Real estate investment continues to thrive across the Greater Seattle market, from downtown high-rises to single-family rentals in Shoreline and Lynnwood. Whether you're acquiring your first rental property in Lake Forest Park or expanding a portfolio across Everett and Mill Creek, securing the right financing determines your success. Real estate loans for investors function differently than traditional owner-occupied mortgages, with unique qualification standards, down payment requirements, and rate structures designed specifically for income-producing properties. Understanding these specialized financing options enables investors to maximize leverage, preserve capital for additional acquisitions, and build sustainable cash-flowing portfolios in one of the nation's most competitive real estate markets.

Understanding Real Estate Loans for Investors

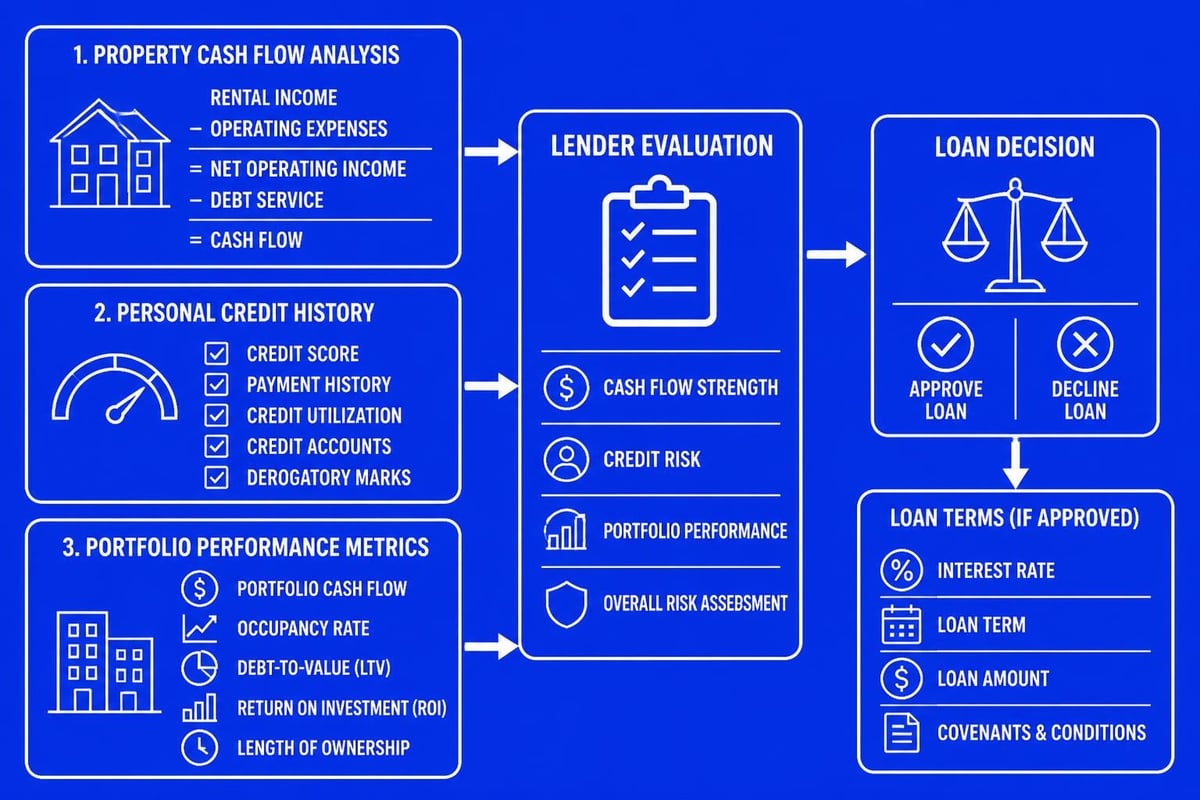

Investment property financing operates under fundamentally different guidelines than traditional residential mortgages. Lenders assess risk based on the property's income potential rather than solely focusing on personal employment history.

Key differences include:

- Higher down payment requirements, typically 15-25%

- Interest rates averaging 0.50-0.75% higher than owner-occupied rates

- Stricter credit score minimums, usually 680 or above

- Income verification through rental performance metrics

- Reserve requirements covering 6-12 months of mortgage payments

The Seattle metro area presents unique opportunities for investors targeting appreciation and rental demand driven by tech employment. Properties near Amazon campuses in Bellevue or Microsoft facilities in Redmond command premium rents, supporting higher leverage ratios when structured correctly.

Portfolio Size and Financing Strategy

Your current portfolio size directly impacts which real estate loans for investors you'll qualify for. Conventional financing through Fannie Mae and Freddie Mac allows up to 10 financed properties per borrower, while portfolio lenders may finance unlimited acquisitions.

First-time investors often start with conventional financing, which offers competitive rates and predictable underwriting. Conventional loan lenders evaluate both personal income and projected rental income when calculating debt-to-income ratios, making qualification accessible for W-2 earners with stable employment.

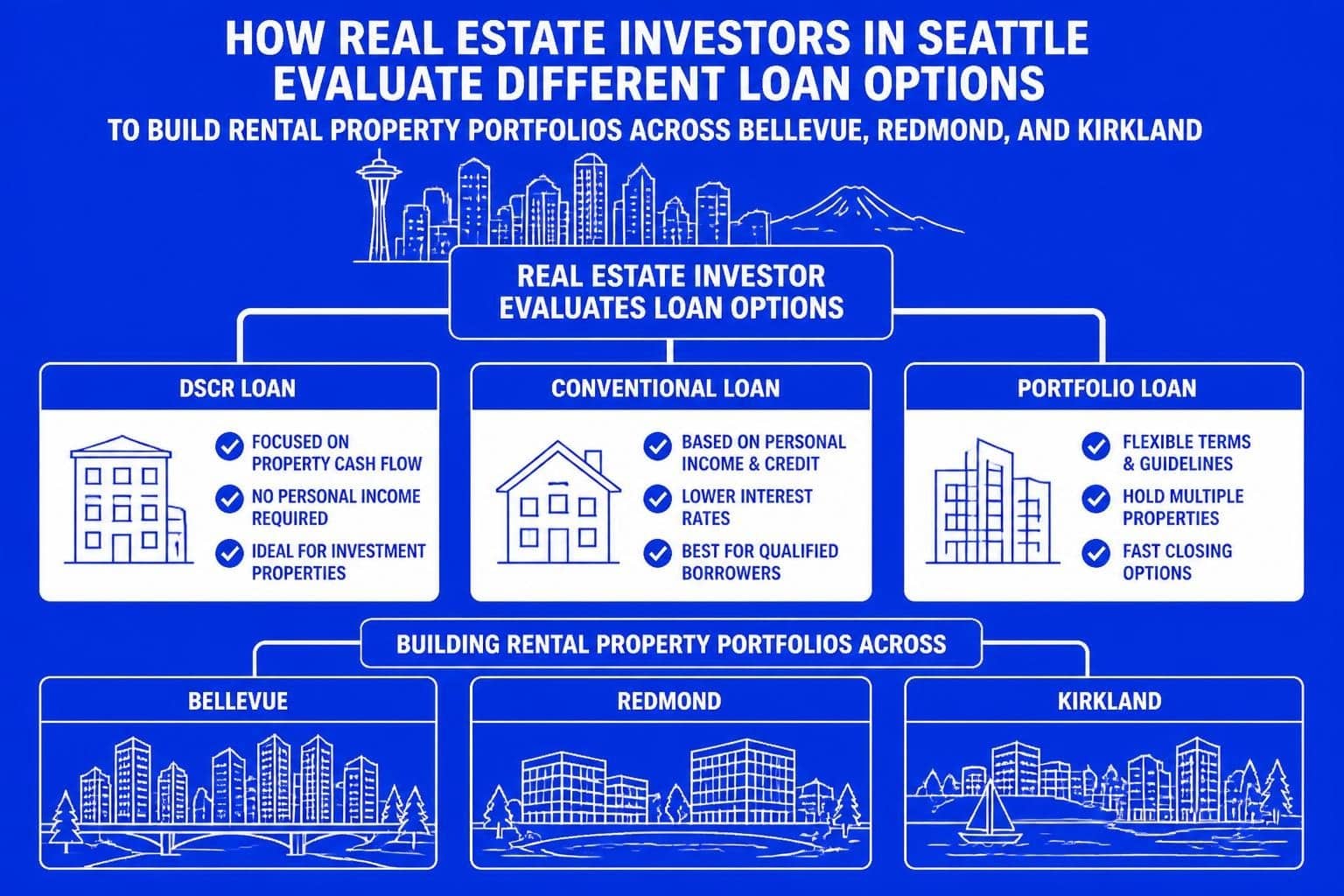

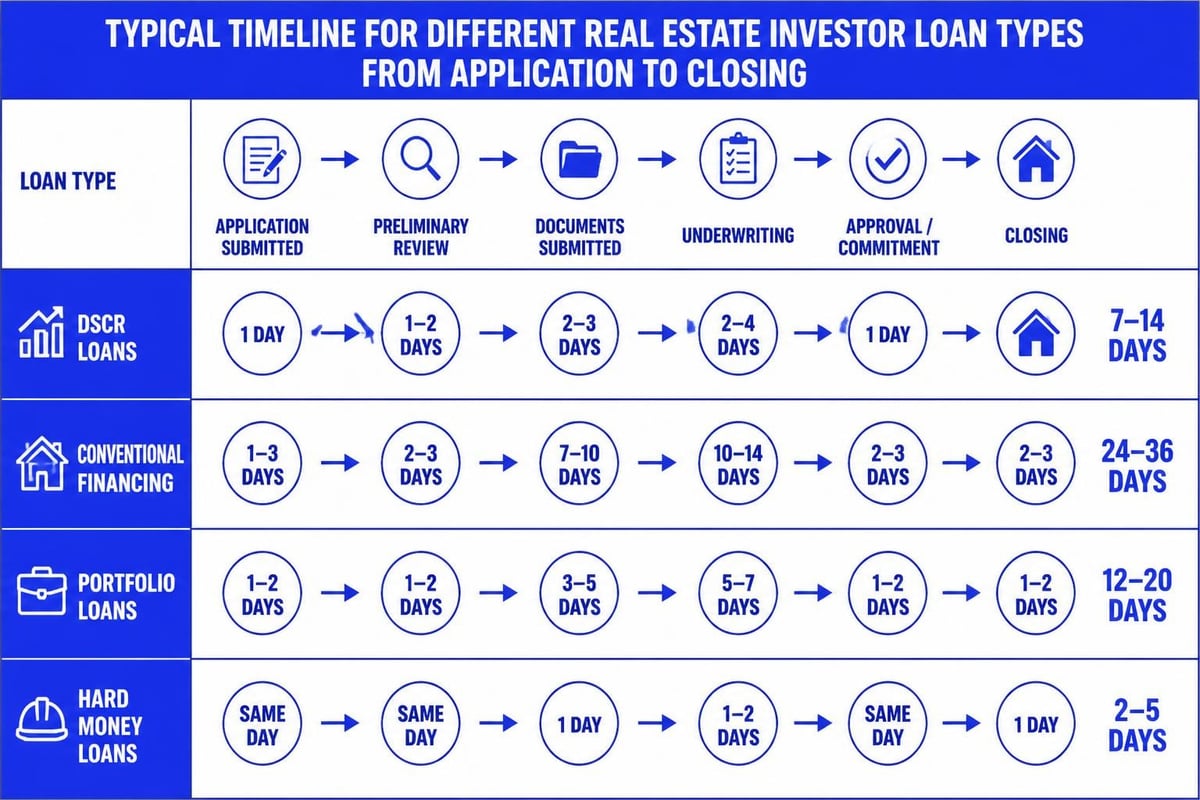

DSCR Loans: Income-Based Financing

Debt Service Coverage Ratio (DSCR) loans have revolutionized investor financing by eliminating traditional income verification requirements. These specialized real estate loans for investors qualify borrowers based exclusively on the property's rental income compared to its mortgage payment.

How DSCR Calculations Work

| DSCR Ratio | Property Performance | Typical Outcome |

|---|---|---|

| 1.25 or higher | Strong cash flow | Best rates, standard down payment |

| 1.0-1.24 | Break-even to modest cash flow | Slightly higher rates, approved |

| 0.75-0.99 | Negative cash flow | Higher rates, larger down payment required |

A property generating $3,500 monthly rent with a $2,800 total monthly payment (PITI) produces a DSCR of 1.25, considered excellent by most lenders. This ratio demonstrates the property generates 25% more income than required for debt service.

Seattle's strong rental market makes DSCR financing particularly attractive. According to various DSCR loan options for investors, these programs offer fixed-rate and adjustable-rate structures suitable for different hold strategies. Properties in Mill Creek or Lynnwood with stable tenant demand qualify readily under these guidelines.

DSCR loan advantages include:

- No tax returns or pay stubs required

- Qualification for self-employed investors simplified

- Unlimited number of financed properties

- Faster underwriting with fewer documentation requirements

- Ability to close in corporate name (LLC financing available)

The trade-off involves slightly higher interest rates, typically 0.25-0.75% above conventional investor rates, and minimum credit scores around 680-700 depending on the lender.

Conventional Investment Property Loans

Conventional financing remains the gold standard for real estate loans for investors with strong personal income and credit profiles. These loans offer the most competitive rates and lowest down payment options available to investors.

Fannie Mae and Freddie Mac guidelines permit financing up to 10 properties simultaneously. Down payment requirements start at 15% for single-unit properties, increasing to 25% for two-to-four unit buildings.

Rental Income Calculation Methods

Lenders use different approaches when calculating rental income for qualification:

- Market Rent Analysis: Appraiser determines fair market rent based on comparable properties

- Lease Agreement: Existing lease provides documented income (75% typically counted)

- Tax Return History: Schedule E showing two-year rental income history (most conservative)

For Seattle investors, understanding these calculation methods proves critical. A Lake Forest Park duplex might appraise with $4,000 monthly market rent, but if you're purchasing with existing tenants paying $3,200, lenders may use the lower figure for qualification purposes.

The mortgage lending process for investment properties requires more extensive documentation than primary residence financing, including detailed property analysis and comprehensive reserve verification.

Portfolio Loans and Private Lending

When conventional financing limits are reached or properties don't meet agency guidelines, portfolio loans provide flexible alternatives. These real estate loans for investors are held by the originating bank rather than sold to secondary markets.

Portfolio loan characteristics:

- Customized underwriting based on relationship and total portfolio performance

- No strict limit on number of financed properties

- Flexible qualification for unique property types

- Potentially higher rates reflecting increased lender risk

- May include cross-collateralization across multiple properties

Private lenders and hard money loans serve investors pursuing fix-and-flip strategies or properties requiring significant rehabilitation. These short-term financing solutions bridge gaps when traditional financing isn't available or speed is essential in competitive Seattle markets.

According to guidance on choosing real estate investor loans, matching financing to your specific investment strategy determines both acquisition success and long-term profitability.

Jumbo Investment Property Financing

Seattle's high property values frequently push investment acquisitions into jumbo loan territory. Properties exceeding $766,550 in King County require jumbo financing, which follows different guidelines than conforming conventional loans.

Jumbo Loan Requirements for Investors

| Requirement Category | Minimum Standard | Competitive Profile |

|---|---|---|

| Credit Score | 700 | 740+ |

| Down Payment | 25% | 30% |

| Reserves | 12 months | 18-24 months |

| Debt-to-Income Ratio | 43% | 36% or below |

For tech professionals working at Amazon or Microsoft with substantial stock compensation, jumbo home loans can be structured using RSUs and bonus income to qualify for higher loan amounts. This strategy proves particularly valuable when acquiring investment properties in Bellevue or Redmond where property values command premium prices.

Jumbo real estate loans for investors typically require more liquid reserves than conforming loans. Lenders want to see 12-24 months of PITI payments available across all financed investment properties, demonstrating capacity to weather vacancy periods or market downturns.

Commercial Real Estate Financing Options

Properties containing five or more units shift from residential to commercial financing territory. These real estate loans for investors operate under completely different underwriting standards focused entirely on property performance.

Commercial loan structures include:

- Traditional Commercial Mortgages: 20-25 year amortization, 5-10 year terms, recourse debt

- SBA 504 Loans: Low down payment option for owner-occupied commercial properties

- Bridge Loans: Short-term financing for value-add repositioning

- CMBS Loans: Non-recourse debt for larger stabilized properties

Exploring types of commercial real estate financing reveals options suited to different property sizes and business plans. A 12-unit apartment building in Everett qualifies for permanent commercial financing, while a mixed-use property in downtown Seattle might utilize construction-to-permanent financing.

Commercial lenders evaluate net operating income (NOI), property location, tenant quality, and sponsor experience when underwriting loans. Personal guarantees are typically required for loans under $5 million, though non-recourse options exist for larger, stabilized assets.

Loan-to-Value Considerations

Commercial real estate loans for investors rarely exceed 75% LTV, with most permanent financing settling between 65-75% depending on property type and location. Cash flow coverage requirements generally mandate 1.25x DSCR minimum, with stronger borrowers achieving better rate pricing.

Seattle's multifamily market supports aggressive underwriting due to consistent rental demand and limited new construction in established neighborhoods. Properties near transit corridors or major employment centers receive preferential pricing from commercial lenders.

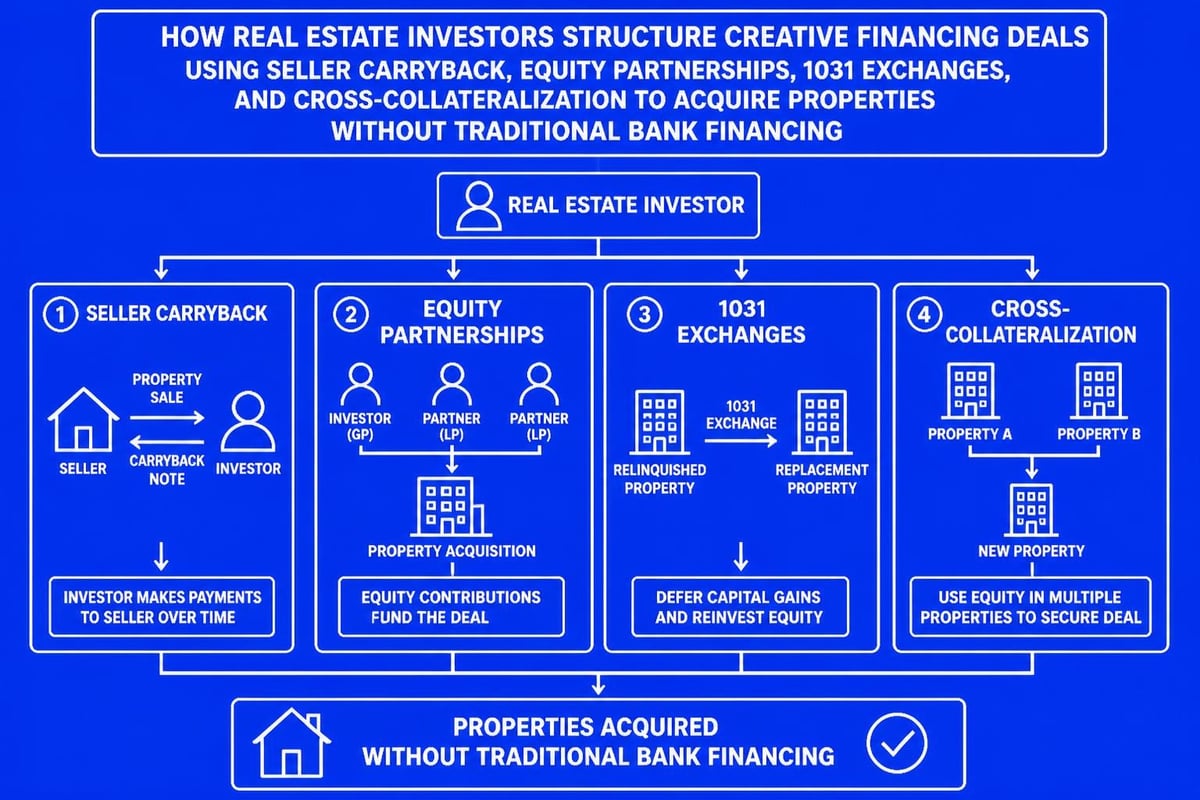

Asset-Based Lending and Creative Financing

Beyond traditional real estate loans for investors, creative financing strategies unlock deals that don't fit conventional boxes. These approaches prove particularly valuable for experienced investors with track records.

Seller financing provides flexible terms negotiated directly with property owners. In markets where sellers own properties free and clear, they may offer financing at competitive rates while deferring capital gains taxes through installment sales.

Creative financing options include:

- Home equity lines of credit (HELOC) for down payments

- 1031 exchanges for tax-deferred portfolio growth

- Partnerships with capital partners (debt vs. equity structures)

- Self-directed IRA investments in real estate

- Cross-collateralization using existing equity

Lake Forest Park and Shoreline markets occasionally present seller financing opportunities, particularly with older owners seeking steady income streams rather than lump-sum sales proceeds. These arrangements bypass traditional lending altogether while potentially offering better terms than institutional financing.

Qualifying Investment Income for Future Purchases

Building a sustainable investment portfolio requires understanding how lenders count rental income for subsequent purchases. This knowledge directly impacts your capacity to scale acquisitions efficiently.

Rental Income Seasoning Requirements

For properties owned less than one year, most lenders require:

- Current lease agreement in place

- Market rent appraisal supporting income figures

- Application of 75% income factor for qualification

- Full PITI expenses deducted from gross rents

After owning a property for one tax year, Schedule E documentation becomes available. Lenders typically average the most recent two years of net rental income, adding back non-cash expenses like depreciation to determine qualifying income.

The difference proves substantial. A Lynnwood rental property generating $2,400 monthly might only contribute $1,350 toward qualifying income ($2,400 x 0.75 = $1,800, minus $450 PITI) when newly acquired. After two tax years showing strong performance, that same property might contribute $1,800 or more based on actual reported income plus depreciation add-backs.

Smart investors structure initial acquisitions with strong cash flow, knowing those properties will support qualification for subsequent purchases within 12-24 months. This strategy accelerates portfolio growth without requiring proportional increases in W-2 income.

Down Payment and Reserve Strategies

Capital preservation determines how quickly investors can scale portfolios. While real estate loans for investors require higher down payments than owner-occupied financing, strategic approaches minimize cash requirements while maintaining qualification strength.

Minimum Down Payment by Property Type

| Property Category | Minimum Down Payment | Optimal Down Payment |

|---|---|---|

| Single-family rental | 15% | 20-25% |

| 2-4 unit property | 25% | 25-30% |

| 5+ units (commercial) | 25% | 30-35% |

| Fix-and-flip projects | 10-20% hard money | Varies by deal |

Reserve requirements vary by lender and portfolio size. First-time investors might qualify with six months reserves, while investors holding multiple properties need 12-18 months of PITI payments across all financed investment properties.

Bellevue and Redmond investors with high W-2 incomes from tech employment often leverage mortgage financing options that allow retirement account statements to satisfy reserve requirements without liquidating positions. This preserves investment growth while meeting lender guidelines.

Interest Rate and Term Structures

Real estate loans for investors span various rate structures and term options, each suited to different hold strategies and market outlooks. Understanding these options enables investors to match financing to business plans effectively.

Fixed-rate investment mortgages provide payment stability and protection against rising rates. These prove ideal for long-term buy-and-hold strategies where consistent cash flow matters more than initial rate minimization. Terms typically run 15 or 30 years, with 30-year amortization preserving cash flow while 15-year terms build equity faster.

Adjustable-rate mortgages (ARMs) offer lower initial rates with adjustment periods after 3, 5, 7, or 10 years. Investors planning to refinance, sell, or substantially improve properties within the fixed period benefit from reduced initial payments, improving cash-on-cash returns during the hold period.

Mill Creek investors pursuing value-add strategies might select 5-year ARMs, planning to refinance into permanent fixed-rate financing once renovations complete and rents stabilize at higher levels. The initial rate savings accelerates renovation funding while lower payments support qualification despite temporarily reduced occupancy.

Interest-only loans exist in portfolio and jumbo investor financing, though less common than during previous cycles. These maximize cash flow by deferring principal payments, suitable for investors prioritizing distribution over equity accumulation.

Tax Implications and Loan Structuring

Financing structures directly impact tax treatment and asset protection strategies. Real estate loans for investors should align with overall business entity structures and tax planning objectives.

Entity-Based Financing

Most conventional lenders require personal guarantees regardless of property ownership structure. However, some portfolio lenders and DSCR programs permit true LLC-to-LLC financing without personal recourse, providing liability protection and estate planning benefits.

Considerations include:

- Due-on-sale clauses triggered by transferring property into LLCs after closing

- Interest rate premiums for LLC financing (typically 0.25-0.50%)

- Legal and accounting costs maintaining separate entities

- Reduced personal credit impact from property performance

Investors holding multiple Everett or Seattle properties often establish separate LLCs per property or small portfolios, limiting cross-exposure if issues arise with individual assets. Financing these entities separately maintains this firewall, though costs more than blanket personal guarantees across portfolios.

Mortgage interest deductibility remains a significant tax advantage for real estate investors. Unlike the $750,000 limit on personal residence mortgage interest deductions, investment property interest deductions have no cap, making leverage particularly attractive from a tax perspective.

Working with Specialized Mortgage Professionals

Navigating the complexity of real estate loans for investors requires expertise beyond typical residential mortgage knowledge. Experienced loan officers specializing in investment property financing understand nuanced guidelines and can structure deals maximizing qualification capacity.

What to look for in an investor-focused mortgage broker:

- Experience with multiple investor loan programs (DSCR, portfolio, conventional)

- Understanding of rental income calculations and portfolio qualification

- Relationships with investors-friendly underwriters

- Track record closing investment property transactions

- Knowledge of local rental markets and property valuations

According to information on choosing the right mortgage lenders, investors benefit from brokers with access to multiple investor-friendly lenders rather than working directly with single-institution loan officers whose options are limited to their employer's products.

Seattle's competitive investment property market demands quick execution. Brokers familiar with local appraisal timelines, title company capabilities, and lender turn times help investors win competitive bids through realistic close-date commitments and minimal contingency periods.

Planning Your Investment Financing Strategy

Successful real estate investors think several acquisitions ahead, structuring each purchase to support subsequent deals. This forward-thinking approach to real estate loans for investors separates accidental landlords from intentional portfolio builders.

Creating a Financing Roadmap

- Assess current qualification capacity: Calculate maximum debt-to-income ratios and available reserves

- Prioritize high-cash-flow acquisitions initially: Build rental income supporting future purchases

- Maintain strong personal credit: Protect scores through careful credit utilization and payment history

- Build lender relationships early: Establish track records before needing maximum flexibility

- Plan refinancing cycles: Take advantage of rate drops and seasoned rental income

Properties in Shoreline or Lake Forest Park might cash flow more modestly than suburban markets, but appreciation potential and stable tenant demand justify acquisition when structured properly. Balancing cash flow with appreciation goals determines optimal financing approaches for different property types.

Long-term investors often mix financing types across portfolios. Core properties held indefinitely might carry 30-year fixed-rate mortgages for stability, while opportunistic acquisitions use bridge loans or hard money for quick execution, later refinancing into permanent debt once stabilized.

Rate Shopping and Program Comparison

Interest rate differences of 0.25-0.50% dramatically impact long-term returns on real estate loans for investors. A $500,000 investment property loan at 7.00% versus 7.50% represents over $35,000 in additional interest costs over 10 years.

Compare programs across these dimensions:

- Interest rate and annual percentage rate (APR)

- Origination fees and closing costs

- Prepayment penalties (common on investor loans)

- Rate lock periods and extension fees

- Post-closing seasoning requirements before refinancing

Understanding the various types of commercial loans and investment property programs available ensures you're evaluating all options rather than settling for the first approval received. Some lenders specialize in certain property types or investor profiles, offering meaningfully better terms for deals matching their sweet spot.

Portfolio lenders sometimes offer relationship pricing, reducing rates for borrowers maintaining deposit accounts or concentrating multiple properties with their institution. These arrangements create win-win scenarios where investor benefits from reduced costs while lenders increase total relationship profitability.

Financing investment properties successfully requires understanding the specialized loan products designed for real estate investors and matching them to your specific acquisition strategy and portfolio goals. Whether you're purchasing your first rental property or expanding an established portfolio across the Seattle metro area, working with an experienced mortgage professional who understands investor financing makes the difference between adequate execution and optimal results. Keith Akada at Mortgage Reel brings over 25 years of experience helping real estate investors across Seattle, Bellevue, Redmond, and Kirkland secure competitive financing for single-family rentals, multi-unit properties, and portfolio growth strategies, with specialized knowledge qualifying complex income structures and executing closings in as few as 9 business days.