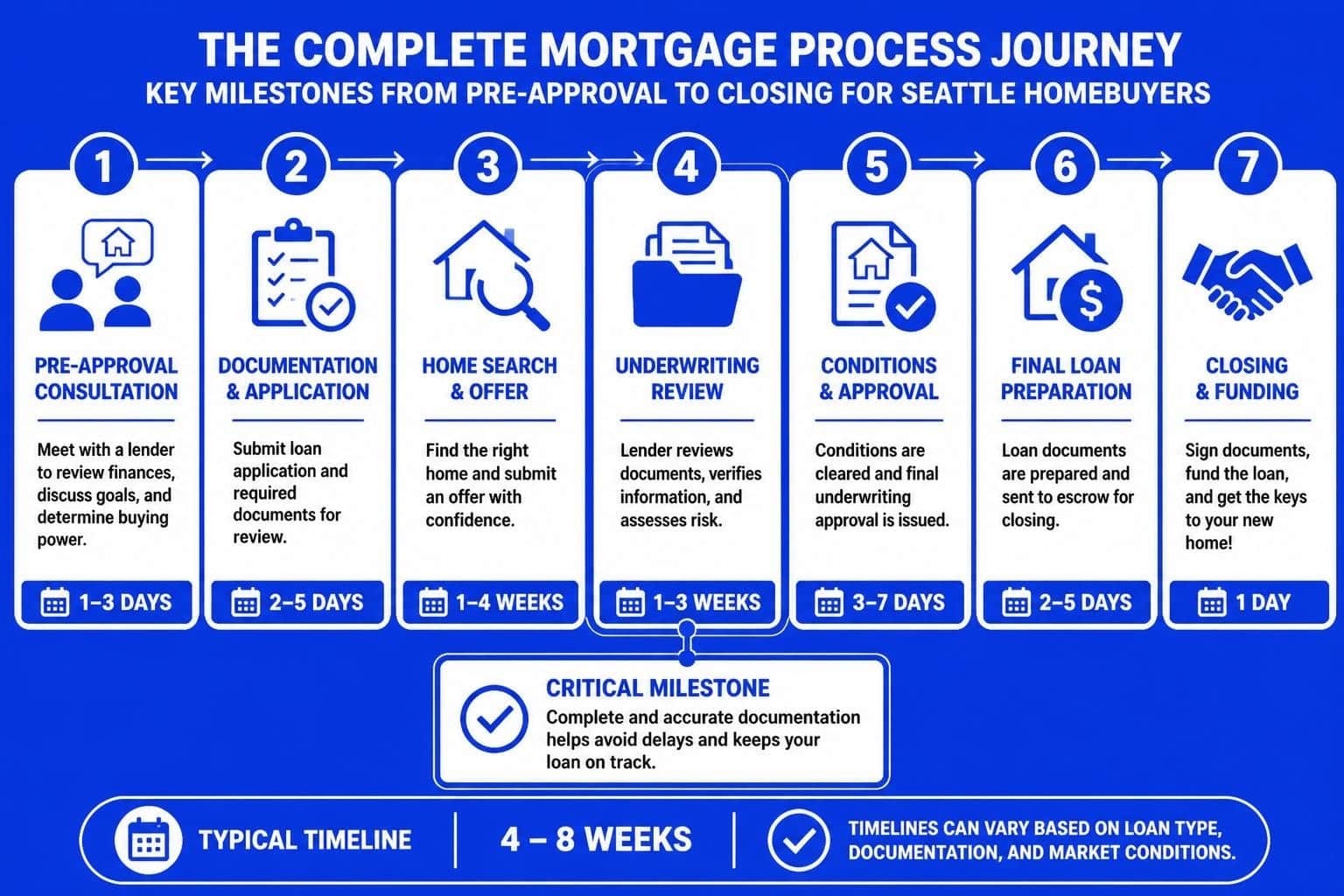

Understanding the mortgage process is essential for anyone planning to purchase or refinance a home in 2026. Whether you're a first-time buyer in Seattle or a tech professional relocating to Bellevue with complex stock compensation, knowing what to expect at each stage helps you make confident decisions and avoid unnecessary delays. The mortgage process involves multiple steps, each designed to verify your financial qualifications, assess the property value, and ensure a secure transaction. With the right guidance and preparation, you can navigate this journey smoothly and achieve your homeownership goals on schedule.

Pre-Approval: Starting Your Mortgage Process Strong

Pre-approval represents the critical first step in the mortgage process and provides a clear picture of your buying power before you start house hunting. Unlike pre-qualification, which offers a rough estimate, pre-approval involves a thorough review of your financial documents, credit history, and employment verification.

Essential documents for pre-approval include:

- Recent pay stubs (typically last 30 days)

- W-2 forms from the past two years

- Federal tax returns (two years for self-employed borrowers)

- Bank statements showing assets and reserves

- Documentation of additional income sources

For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, pre-approval requires special attention to equity compensation. RSUs, stock options, and performance bonuses can significantly increase your purchasing power, but they must be properly documented and qualified according to underwriting guidelines. A knowledgeable mortgage broker in Seattle understands how to structure these income sources to maximize your loan amount while maintaining competitive rates.

Understanding Pre-Approval Timelines

The pre-approval stage typically takes between 24 to 72 hours once you submit complete documentation. However, complex income scenarios or self-employment may extend this timeline. Working with an experienced broker streamlines the process by ensuring all documentation is properly formatted before submission.

In competitive markets like Shoreline, Lynnwood, and Mill Creek, having a strong pre-approval letter gives you a significant advantage when making offers. Sellers and listing agents recognize that pre-approved buyers are serious and financially qualified, which can make the difference in multiple-offer situations.

Application and Documentation: Building Your File

Once you've found the right property and have an accepted offer, the formal mortgage process begins with a complete loan application. This stage involves providing comprehensive financial documentation that underwriters will review to make a final lending decision.

Understanding the complete mortgage process helps you gather the right documents efficiently. Beyond the initial pre-approval documents, you'll need to provide additional paperwork related to the specific property and transaction.

Additional documentation required during application:

- Purchase agreement with all addendums

- Earnest money deposit receipt

- Homeowners insurance information

- HOA documentation (if applicable)

- Gift letter and proof of funds transfer (for down payment gifts)

- Explanation letters for any credit inquiries or deposits

| Document Type | Purpose | Timeline |

|---|---|---|

| Purchase Agreement | Establishes terms and price | Day 1 |

| Appraisal Order | Confirms property value | Days 1-3 |

| Title Search | Verifies clear ownership | Days 3-7 |

| Insurance Quote | Protects lender interest | Days 5-10 |

For Lake Forest Park and Everett buyers, local property considerations may affect documentation requirements. Septic systems, well water, or waterfront properties often require additional inspections and certifications that impact the mortgage process timeline.

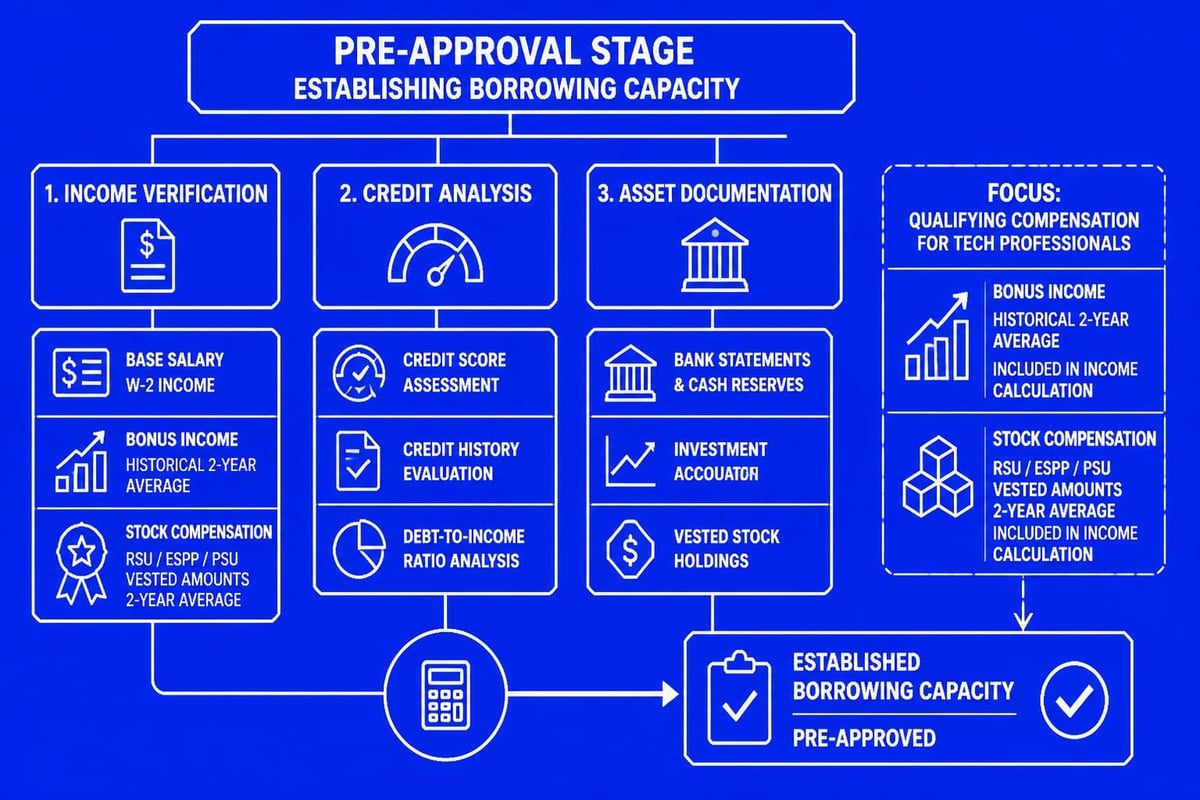

Appraisal and Property Verification

The appraisal represents a crucial checkpoint in the mortgage process where an independent professional assesses the property's market value. Lenders require appraisals to ensure the loan amount doesn't exceed the property's actual worth, protecting both their investment and yours.

Professional appraisers evaluate multiple factors including the property's condition, location, square footage, and recent comparable sales in the area. In Seattle's competitive market, appraisals sometimes come in below the purchase price, particularly during heated bidding situations. This scenario requires careful negotiation and potentially additional cash from the buyer or price renegotiation with the seller.

Managing Appraisal Challenges

When an appraisal falls short of expectations, several options exist:

- Challenge the appraisal with additional comparable sales data

- Renegotiate the purchase price with the seller

- Increase your down payment to cover the difference

- Request a second appraisal if significant errors exist

- Walk away using your appraisal contingency

Understanding how long mortgage approvals take helps you plan for potential appraisal delays. Most appraisals are completed within 7-10 days of ordering, though complex properties or busy markets may extend this timeframe.

Underwriting Review: The Decision-Making Stage

Underwriting represents the most intensive phase of the mortgage process, where a trained professional reviews every aspect of your financial profile and the property documentation. Underwriters work methodically through guidelines established by loan investors, ensuring each loan meets specific criteria for approval.

Primary underwriting focus areas include:

- Income stability and consistency

- Debt-to-income ratio calculations

- Credit history and payment patterns

- Asset verification and source of funds

- Property condition and insurability

During underwriting, you may receive requests for additional documentation called conditions. These requests are standard practice and don't indicate problems with your application. Common conditions include updated pay stubs, explanations for large deposits, or clarification on employment gaps.

Tech professionals in Bellevue and Redmond often face additional scrutiny regarding equity compensation. Underwriters must verify the vesting schedule, historical stock values, and company stability when qualifying RSUs and options. This specialized knowledge separates experienced mortgage brokers from general lenders who may not maximize your qualification potential.

Timeline Expectations for Underwriting

The underwriting phase typically requires 3-7 business days for initial review, with additional time needed if conditions are issued. How the mortgage process works varies by lender capability and loan complexity. Advanced underwriting systems and experienced processors can significantly reduce this timeline, with some lenders offering conditional approval within 24-48 hours.

Maintaining open communication with your loan team during underwriting prevents delays. Respond promptly to condition requests, avoid making major financial changes, and keep your broker informed of any employment or income adjustments.

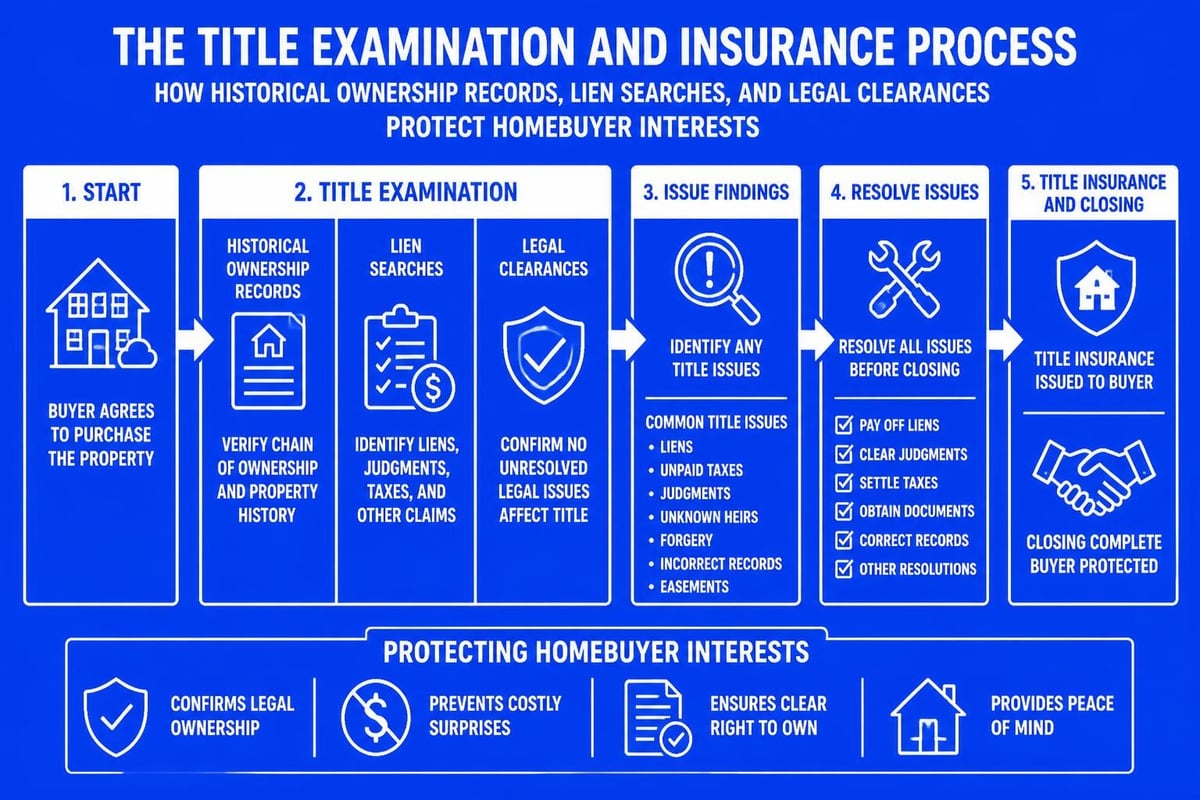

Title Search and Insurance Requirements

While underwriting reviews your financial qualifications, the title company conducts a parallel investigation into the property's ownership history. The title search uncovers any liens, encumbrances, or legal claims that could affect your ownership rights after closing.

Title insurance protects both you and your lender against future claims related to ownership disputes, undiscovered liens, or title defects. Two policies are typically issued: a lender's policy (required) and an owner's policy (optional but recommended).

| Title Issue | Impact | Resolution |

|---|---|---|

| Unpaid Property Taxes | Prevents closing | Seller must pay or arrange payoff |

| Mechanic's Lien | Clouds title | Contractor payment or bond required |

| Boundary Disputes | Questions ownership | Survey and legal resolution |

| Undisclosed Heirs | Ownership challenge | Probate or quit claim deed |

In older Seattle neighborhoods and surrounding areas like Shoreline, title issues occasionally surface due to incomplete historical records or family estate complications. Experienced title companies identify and resolve these issues before closing, ensuring a clean transfer of ownership.

Final Approval and Clear to Close

Receiving "clear to close" status marks the successful completion of all underwriting conditions and verification requirements. At this stage, your loan is fully approved and ready for closing preparation. The clear to close represents a major milestone in the mortgage process, signaling that financing is secured barring any last-minute changes.

Critical actions during the clear to close period:

- Review your Closing Disclosure carefully

- Verify all loan terms match your expectations

- Confirm wire transfer instructions with the title company

- Schedule a final walk-through of the property

- Avoid major purchases or credit inquiries

The Closing Disclosure must be delivered at least three business days before your scheduled closing date, as required by federal law. This document details your final loan terms, closing costs, and cash required to close. Guidance from the Consumer Financial Protection Bureau helps borrowers understand their closing documents and rights.

Preparing for Closing Day

Closing day preparation involves gathering required identification, arranging fund transfers, and reviewing final settlement numbers. Your loan officer should provide a detailed closing checklist that outlines exactly what to bring and expect during the signing appointment.

Most closings in Washington State occur at title company offices, though mobile notary services are available for convenience. The signing appointment typically requires 60-90 minutes to review and execute all documents, including the promissory note, deed of trust, and numerous disclosure statements.

Rate Lock Strategy and Market Timing

Interest rate management represents a sophisticated element of the mortgage process that significantly impacts your long-term housing costs. A rate lock guarantees a specific interest rate for a defined period, protecting you from market fluctuations during the loan processing timeline.

Standard rate lock periods include 30, 45, or 60 days, with longer locks available for new construction or complex transactions. The optimal lock timing balances market conditions with your closing timeline. Locking too early may mean missing rate improvements, while waiting too long exposes you to potential increases.

Monitoring current Seattle mortgage rates helps you make informed decisions about rate lock timing. Experienced brokers provide market insights and recommendations based on economic indicators, Federal Reserve actions, and mortgage bond performance.

Float-Down Options and Rate Protection

Some lenders offer float-down provisions that allow you to capture lower rates if the market improves after locking. These options typically come with specific requirements, such as a minimum rate decrease threshold (often 0.25% to 0.50%) and may involve additional fees.

Understanding mortgage broker pricing helps you evaluate whether rate protection features provide genuine value or simply add unnecessary costs. Transparent brokers explain all pricing components and help you select the optimal strategy for your situation.

Common Mortgage Process Challenges and Solutions

Even well-prepared borrowers encounter obstacles during the mortgage process. Anticipating common challenges and knowing how to address them keeps your transaction moving forward smoothly.

Frequent mortgage process complications:

- Employment verification delays from HR departments

- Appraisal scheduling conflicts in busy markets

- Last-minute credit score changes from new inquiries

- Self-employment income calculation disagreements

- Property inspection issues requiring repairs

For self-employed borrowers in Mill Creek and Everett, income calculation represents the most common challenge. Underwriters analyze tax returns conservatively, often taking two-year averages and making adjustments for non-cash expenses. Working with a broker experienced in self-employment scenarios ensures your income is presented optimally from the start.

Communication breakdowns between parties can derail otherwise smooth transactions. Maintaining regular contact with your loan officer, real estate agent, and title company ensures everyone stays aligned on timelines and requirements. Strategies for successful home buying emphasize proactive coordination among all transaction participants.

Special Considerations for Tech Professionals

Seattle's concentration of technology employers creates unique mortgage process considerations for professionals with equity compensation. Stock-based pay, RSUs, and performance bonuses require specialized qualification approaches that differ significantly from traditional W-2 income.

Lenders typically require a two-year history of receiving equity compensation before fully counting it toward income qualification. However, experienced underwriters can make exceptions for professionals with strong base salaries, significant assets, or guaranteed vesting schedules. The key lies in proper documentation and presentation of the compensation structure.

Maximizing tech income qualification:

- Provide detailed RSU vesting schedules from your employer

- Document historical stock compensation from W-2s and pay stubs

- Show consistent or increasing grant patterns

- Demonstrate company stability and performance

- Maintain liquid assets separate from equity holdings

Jumbo loan qualification for higher-priced properties in Bellevue and Seattle requires additional scrutiny of income stability and reserves. Tech professionals often benefit from jumbo loan programs specifically designed for high-income borrowers with non-traditional compensation structures.

Refinance Process Variations

The mortgage process for refinancing shares many similarities with purchase transactions but includes some distinct differences. Refinance applications don't involve purchase contracts, earnest money, or seller negotiations, which can simplify certain aspects while introducing other considerations.

Key refinance process distinctions:

- No purchase agreement required

- Home value established through appraisal only

- Existing mortgage payoff coordination

- Potential cash-out proceeds calculation

- Different timeline expectations

Understanding mortgage loan approvals helps set realistic expectations for both purchase and refinance transactions. Refinances often close faster than purchases because they eliminate seller coordination and purchase contract contingencies.

Rate-and-term refinances, which simply adjust your interest rate or loan duration without extracting equity, typically process more quickly than cash-out refinances. Cash-out transactions involve additional scrutiny regarding the use of funds and overall debt positioning.

Documentation Best Practices Throughout the Process

Maintaining organized, complete documentation throughout the mortgage process prevents delays and demonstrates financial responsibility to underwriters. Digital document management systems make it easier to track required paperwork and respond quickly to condition requests.

Create a dedicated folder system organizing documents by category: income verification, asset documentation, property information, and correspondence. Many borrowers find cloud-based storage helpful for accessing documents from multiple devices and sharing with their loan team efficiently.

Document organization tips:

- Scan or photograph all physical documents

- Use clear, descriptive file names with dates

- Keep original documents in a safe location

- Respond to requests within 24 hours when possible

- Ask questions immediately if requests seem unclear

Proactive documentation management accelerates the mortgage process significantly. Rather than waiting for specific requests, provide comprehensive documentation upfront and update materials monthly as you receive new pay stubs or bank statements.

Working with Your Loan Team Effectively

The mortgage process involves collaboration among multiple professionals, each playing a specific role in bringing your loan to closing. Your loan officer coordinates the overall process, while processors handle documentation, underwriters make credit decisions, and closers prepare final paperwork.

Understanding each team member's role helps you direct questions appropriately and maintain realistic expectations about response times. Loan officers focus on loan structuring and client communication, while processors manage day-to-day documentation flow and condition clearance.

Building productive lender relationships:

- Establish preferred communication methods early

- Provide complete responses to information requests

- Keep your team informed of any financial changes

- Review documents promptly when received

- Trust professional recommendations while asking questions

Experience matters significantly in mortgage execution, particularly in competitive markets with tight timelines. Getting approved for a mortgage loan becomes more predictable when working with seasoned professionals who anticipate challenges and structure solutions proactively. Look for loan officers with extensive local market knowledge, strong lender relationships, and proven track records of on-time closings.

Final Walk-Through and Closing Preparation

The final walk-through occurs within 24 hours of closing and provides your last opportunity to verify the property's condition before taking ownership. This inspection confirms that agreed-upon repairs were completed, fixtures and appliances remain with the property, and no new damage occurred since your initial inspection.

Bring your purchase agreement and inspection reports to reference during the walk-through. Test major systems including plumbing, electrical, heating, and cooling. Check that all seller-owned items listed in the contract are present and in working condition.

If significant issues arise during the final walk-through, you have several options including delaying closing until repairs are completed, negotiating a credit at closing, or establishing an escrow holdback for post-closing resolution. Your real estate agent and loan officer can advise on the best approach based on the specific circumstances.

Closing Day Execution

Closing day represents the culmination of the entire mortgage process. You'll review and sign numerous documents, transfer funds, and receive the keys to your new property. The title company manages the closing appointment and ensures all documents are properly executed and recorded.

Essential closing day items:

- Government-issued photo identification

- Cashier's check or wire confirmation for closing funds

- Proof of homeowners insurance with lender listed as mortgagee

- Any required inspection reports or certifications

- Questions about documents you don't understand

Comprehensive mortgage process guides emphasize the importance of reading every document before signing. Don't hesitate to ask questions or request clarification about any terms, numbers, or obligations. The closing agent is required to explain each document and ensure you understand what you're signing.

After all documents are signed and funds are transferred, the deed and deed of trust are recorded with the county, officially transferring ownership to you and establishing the lender's security interest in the property.

Successfully navigating the mortgage process requires preparation, organization, and experienced guidance at every stage from pre-approval through closing. Understanding each phase helps you anticipate requirements, avoid delays, and make confident decisions about one of life's most significant financial commitments. Keith Akada and the team at Mortgage Reel bring over 25 years of expertise serving Seattle, Bellevue, Redmond, and Kirkland homebuyers with transparent communication, strategic advice, and proven execution in competitive markets. Whether you're a first-time buyer or a tech professional with complex compensation, our specialized approach to qualifying income and structuring loans maximizes your purchasing power while delivering reliable closings in as few as 9 business days.