Investing in rental properties throughout Seattle, Bellevue, Redmond, and surrounding areas requires securing the right financing from lenders who understand investment real estate. Unlike traditional home loans, rental property mortgage lenders evaluate properties based on income potential, debt service coverage ratios, and investor experience rather than solely personal employment history. For tech professionals at Amazon, Microsoft, and Google looking to diversify their wealth beyond stock compensation, understanding the specialized lending landscape for investment properties becomes crucial to building a successful real estate portfolio. This comprehensive guide explores how rental property financing works, what lenders require, and strategies to secure competitive terms in competitive markets like Kirkland and Shoreline.

Understanding Rental Property Mortgage Lenders

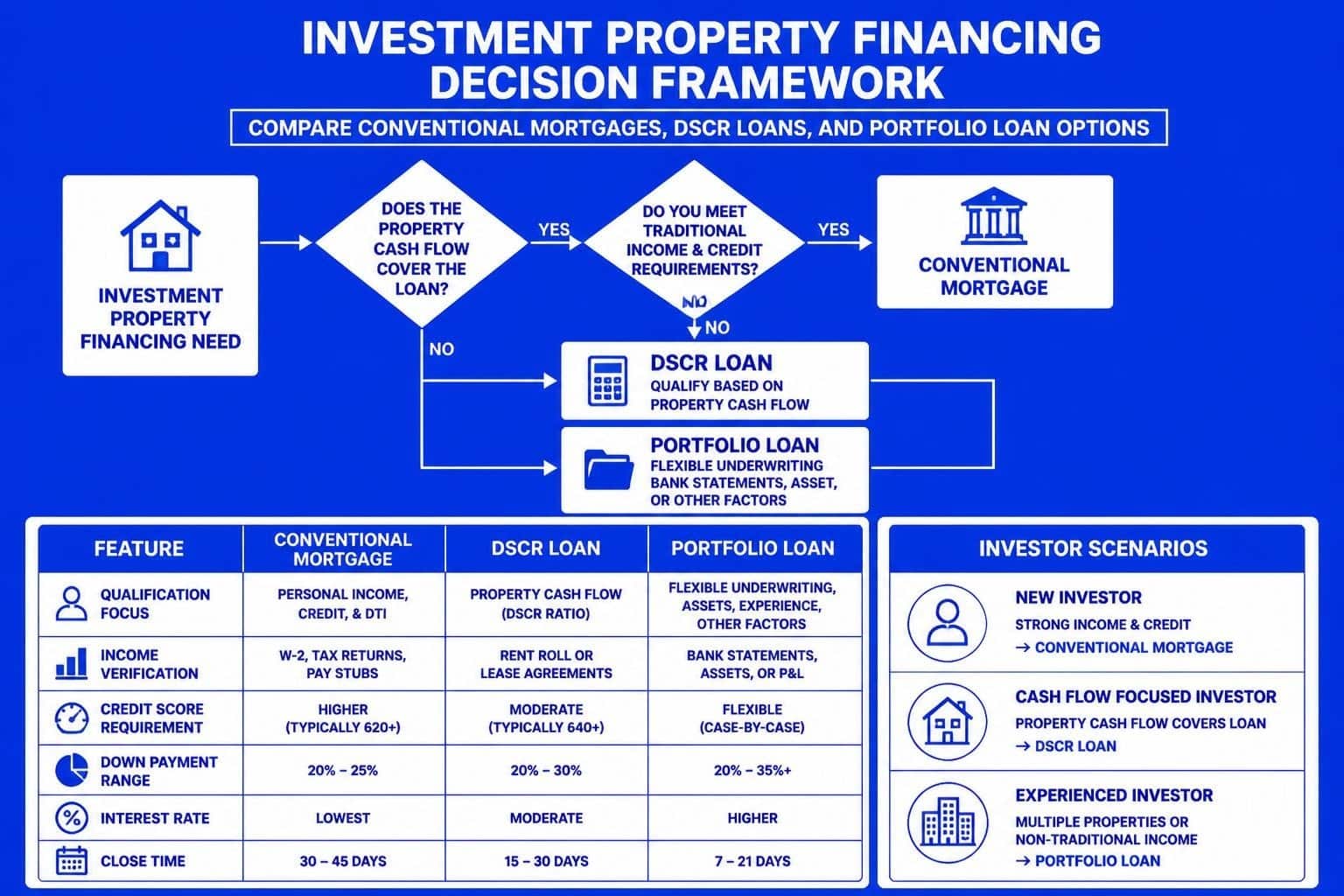

Rental property mortgage lenders operate differently from traditional residential lenders because they assess both borrower creditworthiness and property performance. These specialized lenders recognize that investment properties generate income streams that support mortgage payments, fundamentally changing the underwriting equation.

Investment property lenders fall into several categories:

- Conventional lenders offering investment property programs through Fannie Mae and Freddie Mac

- DSCR (Debt Service Coverage Ratio) specialized lenders who qualify borrowers based purely on rental income

- Portfolio lenders who keep loans in-house and offer flexible underwriting

- Private money lenders providing short-term bridge financing

- Credit unions serving local Seattle-area investors with relationship-based lending

The distinction between these lender types matters significantly. Conventional programs require full income documentation, tax returns, and personal debt-to-income calculations. Meanwhile, DSCR loans from specialized lenders streamline qualification by focusing exclusively on whether rental income covers the mortgage payment, property taxes, insurance, and HOA fees.

Key Differences from Primary Residence Financing

Rental property mortgage lenders implement stricter qualification standards compared to owner-occupied loans. Down payment requirements typically start at 15-25% for conventional investment loans, with the exact amount depending on credit scores, property type, and whether you already own other investment properties.

Interest rates on rental properties run approximately 0.5-0.75% higher than comparable primary residence loans. This pricing adjustment reflects the higher default risk lenders associate with investment properties, where owners might prioritize their primary residence payment if financial stress occurs.

Qualification Requirements for Investment Property Loans

Securing financing through rental property mortgage lenders requires meeting specific benchmarks that demonstrate both personal financial strength and property viability. Most conventional lenders require minimum credit scores of 620-640 for investment properties, though competitive rates typically demand scores above 700.

Financial reserves represent a critical qualification factor. Lenders typically require 6-12 months of mortgage payments (PITI) held in reserve for the investment property, in addition to any primary residence reserves. For Seattle-area investors purchasing a $600,000 rental property with a $3,500 monthly payment, this means demonstrating $21,000-$42,000 in liquid assets beyond the down payment and closing costs.

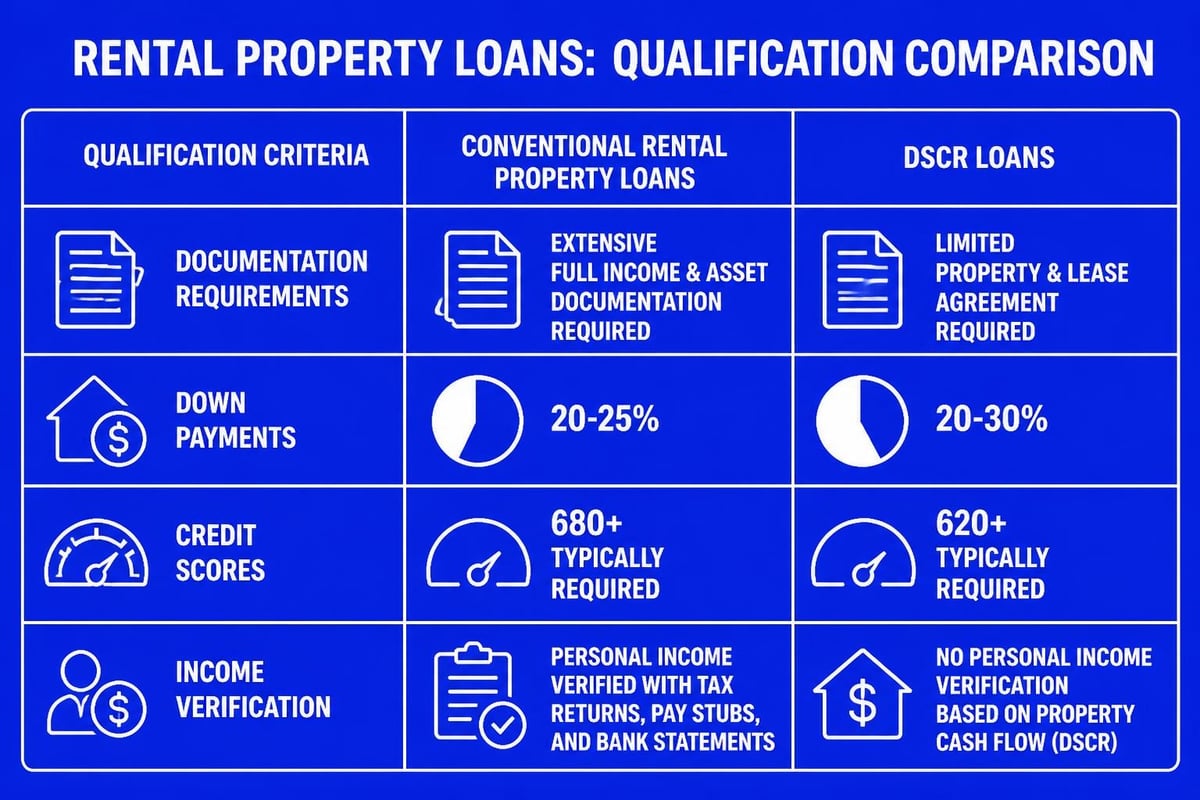

Documentation Standards Across Lender Types

Traditional rental property mortgage lenders require comprehensive documentation including two years of personal tax returns, two years of property tax returns if you already own rentals, W-2s or 1099s, two months of bank statements, and profit-and-loss statements for properties currently owned.

For tech professionals with complex compensation structures including RSUs, stock options, and bonuses, mortgage financing becomes more nuanced. Lenders calculate qualifying income differently for equity compensation, often requiring two-year histories and applying discounts or averaging methods that can significantly impact borrowing capacity.

| Lender Type | Income Documentation | Property Documentation | Typical Timeline |

|---|---|---|---|

| Conventional | Full tax returns, W-2s, paystubs | Appraisal, lease agreement, rent survey | 30-45 days |

| DSCR Lender | None required | Appraisal with rental analysis | 21-30 days |

| Portfolio Lender | Varies by relationship | Appraisal, business plan | 30-60 days |

| Hard Money | Bank statements only | Property valuation | 7-14 days |

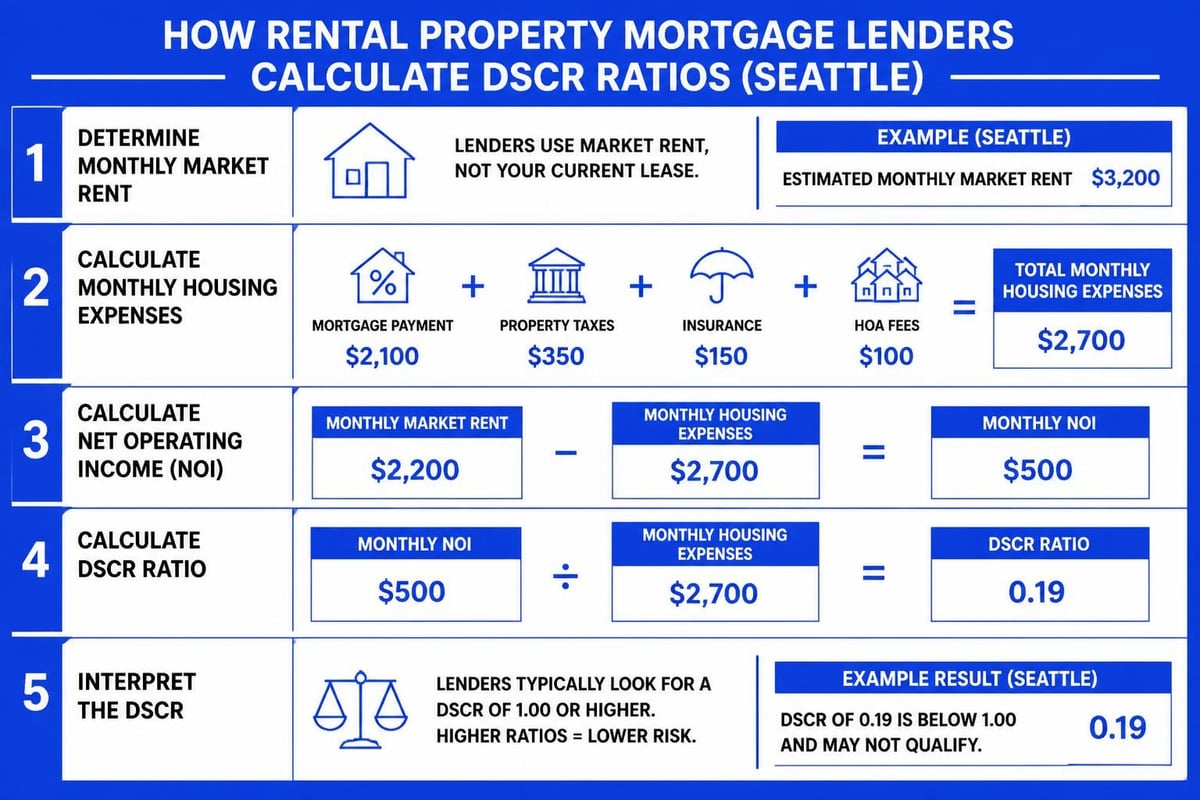

DSCR lenders revolutionized investor financing by eliminating personal income documentation entirely. These rental property mortgage lenders calculate a debt service coverage ratio by dividing the property's monthly rental income by its monthly mortgage payment (including taxes, insurance, and HOA fees). Ratios above 1.0 indicate the property generates sufficient income to cover all housing expenses.

Loan Programs for Seattle Investment Properties

Rental property mortgage lenders offer multiple program structures tailored to different investor profiles and property strategies. Understanding which program aligns with your investment approach and financial situation determines both qualification success and long-term profitability.

Conventional Investment Property Loans

Fannie Mae and Freddie Mac programs remain the foundation for most rental property financing, offering 30-year fixed rates with the strongest long-term value proposition. These programs allow investors to finance up to 10 properties simultaneously, making them ideal for building substantial portfolios across Seattle, Lynnwood, and Mill Creek.

Conventional investment loan requirements include:

- 15-25% down payment depending on credit score and property count

- Maximum debt-to-income ratio of 45%, including all rental property payments

- 75% of rental income counted toward qualifying (25% discount for vacancy and maintenance)

- Six-month reserve requirement per financed property

For a typical Shoreline duplex purchase at $750,000, conventional financing requires $112,500-$187,500 down, proof that total monthly debts don't exceed 45% of gross income after accounting for 75% of projected rental income, and liquid reserves of approximately $33,000.

DSCR and No-Doc Investment Loans

DSCR programs from specialized rental property mortgage lenders provide powerful alternatives for investors who don't meet conventional documentation standards or want streamlined qualification. Self-employed investors, those with significant tax write-offs, and borrowers managing multiple income streams benefit enormously from rental property financing options that ignore personal tax returns entirely.

These programs typically require 20-25% down payments and accept DSCR ratios as low as 1.0, meaning rental income exactly equals the mortgage payment. Many lenders prefer ratios of 1.15-1.25 for optimal pricing, creating situations where stronger property performance directly translates to better interest rates.

Interest rates on DSCR loans run 0.25-0.75% higher than conventional investment loans, but the qualification simplicity and speed often justify the premium. Properties in high-rent areas like Bellevue and Redmond perform particularly well under DSCR analysis, as strong rental markets generate ratios well above minimum thresholds.

Portfolio Lenders and Private Financing Options

Beyond agency programs, rental property mortgage lenders include portfolio lenders who establish their own underwriting guidelines and keep loans on their balance sheets rather than selling to Fannie Mae or Freddie Mac. This structure creates flexibility for unique properties, complex borrower situations, or investment strategies that don't fit conventional boxes.

Community banks and credit unions operating in the Seattle area often maintain portfolio lending divisions serving local real estate investors. These relationships-based lenders consider factors beyond credit scores and debt ratios, including overall banking relationship, local market knowledge, and property quality.

Bridge Loans and Hard Money Lending

Short-term financing from hard money lenders serves specific investment strategies like fix-and-flip projects, properties requiring substantial renovation, or time-sensitive purchases where conventional financing timelines don't work. These rental property mortgage lenders focus primarily on property value and after-repair value rather than borrower financials.

Hard money loans typically feature:

- Interest rates of 8-12% with 2-4 points in origination fees

- Loan-to-value ratios of 65-75% based on as-is or after-repair value

- Terms of 6-24 months requiring refinance or sale as exit strategy

- Minimal documentation and closing in 7-14 days

An investor purchasing a distressed Lake Forest Park property for $500,000 requiring $100,000 in renovations might secure a hard money loan at 70% LTV ($350,000), complete renovations increasing the value to $700,000, then refinance into conventional long-term financing once the property stabilizes and generates rental income.

Maximizing Approval Odds with Investment Property Lenders

Successfully securing financing from rental property mortgage lenders requires strategic preparation addressing the specific factors these lenders prioritize. Unlike primary residence purchases where stable employment history and personal income drive approval, investment lending emphasizes property performance, investor experience, and comprehensive financial positioning.

Building strong borrower profiles includes:

- Maintaining credit scores above 720 for optimal pricing across all lender types

- Documenting existing rental property management experience and successful performance

- Accumulating substantial reserves beyond minimum requirements

- Structuring personal finances to minimize debt-to-income ratios before applying

- Developing relationships with experienced mortgage brokers who specialize in investment lending

Property selection significantly impacts approval likelihood and terms. Lenders prefer single-family homes, duplexes, and small multifamily properties (2-4 units) in established neighborhoods with strong rental demand. Properties in Kirkland, Redmond, and Bellevue command favorable terms due to consistently strong rental markets and appreciation trends.

Leveraging Tech Compensation for Investment Purchases

Seattle-area tech professionals possess unique advantages when working with rental property mortgage lenders, particularly those familiar with equity compensation structures. RSUs, ESPP income, and annual bonuses create substantial qualifying income when properly documented and presented.

However, lenders apply specific methodologies to equity compensation. Most require two-year histories of RSU vesting, calculate averages across that period, and may apply 70-100% of the averaged amount depending on vesting likelihood and company stability. Microsoft and Amazon employees often receive full credit due to company stability, while startup equity faces heavier discounting.

For an investor earning $150,000 base salary plus $100,000 annually in vested RSUs, conventional lenders might calculate qualifying income at $200,000-$225,000 depending on consistency and documentation. This distinction determines maximum purchase price and overall borrowing capacity across jumbo loan scenarios.

Rate Shopping and Lender Comparison Strategies

Not all rental property mortgage lenders offer identical terms, pricing, or service quality. Systematic comparison across multiple lender types ensures optimal financing for your specific situation and investment strategy.

Key comparison factors include:

- Interest rate and APR after accounting for all fees and points

- Closing timeline and ability to meet purchase contract deadlines

- Prepayment penalties or restrictions on future refinancing

- Recourse versus non-recourse loan structures

- LLC or entity ownership allowances

Conventional lenders through mortgage brokers often provide the most competitive rates for well-qualified borrowers with strong documentation. DSCR specialists excel for borrowers seeking speed and simplified qualification. Portfolio lenders shine for unique properties or complex situations requiring human underwriting judgment.

Working with Specialized Investment Loan Officers

Engaging loan officers who specialize in investment property financing rather than generalist mortgage originators dramatically impacts success rates and terms. Specialized professionals understand nuances like how to maximize rental income calculations, which properties lenders favor, and how to structure multiple property purchases for optimal qualification.

In markets like Everett and Mill Creek where investment opportunities may include properties requiring renovation or unique configurations, experienced loan officers navigate complex scenarios that might result in denial from lenders unfamiliar with investment lending. They also maintain relationships with multiple rental property mortgage lenders, enabling them to match borrowers with optimal programs rather than forcing every scenario through a single lender's guidelines.

| Evaluation Criteria | Questions to Ask | Why It Matters |

|---|---|---|

| Investment Specialization | What percentage of your business involves rental property loans? | Specialists understand investment underwriting nuances |

| Lender Relationships | Which rental property mortgage lenders do you work with? | Access to multiple programs ensures best fit |

| Portfolio Strategy | How do you help investors scale to multiple properties? | Long-term partnership beyond single transaction |

| Rate Competitiveness | How do your investment property rates compare to market averages? | Direct impact on cash flow and ROI |

Tax Considerations and Strategic Structuring

Understanding how rental property mortgage lenders interact with tax strategies and ownership structures prevents costly mistakes and optimizes long-term wealth building. The mortgage interest deduction on investment properties operates differently from primary residences, with all mortgage interest remaining fully deductible against rental income regardless of loan amount.

Investors should coordinate financing decisions with tax advisors, particularly around timing of purchases, refinances, and property sales. Cash-out refinances on investment properties provide tax-free access to equity, creating capital for additional purchases without triggering taxable events.

Entity Ownership and Financing Options

Many investors prefer holding rental properties in LLCs for liability protection, but this ownership structure affects lender options. Most conventional rental property mortgage lenders require personal ownership rather than LLC titling, with some allowing LLC ownership after closing through quit-claim deed with lender approval.

Specialized portfolio lenders and DSCR programs increasingly accommodate direct LLC ownership, recognizing investor preferences for liability protection. These programs typically require personal guarantees but allow properties to title directly in entity names from origination.

For Seattle investors building substantial portfolios, working with conventional loan lenders who understand entity structures and can navigate the complexities of multi-property financing becomes essential to sustainable growth strategies.

Market-Specific Considerations for Seattle Investors

Local market dynamics significantly influence both financing availability and investment viability when working with rental property mortgage lenders. Seattle's strong job market, limited housing supply, and consistent population growth create favorable conditions for rental property investing, particularly in submarkets with new employment centers.

Redmond's continued Microsoft campus expansion and presence of Nintendo of America, SpaceX, and other tech employers creates consistent rental demand from high-income professionals. Lenders view Redmond investment properties favorably due to these economic fundamentals, often resulting in competitive terms and straightforward appraisals.

Bellevue's urban density and walkability premium attracts renters willing to pay premium rates for location convenience. Investment properties near transit stations, downtown Bellevue, or within top school boundaries command strong rental rates that easily satisfy DSCR requirements, even at higher purchase prices.

Appraisal Challenges in Competitive Markets

Rental property mortgage lenders base loan amounts on appraised value, making appraisal accuracy critical to deal success. Seattle's competitive market sometimes creates scenarios where purchase prices exceed recent comparable sales, particularly for properties with income-enhancing features like ADUs or recent renovations.

Experienced investors prepare comprehensive rent comparables, document property improvements, and provide appraisers with relevant market data to support valuations. Some rental property mortgage lenders allow desktop appraisals or appraisal waivers for refinances, accelerating timelines and reducing costs for properties with clear automated valuation model support.

Properties in Shoreline and Lake Forest Park sometimes face appraisal challenges due to smaller comparable pools and diverse property types. Working with lenders familiar with these submarkets and their unique characteristics prevents delays and ensures realistic expectations around loan amounts.

Building Long-Term Lender Relationships

Successful real estate investors recognize that relationships with quality rental property mortgage lenders represent valuable business assets. As portfolios grow from one property to four, eight, or ten properties, having established relationships with lenders who understand your strategy, trust your track record, and prioritize your business creates competitive advantages.

Relationship benefits include:

- Faster pre-approval and underwriting as lenders become familiar with your financial profile

- Flexibility during challenging scenarios based on proven payment history

- Access to off-market loan products or special programs not broadly advertised

- Priority processing during high-volume periods when capacity constraints affect timelines

- Strategic guidance on optimal timing for refinances, cash-out scenarios, and portfolio expansion

Maintaining these relationships requires consistent communication, prompt response to documentation requests, and financial discipline that translates to on-time payments and successful property performance. Investors who close multiple loans with the same lender build credibility that pays dividends through preferential treatment and better terms.

Advanced Strategies for Portfolio Scaling

Experienced investors working with rental property mortgage lenders employ sophisticated strategies to accelerate portfolio growth while managing risk and maintaining qualification capacity. Understanding these approaches distinguishes casual investors from professionals building substantial wealth through real estate.

Cross-collateralization allows investors to leverage equity in existing properties to fund down payments on new acquisitions. Cash-out refinances on performing properties with substantial appreciation provide capital for subsequent purchases without requiring savings accumulation or asset liquidation.

1031 exchanges combined with strategic financing create powerful tax-deferred growth opportunities. Investors sell appreciated properties, defer capital gains through 1031 exchange into larger or multiple replacement properties, and establish new mortgages on the replacement properties that reset basis and depreciation schedules.

BRRRR strategies (Buy, Rehab, Rent, Refinance, Repeat) pair bridge financing with long-term rental property mortgage lenders to recycle capital efficiently. Investors purchase distressed properties with hard money loans, complete renovations, stabilize with tenants, then refinance into conventional long-term financing that returns most or all invested capital for deployment into the next project.

For Everett and Mill Creek investors where property prices remain more accessible than core Seattle markets, BRRRR strategies create opportunities to build equity through forced appreciation while establishing cash-flowing assets that generate passive income and long-term wealth.

Choosing the right rental property mortgage lenders directly impacts both immediate deal success and long-term portfolio performance. By understanding the distinct qualification approaches, program options, and strategic considerations across lender types, Seattle-area investors position themselves to build substantial real estate wealth efficiently and sustainably. Whether you're a tech professional looking to diversify beyond stock compensation or an experienced investor scaling your portfolio across Bellevue, Redmond, and surrounding markets, working with knowledgeable financing partners who understand investment lending makes all the difference. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area investors secure optimal financing for rental properties, with specialized expertise in qualifying complex compensation structures and navigating the unique dynamics of Pacific Northwest real estate markets.