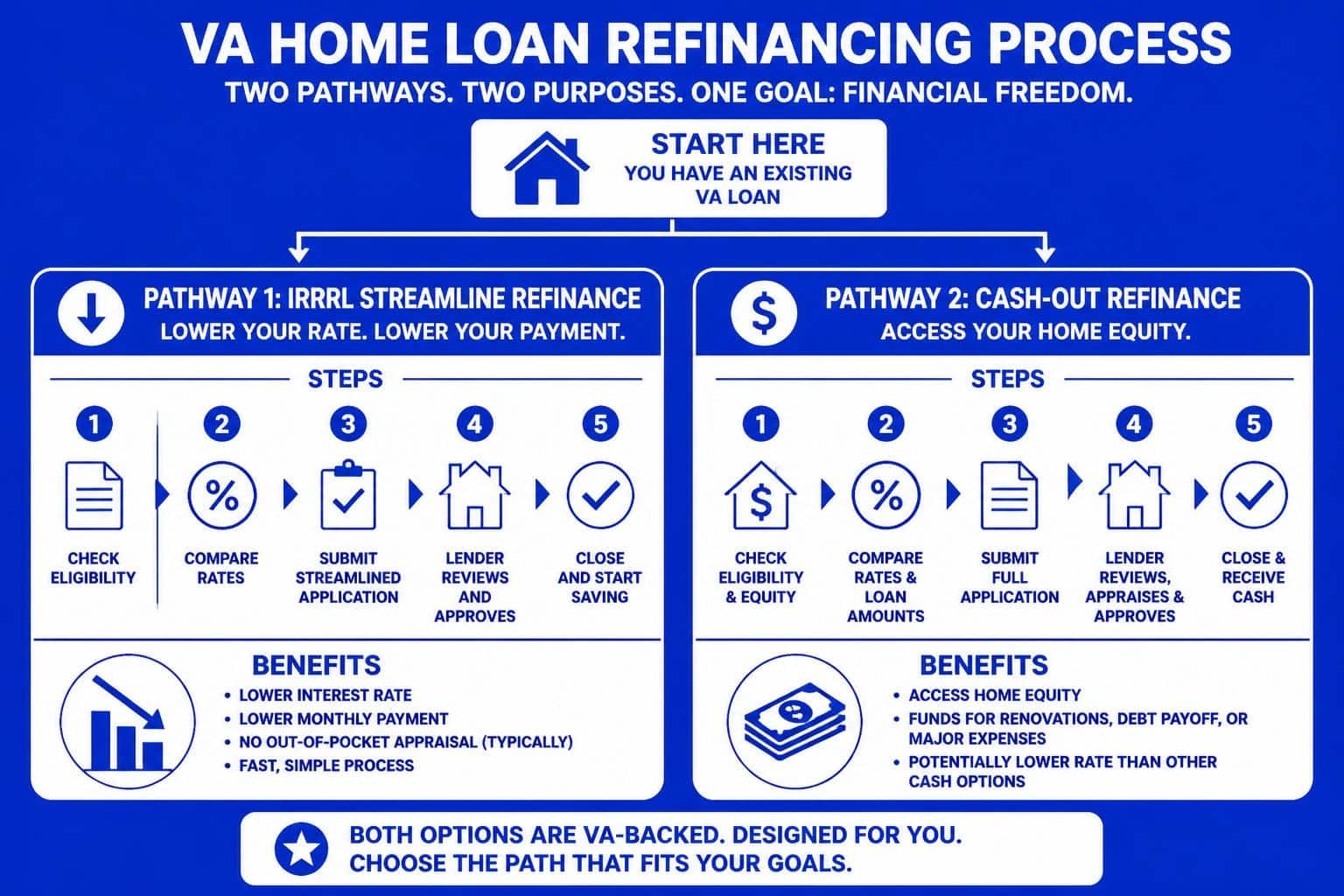

Veterans and active-duty service members throughout the Greater Seattle area have access to some of the most powerful refinancing benefits available in the mortgage industry. VA home loans refinance options provide opportunities to reduce monthly payments, access home equity, or shorten loan terms without many of the restrictions conventional borrowers face. Whether you're in Seattle, Bellevue, Redmond, Kirkland, or surrounding communities like Shoreline and Lynnwood, understanding these specialized refinance programs can unlock substantial savings and financial flexibility. With Seattle-area home values appreciating significantly over recent years, many veterans are sitting on considerable equity they can leverage strategically.

Understanding VA Home Loans Refinance Options

The Department of Veterans Affairs supports two primary refinance pathways designed specifically for eligible veterans, active-duty service members, and qualifying surviving spouses. Each program serves distinct financial objectives and comes with unique advantages.

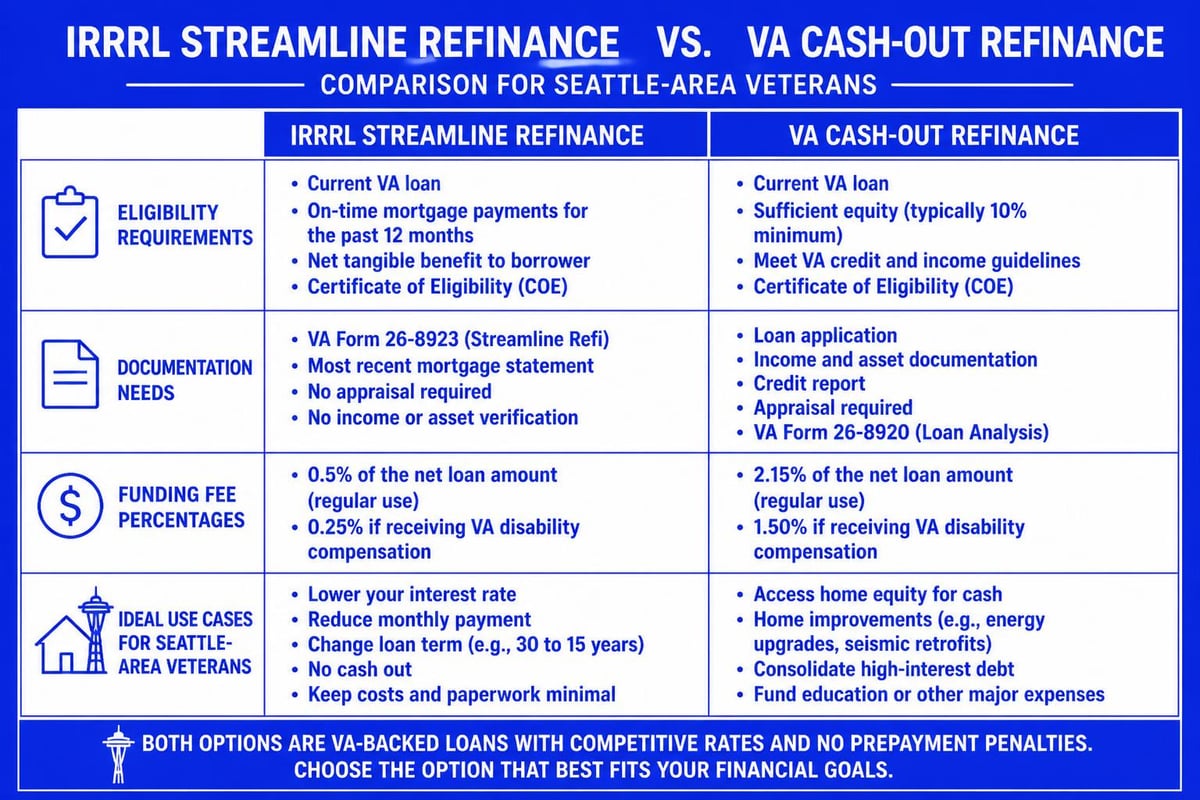

The Interest Rate Reduction Refinance Loan (IRRRL), commonly called the VA streamline refinance, focuses exclusively on lowering your interest rate or converting from an adjustable-rate mortgage to a fixed-rate loan. This option requires minimal documentation and no appraisal in most cases, making it the fastest path to reduced payments.

Key IRRRL Features:

- No appraisal typically required

- Limited income verification

- Refinance up to 100% of property value

- No out-of-pocket costs allowed

- Funding fee can be rolled into loan balance

- Must result in lower payment or more stable loan terms

The second option, the VA cash-out refinance, allows you to tap into your home equity while refinancing. This program permits borrowing up to 100% of your home's current value, providing funds for debt consolidation, home improvements, education expenses, or other financial needs.

IRRRL: The Streamlined Path to Lower Rates

For Seattle veterans looking to reduce their monthly mortgage payment quickly, the IRRRL represents the most efficient solution. This program earned its "streamline" designation through significantly reduced documentation requirements compared to traditional refinancing.

Eligibility Requirements for IRRRL

You must currently have a VA-backed mortgage to qualify for an IRRRL. The refinance must result in a lower interest rate, unless you're converting from an adjustable-rate to a fixed-rate mortgage. You'll need a Certificate of Eligibility, though lenders can typically obtain this electronically during the application process.

Documentation Typically Required:

- Current mortgage statement

- Certificate of Eligibility (COE)

- Payment history verification

- Credit report authorization

- Minimal income documentation

The occupancy requirement for IRRRL is straightforward. You must certify that you previously occupied the property as your primary residence. Current occupancy isn't required, making this ideal for veterans who've relocated from Seattle to other areas but retain their Washington property as a rental investment.

Cost Considerations and Funding Fees

The VA funding fee for IRRRL in 2026 stands at 0.5% of the loan amount for most borrowers. Veterans with service-connected disabilities are exempt from this fee. Unlike conventional refinancing, lenders cannot charge you out-of-pocket costs with an IRRRL-all fees must be rolled into the new loan balance.

| Cost Component | IRRRL | Traditional Refinance |

|---|---|---|

| Funding Fee | 0.5% (waived for disabled veterans) | N/A |

| Appraisal | Usually not required | Required |

| Income Verification | Minimal | Full documentation |

| Out-of-Pocket Costs | Not allowed | Typically required |

For a $600,000 refinance common in Seattle's competitive housing market, the funding fee would total $3,000. When working with experienced mortgage brokers, you can model precisely when the accumulated savings justify this upfront investment.

VA Cash-Out Refinance: Accessing Your Equity

Seattle-area home values have risen substantially, creating significant equity for veteran homeowners who purchased even just a few years ago. The VA cash-out refinance enables you to convert this equity into accessible funds while potentially securing better loan terms.

How VA Cash-Out Refinance Works

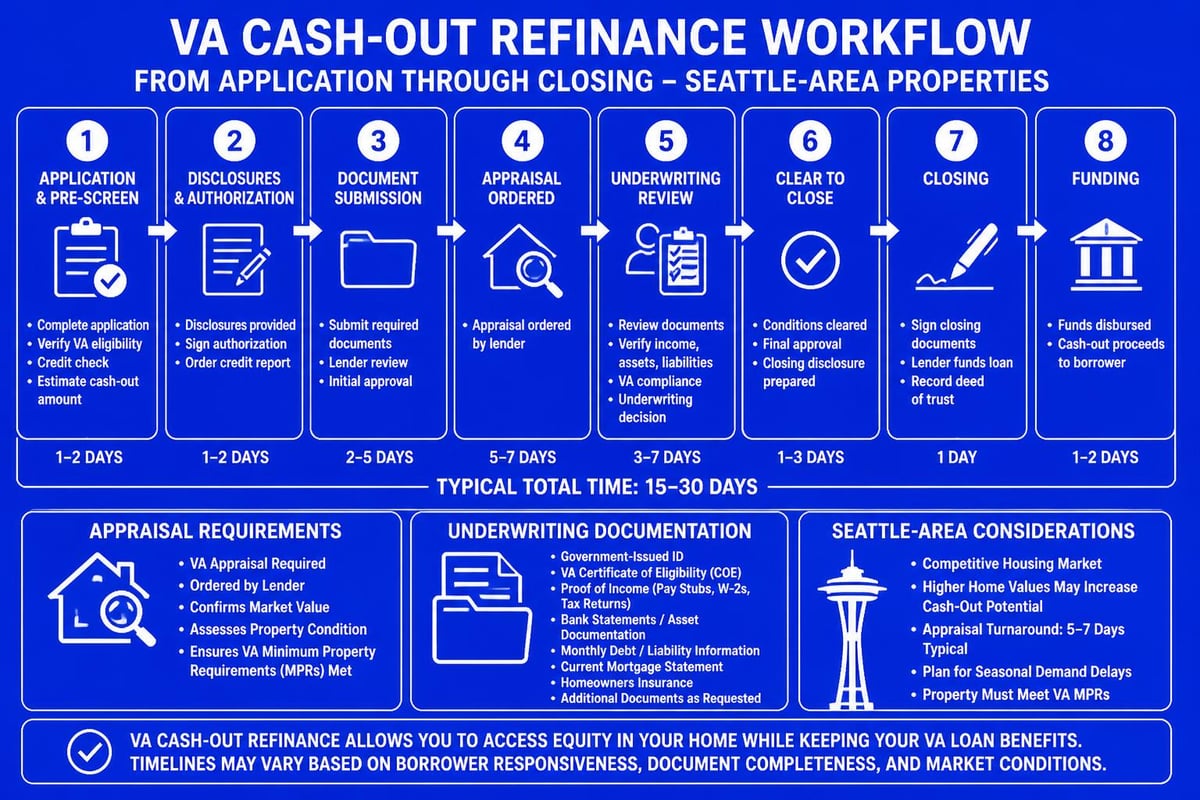

Unlike the IRRRL, a cash-out refinance requires a full appraisal and complete income verification. You can refinance up to 100% of your home's current appraised value, though most lenders recommend maintaining some equity cushion for financial stability.

The program works with both existing VA loans and conventional mortgages. If you currently have a conventional loan, you can refinance into a VA cash-out loan, often eliminating private mortgage insurance while accessing equity. This conversion particularly benefits veterans who initially purchased with conventional financing before learning about VA loan benefits.

Common Uses for Cash-Out Funds:

- Home renovations and improvements

- Debt consolidation at lower interest rates

- Education expenses for family members

- Investment property down payments

- Emergency fund establishment

- Business capital

For tech professionals at Amazon, Microsoft, or Google who receive significant stock compensation, the cash-out refinance can provide liquidity without triggering taxable events from selling RSUs or options. This strategy aligns particularly well with the financial planning needs common among Seattle's technology sector.

Cash-Out Refinance Requirements and Limits

The VA cash-out refinance carries stricter requirements than the IRRRL. You must have sufficient income to support the new loan amount, meet credit standards (typically 620+ FICO score), and demonstrate occupancy or occupancy intent.

Essential Qualification Criteria:

- Current property appraisal required

- Debt-to-income ratio typically below 41%

- Minimum credit score around 620

- Certificate of Eligibility

- Verification of income and assets

- Primary residence or occupancy certification

The funding fee for cash-out refinancing differs from IRRRL rates. For first-time VA loan users, the fee equals 2.3% of the loan amount. Subsequent use increases this to 3.6%. Veterans with service-connected disabilities remain exempt from all funding fees.

In markets like Bellevue and Redmond where median home prices exceed $900,000, this funding fee represents a significant cost factor. A $700,000 cash-out refinance for a subsequent user would carry a $25,200 funding fee. Strategic planning with a knowledgeable Seattle mortgage broker helps determine whether the benefits justify these costs for your specific situation.

Comparing VA Refinance to Conventional Options

Veterans considering refinancing should understand how VA programs compare against conventional alternatives. The differences often prove substantial, particularly for high-balance loans common throughout the Seattle metropolitan area.

Rate and Cost Advantages

VA loans consistently offer interest rates 0.25% to 0.50% below comparable conventional mortgages. This discount stems from the VA guarantee, which reduces lender risk. For a $600,000 loan, a 0.375% rate advantage saves approximately $135 monthly-$1,620 annually.

Conventional refinancing requires private mortgage insurance (PMI) when loan-to-value exceeds 80%. VA programs never require mortgage insurance regardless of loan-to-value ratio. For Seattle homeowners refinancing with less than 20% equity, this elimination of PMI often outweighs any other cost considerations.

| Feature | VA Refinance | Conventional Refinance |

|---|---|---|

| Maximum LTV | 100% (cash-out) | 80% without PMI |

| Mortgage Insurance | Never required | Required above 80% LTV |

| Funding Fee | 0.5%-3.6% (one-time) | N/A |

| Interest Rates | Typically 0.25%-0.50% lower | Market rate |

| Closing Costs | Competitive, IRRRL limits apply | Standard closing costs |

Understanding these distinctions helps veterans make informed decisions. Mortgage financing professionals familiar with both VA and conventional products can provide side-by-side comparisons tailored to your financial situation.

Timing Your VA Home Loans Refinance

Market conditions in Seattle fluctuate, creating varying opportunities for refinancing throughout economic cycles. Knowing when to refinance maximizes your financial benefit.

Rate Environment Considerations

The traditional rule suggests refinancing when you can reduce your rate by at least 0.75% to 1.0%. However, the IRRRL's low costs and streamlined process make refinancing worthwhile with smaller rate improvements-sometimes as little as 0.5%.

Optimal Refinance Timing Indicators:

- Interest rates drop 0.5% or more below your current rate

- Your credit score has improved significantly since original loan

- You plan to remain in the property at least 2-3 years

- Home values have risen, increasing available equity

- You need to convert from adjustable to fixed-rate financing

In competitive markets like Kirkland and Mill Creek, property values can shift rapidly. Monitoring these trends helps identify windows when cash-out refinancing becomes particularly advantageous. Some veterans successfully time refinances to coincide with appraisal peaks, maximizing accessible equity.

Break-Even Analysis

Calculate your break-even point before committing to any va home loans refinance. Divide total closing costs by monthly savings to determine how many months you need to recoup your investment.

For an IRRRL with $5,000 in total costs (including the funding fee) that saves $200 monthly, your break-even point occurs at 25 months. If you anticipate remaining in the property beyond this timeframe, refinancing makes financial sense. Experienced mortgage professionals provide detailed break-even calculations customized to your specific loan scenario.

Special Considerations for Seattle Veterans

The Pacific Northwest housing market presents unique characteristics that influence refinancing decisions. Seattle's strong economy, driven by technology and aerospace industries, creates specific opportunities and challenges for veteran homeowners.

High-Balance Loan Limits

King County's conforming loan limit for 2026 reaches $891,250 for single-family homes. VA loans follow these limits, but many Seattle-area properties exceed even these thresholds. The good news: VA loans have no absolute maximum, though lenders typically cap eligibility around $2 million for most borrowers.

For properties valued above conforming limits, your VA entitlement works differently. Veterans with full entitlement remaining can still obtain 100% financing, but those with partial entitlement used may need a down payment for the portion exceeding limits. This complexity makes working with jumbo home loan specialists particularly valuable in Seattle's expensive housing market.

Property Type Considerations

The VA approves various property types for refinancing, but certain restrictions apply. Single-family homes, condominiums in VA-approved buildings, townhouses, and multi-unit properties (up to four units) qualify when you occupy one unit.

In Seattle neighborhoods like Capitol Hill, Ballard, and Queen Anne, many veterans own condominiums. Verify that your building maintains VA approval before pursuing refinancing. Buildings can lose approval if homeowner association financial health deteriorates or required maintenance falls behind. Your lender confirms approval status during the application process.

Documentation and Application Process

Preparing proper documentation accelerates your va home loans refinance application and prevents delays. While IRRRL requires minimal paperwork, cash-out refinancing demands comprehensive financial documentation.

Essential Documents for IRRRL

The streamlined nature of IRRRL means you'll provide less documentation than original home purchases. However, gathering these items before application ensures smooth processing:

- Current mortgage statement showing payment history

- Government-issued photo identification

- Certificate of Eligibility (lender can obtain electronically)

- Previous occupancy certification

- Credit report authorization

- Bank statements for closing costs

Most lenders process IRRRLs without requiring pay stubs, tax returns, or employment verification. This reduction in paperwork reflects the program's streamlined design.

Comprehensive Documentation for Cash-Out Refinance

Cash-out refinancing requires full income and asset verification similar to purchase transactions. Tech professionals with complex compensation structures should prepare detailed documentation of base salary, bonuses, RSUs, and stock options.

Complete Cash-Out Documentation List:

- Two years of tax returns with all schedules

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Investment account statements showing stock holdings

- Employment verification letter

- Property insurance declarations

- Homeowner association documents (if applicable)

- Appraisal (ordered by lender)

For Microsoft, Amazon, and Google employees, specialized documentation proves stock compensation stability. Mortgage brokers experienced with tech sector compensation understand how to qualify RSUs and options properly, maximizing your borrowing power for refinancing.

Working with Lenders and Closing Timeline

VA home loans refinance transactions typically close faster than conventional refinances, particularly for IRRRLs. Understanding the timeline helps you plan accordingly.

Expected Timeline and Milestones

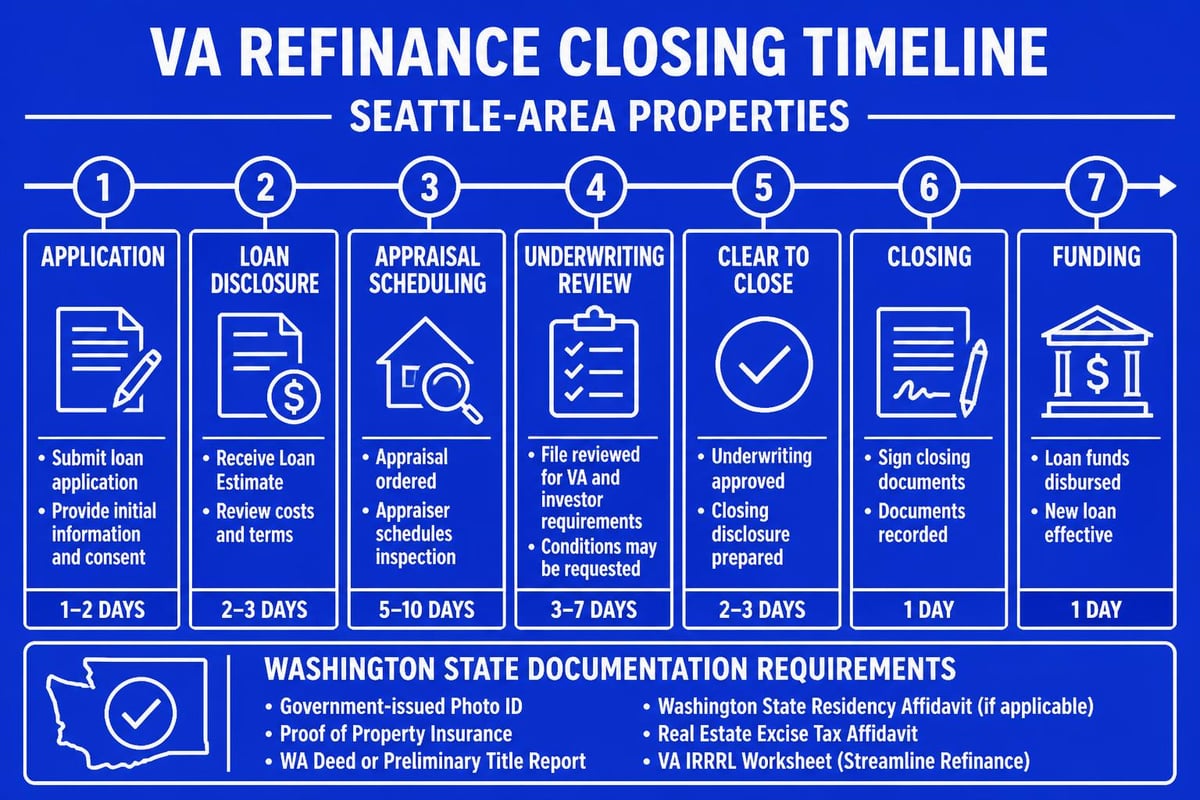

IRRRL refinances often close within 20-30 days when documentation flows smoothly. Cash-out refinances take 30-45 days due to appraisal requirements and comprehensive underwriting.

Typical Refinance Timeline:

- Days 1-3: Application submission and initial review

- Days 4-7: Appraisal ordered (cash-out only)

- Days 8-14: Title work and preliminary underwriting

- Days 15-20: Appraisal completed and reviewed

- Days 21-25: Final underwriting approval

- Days 26-30: Clear to close and closing scheduled

Some lenders offer expedited processing for qualified borrowers. When time sensitivity matters, discuss acceleration options during your initial consultation. The ability to close loans quickly proves particularly valuable in Seattle's fast-paced market.

Choosing the Right Lender

Not all lenders offer identical VA refinance programs or service levels. Compare multiple factors beyond interest rates when selecting your lender.

Veterans should evaluate lender expertise with VA products specifically. Some mortgage companies process few VA loans, leading to processing delays and potential guideline misunderstandings. Lenders specializing in VA loans typically provide smoother experiences and faster closings.

Critical Lender Selection Factors:

- VA loan volume and specialization

- Interest rate competitiveness

- Funding fee policies and calculations

- Processing timeline commitments

- Communication style and responsiveness

- Local market knowledge (especially for Seattle nuances)

- Tech sector compensation expertise

Reading reviews from other veterans provides insight into lender performance. Look for patterns in feedback regarding communication, timeline accuracy, and problem-solving ability when challenges arise.

Maximizing Your VA Refinance Benefits

Strategic planning enhances the value you extract from va home loans refinance programs. Consider these optimization strategies when structuring your refinance.

Rate Shopping and Timing

VA loan rates fluctuate daily based on bond market movements. Monitoring rate trends over several weeks helps identify favorable entry points. Most lenders allow rate locks for 30-60 days, protecting you from increases during processing.

Request loan estimates from multiple lenders simultaneously. This approach ensures rate quotes reflect identical market conditions, enabling accurate comparisons. Focus on the Annual Percentage Rate (APR) rather than just the interest rate, as APR incorporates fees and provides a complete cost picture.

Leveraging Equity Strategically

For cash-out refinancing, calculate the optimal amount to withdraw. Taking excessive equity reduces your financial cushion and increases monthly payments. Conversely, taking too little may necessitate another transaction later, incurring duplicate closing costs.

Consider your specific financial goals when determining cash-out amounts. Debt consolidation proves worthwhile when credit card rates exceed 15-20%, but consolidating low-rate auto loans may not make financial sense. Run detailed analyses comparing your current debt structure against the refinanced scenario.

Understanding Funding Fee Exemptions

Veterans with service-connected disabilities receive full funding fee exemptions on VA home loans refinance transactions. This benefit produces substantial savings-potentially tens of thousands of dollars on large Seattle-area loan amounts.

Even minor disability ratings (10% or higher) qualify for exemption. If you've recently received a disability rating, provide documentation to your lender before closing. Retroactive fee refunds are possible but involve additional administrative complexity.

Purple Heart recipients also receive funding fee waivers. Surviving spouses of veterans who died in service or from service-connected conditions qualify for this exemption as well.

Refinancing Rental Properties with VA Loans

Veterans who've relocated from Seattle but retain their property as a rental face specific refinancing considerations. The VA permits refinancing these properties under certain circumstances.

Occupancy Requirements for Investment Properties

The original VA loan required you to occupy the property as your primary residence. For refinancing, you must certify previous occupancy but need not currently live there. This flexibility enables refinancing properties that have transitioned to rental use.

IRRRL refinancing on rental properties proceeds identically to owner-occupied refinancing. The streamlined process doesn't change based on current occupancy status. Cash-out refinancing requires additional rental income documentation to qualify, as lenders must verify your ability to carry the new mortgage.

Rental Income Qualification

When refinancing a rental property with VA cash-out, lenders analyze rental income to support the new loan amount. They typically use 75% of gross rental income to offset the mortgage payment in debt-to-income calculations.

Properties located in strong Seattle rental markets like Fremont, Wallingford, and University District often generate sufficient income to qualify easily. Provide lease agreements and deposit documentation proving rental income stability. Properties rented to Section 8 tenants offer particularly strong income verification due to government payment guarantees.

Common VA Refinance Mistakes to Avoid

Veterans sometimes encounter preventable obstacles during refinancing. Awareness of these pitfalls helps you navigate the process successfully.

Failing to Compare Multiple Lenders

Accepting the first refinance offer without shopping constitutes a costly mistake. Interest rate variations of 0.125% to 0.25% between lenders are common. On a $500,000 loan, a 0.25% rate difference equals approximately $75 monthly-$900 annually.

Obtain at least three loan estimates from different lenders. Qualified mortgage brokers access multiple investor channels, potentially offering better rates than single-source direct lenders. The comparison process takes minimal time but produces substantial savings.

Ignoring Credit Score Impact

Many veterans assume VA loans require no credit standards. While the VA itself imposes no minimum score, individual lenders establish their own requirements-typically 580-620 for cash-out refinancing.

Check your credit reports several months before refinancing. Dispute errors, pay down revolving balances, and avoid new credit applications. Even modest score improvements can reduce your interest rate or expand lender options.

Refinancing Too Frequently

The VA limits IRRRL usage to once every 210 days from the previous loan's closing. Some veterans refinance repeatedly chasing minor rate improvements, accumulating funding fees that negate savings.

Calculate true cost-benefit including all fees before pursuing another refinance. Unless rates drop substantially (0.75% or more), frequent refinancing often proves counterproductive. The 210-day seasoning requirement prevents the most egregious churning, but longer intervals typically serve your financial interests better.

Overlooking State-Specific Costs

Washington State imposes specific closing costs that impact refinancing economics. The state excise tax doesn't apply to refinances, but recording fees, title insurance, and escrow charges still accumulate.

In King County, expect title and escrow fees around $1,500-$2,500 depending on loan size. Pierce and Snohomish counties have similar fee structures. Factor these region-specific costs into break-even calculations for accurate financial projections.

VA Refinance FAQs for Seattle Veterans

Addressing common questions provides clarity on va home loans refinance programs and their application to local situations.

Can I refinance if I've had a recent bankruptcy or foreclosure?

Yes, though waiting periods apply. VA guidelines permit refinancing two years after Chapter 7 bankruptcy discharge and one year into a Chapter 13 repayment plan. Foreclosures typically require a two-year waiting period. These timeframes are shorter than conventional loan requirements.

Do I need to use my VA loan benefit to buy before I can refinance?

No. Veterans can refinance conventional mortgages into VA loans through the cash-out program. This strategy eliminates PMI and often secures better rates. You must have sufficient VA entitlement remaining and meet standard qualification criteria.

How does the VA funding fee compare to conventional closing costs?

The IRRRL funding fee (0.5%) typically costs less than conventional refinance closing costs (2-3% of loan amount). Cash-out funding fees (2.3-3.6%) approximate conventional costs but eliminate ongoing PMI requirements.

Can I refinance a VA loan on a manufactured home?

Yes, manufactured homes on permanent foundations qualify for VA refinancing. The home must meet HUD construction standards and be classified as real property rather than personal property. Verify your title status before proceeding.

What happens to my VA entitlement after refinancing?

IRRRL refinancing doesn't change your entitlement status-it remains tied to the property. Cash-out refinancing of a non-VA loan restores your previously used entitlement to the property. Understanding VA loan benefits helps maximize this valuable resource.

VA home loans refinance programs offer veterans throughout Seattle and surrounding communities powerful tools for reducing housing costs and accessing home equity. Whether you pursue an IRRRL for lower rates or a cash-out refinance for financial flexibility, understanding program requirements and strategic timing maximizes your benefits. Working with experienced professionals who specialize in VA products and understand the unique dynamics of the Seattle housing market ensures smooth processing and optimal outcomes. Keith Akada at Mortgage Reel brings 25+ years of expertise helping veterans and service members navigate refinancing decisions with clarity and confidence, backed by 750+ five-star reviews and specialized knowledge of tech sector compensation common among Seattle-area borrowers.